The Breadth of Benefits in Global High Yield

- When considering a global high yield strategy, investors may initially contemplate the rationale of positioning based on differences in regional economic growth and relative value. While those variations remain critical to allocation decisions, investors should also remain cognizant of the structural benefits of traversing regions, which we explain in the concluding post of our series on European High Yield.

- Although there are numerous global strategies from which to choose, our macroeconomic scenarios continue to indicate a supportive backdrop for global high yield assets amidst expectations that default rates remain within historical norms.

- Furthermore, the increase in global yields to near decade-high levels indicates an opportunity to consider an actively managed global strategy given the potential to generate alpha and total return.

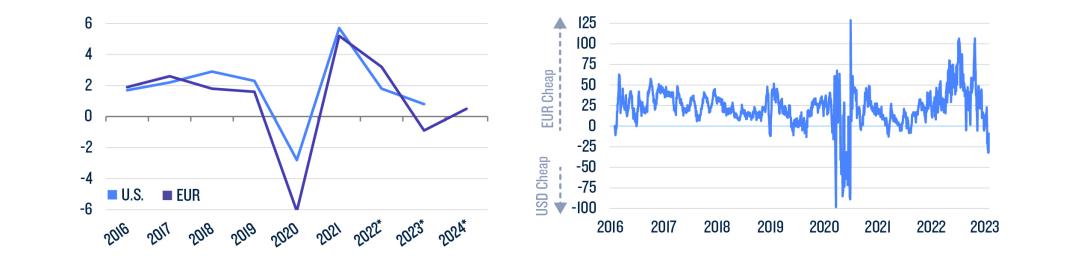

Rapidly shifting conditions across global regions has become one of the defining characteristics of the current market environment. Although processing the implications of differences in GDP growth and relative value can be disorienting (Figure 1), they play into the strengths of an active global high yield strategy.

Figure 1: The shift in global growth and high yield relative value over time (LHS: U.S. and EA GDP growth, %; RHS: Median EUR - USD L-OAS difference of selected dual currency bond issuers (average of mean and median))

Source: PGIM Fixed Income as of February 3, 2023. *Represents PGIM Fixed Income estimates.

Yet, these factors are only part of the reason for investing across regions. An active global high yield strategy also features the flexibility to benefit from structural nuances in credit dispersion, issuer spread premiums, and opportunity sets.

Dispersion in two perspectives

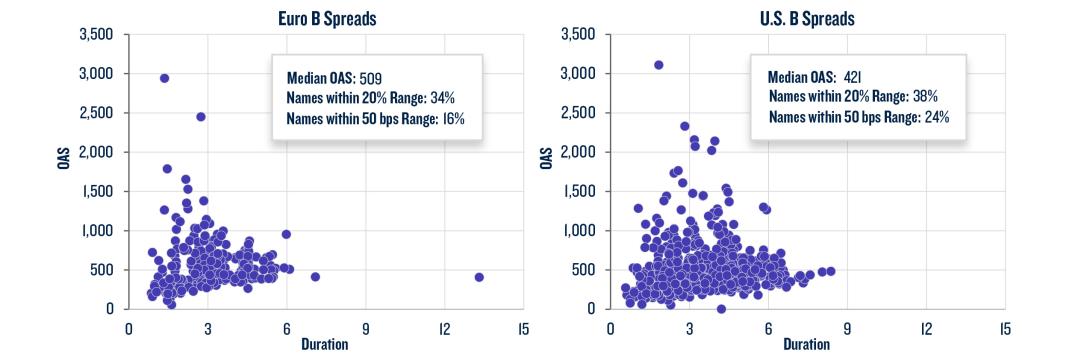

Although the chart on the right of Figure 1 shows that the relative value between the U.S. and European markets is near a point of balance, the latter’s usual long-term structural cheapness is also apparent. Greater dispersion amongst issuers and credit spreads is one of the contributing factors to that cheapness. Figure 2 shows the greater dispersion in European B rated spreads vs. those in the U.S., particularly in those further from the median. For example, although both markets had a similar grouping of names within 20% of the median, the European market had notably fewer within 50 bps of the median, indicating less concentrated grouping.

Figure 2: Dispersion in the European market is further afield than in the U.S.

Source: PGIM Fixed Income as of February 23, 2023. Spreads are based on single B high yield.

The implications of greater dispersion can be seen from two related perspectives. The first being that it reflects distortions that exist in individual credits (e.g., in business objectives or financial stability) after years of operating amidst the deluge of central bank liquidity. The second indicates an expanded field of potentially attractive issues.

In a logical progression, the breadth of dispersion also points to the stark dichotomy between potential winners and losers amongst names with attractive spread levels. Therefore, distinguishing the troubled names from those with the potential to contribute to alpha generation indicates the need for thorough, ongoing credit research.

Global analysis for global issuers

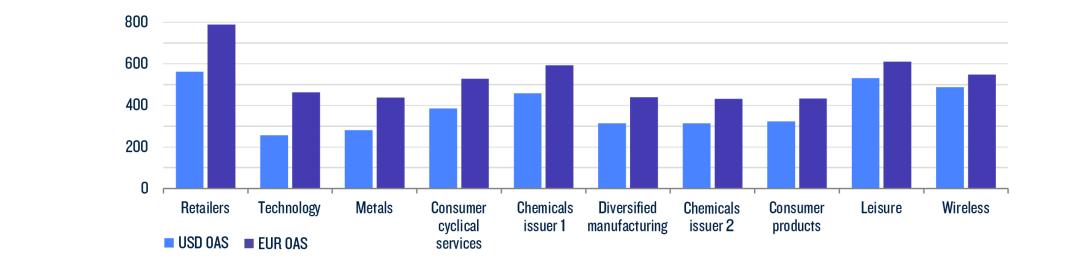

Names amongst the outliers in Figure 2 likely include reverse Yankee issuers (U.S. domiciled names issuing in euros or gilts), which may enter the market for a variety of reasons—such as diversifying their investor base—but at a cost. In late 2022, we conducted an analysis of 10 names from an array of industries that issued debt in a range of structures in the U.S. and European markets (Figure 3). We found the euro offerings were an average of 181 bps wide of the offerings in the U.S. with some premiums reaching as high as 271 bps.1

Figure 3: PGIM Fixed Income’s analysis of high yield reverse Yankee spread premiums (basis points)

Source: PGIM Fixed Income. Analysis conducted in November 2022.

Although the bonds in the analysis have identical credit risk, the spread differential is driven by a combination of a lack of resources to analyse the breadth of U.S. issuers—prompting many European investors to avoid the opportunity set—and the lower liquidity levels in the European market. Yet, the compelling opportunities amongst reverse Yankee premiums presents another benefit for investors with the global research to cover transactions across regions.

An expanded playing field

In addition to the attributes above, a global high yield strategy is complemented by the depth of an expanded opportunity set (as well as the respective credit dislocations) in the U.S. and beyond. Figure 4 shows that the market value of the global high yield universe is several times larger than the European domestic market, depending on whether emerging market high yield credits are included. Furthermore, investors stand to pickup sizable increases in spread and yield when investing on a global basis.

For reference, the yields in Figure 4 represent increases of about 250-275 bps from a year earlier, and in an environment where yield may be considered destiny, the increased yields bode well for sector returns going forward.

Figure 4: A global opportunity set that can expand by four to five times for European investors

Source: PGIM Fixed Income and ICE BofA as of March 3, 2023. *Referenced spread is option adjusted spread over government interest rates.

Source: PGIM Fixed Income and ICE BofA as of March 3, 2023. *Referenced spread is option adjusted spread over government interest rates.

The implications from mixed economic outlooks

At this point, investors have their pick of global fixed income strategies with yields that are notably higher than a year earlier. Thus, they need to consider the sectors that may be appropriately suited to their objectives. For those with a total return emphasis, our macro scenarios continue to support the benefits of a global high yield allocation.

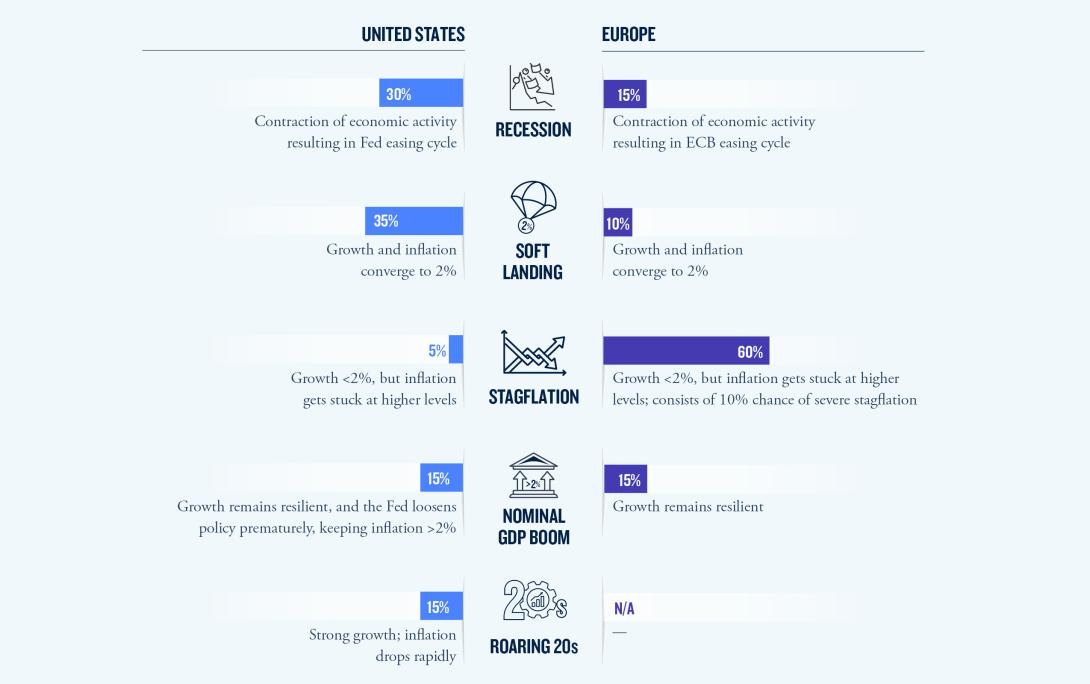

Although a slew of negative risks remains on the horizon, recent developments warrant consideration as well. For example, surging inflation has been softened by cooling goods prices, slowing growth in China has been countered by its shift away from zero-COVID measures, Europe’s current energy crisis has been mitigated (for now) by warm winter weather, and broad tightening in monetary policies has thus far been met with resilient economic activity. The mix of factors culminates in the scenarios described in Figure 5.

Figure 5: PGIM Fixed Income’s central macroeconomic scenarios (% chance of each scenario playing out)

Source: PGIM Fixed Income.

In the U.S., we assign equal probabilities to a recession and a soft landing with weighting potentially skewed to the latter as the demand for labour remains historically high. The soft-landing scenario (i.e., with inflation retreating towards the Federal Reserve’s 2% target) could support the asset class—which represents ~75% of the Global High Yield universe—given the likelihood that long-term interest rates and credit spreads remain elevated enough to provide attractive levels of income. Even in a recession outcome, whilst spreads may widen for a short period, rates would likely rally and bolster the prospects for a positive total return.

Europe faces more “imported inflation” due to the effects of higher energy costs on goods prices, which is more difficult for the European Central Bank to control. Hence, our base case points to stagflation as policy rate increases cool demand and inflation remains elevated. Although our base case suggests risk assets have near-term downside, this is somewhat cushioned by the level and dispersion in European credit spreads (again, see Figure 2).

While investors tend to focus on the up-and-down movement in interest rates and spreads, the current macro configuration also lends itself to the possibility of a rangebound outcome. In a scenario where rates and spreads generally move sideways, the elevated yields and the income-related returns across the high yield universe would be another factor supporting performance across the sector (again, see Figure 4 for the year-over-year change in yields).

As a concluding thought regarding the implications of our scenarios, the potential for recession and/or stagflation has historically alluded to an uptick in defaults, therefore contributing to a volatile stretch for high yield. However, the credit cycle encompassing COVID and the consequent recovery benefitted corporates by lowering borrowing costs, supporting valuations, and boosting profitability (amongst other factors), which means that corporate balance sheets enter a period of potential stress in solid shape with strong liquidity.

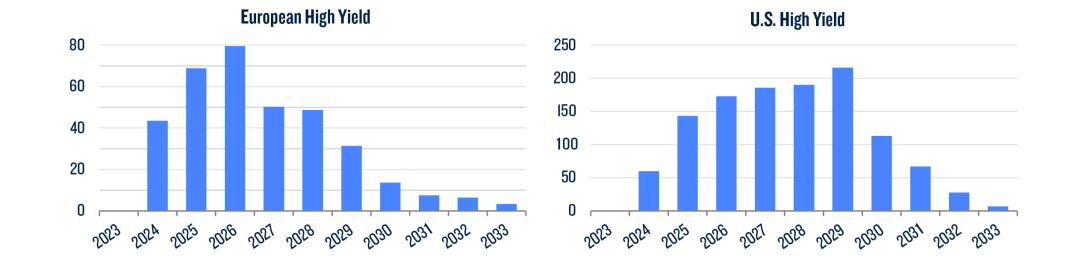

This underscores the improving quality of the global market in recent years as the BB component rose to more than 54% of the market in mid-February 2023 from about 48.5% a decade earlier. The improving quality has been partially driven by smaller/more speculative credits gravitating toward leveraged loan financing. Furthermore, the global high yield market should benefit from the lack of a maturity wall through 2024 with refinancing needs likely to peak in 2026 and 2029 in Europe and the U.S., respectively (Figure 6). Therefore, in a recessionary scenario, four-year default rates would likely remain less than 12-15% in the U.S. and Europe, i.e., average annual defaults reaching about 3-4%. These rates are in line with, or below, historic medians and far below the levels from the financial crisis cycle of 2008-09 or the pandemic cycle of 2020-21.

Figure 6: The lack of near-term maturity walls support low defaults in 2023 (high yield bonds maturing by year; LHS: € billions; RHS: $ billions)

Source: PGIM Fixed Income and Barclays as of December 31, 2022.

Conclusion

The benefits of a global high yield strategy extend from the tactical to the structural. In addition to benefitting from changes in economic paths and relative value dynamics, active global strategies maintain the flexibility to capitalise on nuances that extend across regional markets.

When viewing the sector from a total-return perspective, the prior increases in interest rates and credit spreads will remain important aspects going forward. In the event of stagflation, spreads and rates have already repriced to some effect, thus likely cushioning some of the blow, whereas a recession could coincide with a decline in rates, thus offsetting some of the volatility in credit spreads. In a case where rates and spreads move sideways, the sector should generate attractive levels of income, an outcome where rates remain near their peaks and credit spreads contract may enhance the sector’s total-return potential.

A global perspective provides a fitting conclusion to our European high yield series. Although the asset class represents a specific area of the capital markets, its attributes are capable of meeting the varied needs of investors across the globe, and it remains an asset class to keep front of mind amidst quickly evolving conditions throughout global markets.

Read More from PGIM Fixed Income

1 The spread differential is based on cross currency basis, option-adjusted spreads.

Source(s) of data (unless otherwise noted): PGIM Fixed Income as of February 2023.

For Professional Investors only. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. All investments involve risk, including the possible loss of capital.

PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.

These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. PGIM Fixed Income as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Investors seeking information regarding their particular investment needs should contact their own financial professional.

These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy.

Any forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fee. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government agency or private guarantor, there is no assurance that the guarantor will meet its obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss.

In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a Singapore investment manager registered with and licensed by the Monetary Authority of Singapore. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 (paragraph (a) to (i) of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 - Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3.

© 2023 PFI and its related entities.

2023-1823

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in