Shielding factor portfolios from credit downgrades and defaults

Speed read

Higher Sharpe ratio and reduced downside risk via enhanced factors

Improved downside risk management in portfolio construction

Multi-factor strategies well fitted to mitigate downgrades and defaults

Preventing downside risk is paramount when investing in corporate bonds, as the loss on a bond investment can be multiple times larger than its upside potential. Typical events that cause price declines are downgrades and defaults. Our research shows that a naïve academic implementation of a factor strategy leads to increased downside risk.1

Robeco’s multi-factorcredit strategies use two main methods to effectively bring down downgrade and default rates. First, by using enhanced factor definitions, we avoid the risks to which investors in generic factor definitions are unnecessarily exposed. Second, our proprietary portfolio construction algorithm manages risks and identifies high-risk names with the goal to effectively reduce the portfolio downgrade and default rates below benchmark levels. As a result, there typically is a reduction in downside risk in our portfolios, with the expectation that risk-adjusted returns improve.

The effect of downgrades and defaults on corporate bond returns

To investigate corporate bond returns around downgrades or defaults, we carried out an event study over the period 1994 to 2020. The finding was that, one year prior to being downgraded, the average bond underperformed its benchmark by 12%. For defaults, this underperformance was even greater, at 47%. To improve the return of a corporate bond strategy, it is therefore paramount to avoid having these bonds in the portfolio well in advance of a downgrade or default event.

Interestingly, the analysis also showed that a downgraded bond consistently outperforms the market after its initial decline, implying that the market overreacts to downgrades. This overreaction is particularly strong for downgrades from investment grade to high yield, also known as ‘fallen angels’.2

Downgrades and defaults in credit factor portfolios

Robeco’s multi-factor strategies in investment grade and high yield credits target balanced exposure to factors such as value, momentum, low-risk/quality and size. Generic versions of these factors have been documented in our academic work, showing that factor portfolios have better risk-adjusted returns than the overall credit market. These generic factors are defined such that they are applicable broadly across all corporate bonds as they use only corporate bond information.

Within our live investment strategies, we extend the generic factor definitions by using more sophisticated techniques and by using accounting and equity data to derive enhanced definitions. By avoiding unrewarded risks that are present in the generic definitions, these enhanced factors have previously been shown to have significantly higher risk-adjusted returns than the generic factors.

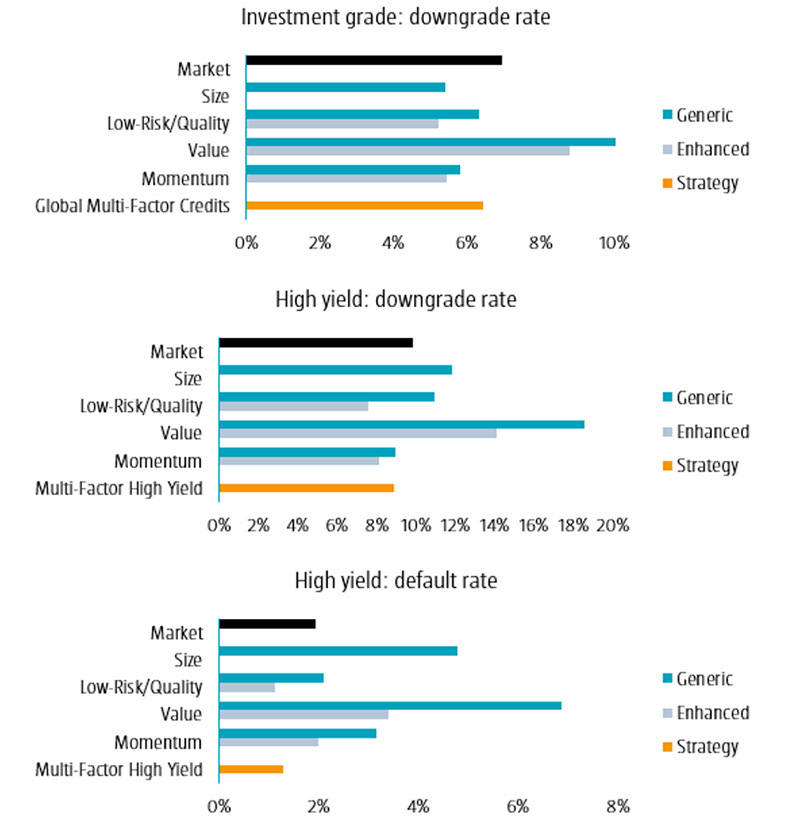

To analyze the probability of downgrade and default events in factor portfolios, we count the number of times a bond in a factor portfolio has been downgraded or has defaulted within 12 months of the establishment of the portfolio. We do this for the factor portfolios constructed using the academic approach in Houweling and Van Zundert (2017), where a factor portfolio invests in all bonds that are ranked in the top 10% of the investment universe, as sorted on that factor. The results are shown in Figure 1; defaults in investment grade are not shown, as there are too few observations to draw proper conclusions. We find that, for all factors, our enhanced factor definitions (the grey bars in the chart) effectively decrease the downgrade as well as the default rates compared to the generic definitions (the blue bars).

Figure 1 | 12-month-ahead downgrade and default rates

Across factors, we observe that the value factor has the highest downgrade as well as default rates. This is because the value factor favors bonds with higher spreads, compared to their peers. Its generic definition only corrects the credit spread for the bond’s rating, spread changes and maturity, but ignores company-specific differences beyond ratings that can be identified through, for example, equity or accounting information. The enhanced approach does take these dimensions along and therefore effectively decreases both downgrade and default rates.

Living up to its name, the enhanced low-risk/quality factor has the lowest downside risk. This is especially visible in the default rates, where the factor tilts away from the risky lower-rated segment of the market (CCC and below).

Downside risk management in multi-factor strategies

The academic implementation of the factor portfolios applies only very basic risk management to the portfolio and tends to be poorly diversified, as it simply buys all the bonds in the top decile. This can result in exposures to high-risk names and concentrated positions in certain high-risk market segments. Figure 1 also shows the downgrade and default rates of our multi-factor strategies (see the orange bars), which combine enhanced factors in a multi-factor approach to benefit from diversification. Moreover, these strategies apply our proprietary portfolio construction algorithm to control the risk of the portfolio in multiple dimensions using our DTS-based credit risk model. This effectively mitigates the downgrade and default risk as these strategies have reduced downgrades and defaults compared to their benchmarks.

Another element of the portfolio construction algorithm is a default-prediction rule that aims to exclude bonds that have a high probability of default. We find that portfolio construction with this generic rule is sufficient to bring down the downgrade rate (9.13%) and default rate (1.50%) of the multi-factor high yield strategy below those of the market.

One recent improvement to our portfolio construction algorithm is an enhanced default-prediction rule that replaces the more generic rule that was already in place. The enhanced rule uses market-based information in an effort to better predict default probabilities, without decreasing the risk-adjusted return of the strategy.

The impact of this enhanced rule is as follows:

The multi-factor credits strategy has only half the default rate and also fewer downgrades than the overall investment grade market. While rare in investment grade, the exposure to defaults is successfully reduced. The enhanced default-prediction rule delivers a small increase in the Sharpe ratio and a small decrease in downgrade rate.

The multi-factor high yield strategy benefits the most, as the probability of default is higher in this segment of the market, so that there is more to gain than in investment grade where downside risk is more limited. As a result of the enhancement, both downgrade and default rates decrease further.

Overall, our research shows that the multi-factor credits and multi-factor high yield strategies have attractive risk-adjusted returns and less downside risk compared to their benchmarks.

1This article is based on the paper “Limiting downside risk in Multi-Factor Credits and Multi-Factor High Yield”, by Joris Blonk and Patrick Houweling, October 2021. 2See “Is there value in fallen angels?”, by Robbert-Jan ‘t Hoen and Patrick Houweling, October 2020.