The Future Of Fixed Income: How Technology Will Revolutionize Asset Management

IN THIS PAPER - Fixed-income investing hasn’t kept up with the rapid pace of technological innovation in the rest of the financial industry. But that’s about to change. Machines will empower humans to achieve unique insights and act faster in a market where speed and alpha are inextricably linked.

The Digital Revolution Is Coming To Fixed Income

Artificial intelligence, automation and predictive analytics are transforming virtually every industry, but bond investing hasn’t really changed. The typical investment process is inefficient, from research and portfolio construction to trading. But this story will change as human and machine join forces.

In the next few years, we expect the rise of fixed-income technology to open a wide gulf in performance between those managers who have integrated cutting-edge tools into every stage of their investment processes and those who haven’t.

In the past, the quest for excess return (alpha) was dominated by either the superhuman bond investor who attempted to single-handedly navigate global markets or the quantitative shop that could exploit inefficiencies in the short term but couldn’t see the bigger picture.

In an information-heavy world, just sticking with the status quo won’t be good enough. It’s imperative to integrate technology into the investment process to provide managers with tailored information that enables faster decision-making, makes every step of the process more efficient, and provides a more complete picture of risk and opportunity.

Several firms have used a “best of breed” strategy, creating or sourcing individual tools to help in one specific area of investing, such as research, trading or portfolio management. That’s a good start, but to stay ahead, firms will need to focus on how these tools work together to create an ecosystem that magnifies the human impact.

BUILDING LIQUIDITY: TURNING PUDDLES INTO POOLS

Liquidity is the number-one issue influencing a fixed-income manager’s ability to create alpha. Firms that can’t effectively assess a bond’s liquidity won’t be able to implement their investment ideas. And if a trade can’t be implemented, there’s no way it can make money.

“Liquidity pools,” or markets that provide liquidity for credit securities, have long been highly fragmented across multiple external third-party sources. The information provided by these sources is valuable, but it’s inefficient to continually monitor each one and then compare and contrast the data.

To keep up in a marketplace that will digest and react to every new bit of information faster and faster, successful fixed-income managers will need to use technology that pulls all external fixed- income trading platforms together in one place. Firms that adopt this technology can become price makers instead of price takers, resulting in better executions, lower transaction costs and faster investment of new cash inflows.

These kinds of trading platforms aren’t theoretical anymore.

In 2016, we developed ALFA (Automated Liquidity and Filtering Analytics) with this need in mind. By aggregating separate pockets of existing market data into a single user interface and enabling our traders to filter by specific identifiers or security characteristics, ALFA helps AB traders make better, more informed decisions on the price levels at which less liquid and illiquid securities should trade. The objective is to be able to buy bonds for clients’ portfolios at the lowest price and sell them at the highest price.

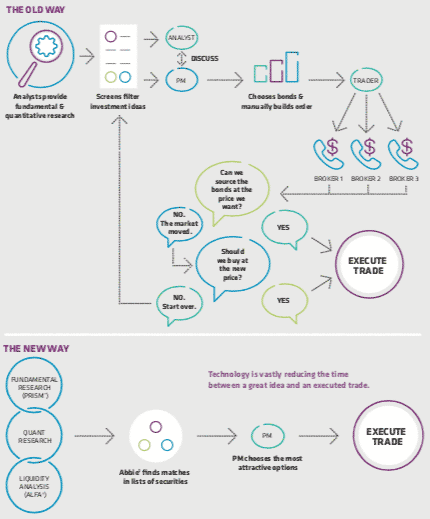

ALFA can also alert our traders when certain market events occur. In February 2017, for example, ALFA flagged to one of our emerging- market debt traders that an unusually high number of dealers were offering bonds issued by the Brazilian Development Bank (BNDES), one of the largest development banks in the world. Our trader took a closer look at the offers and discovered that BNDES was trading at a lower valuation than the bonds of another large Brazilian bank, Caixa Econômica Federal (CAIXBR), which we deemed to be a fundamentally weaker credit.

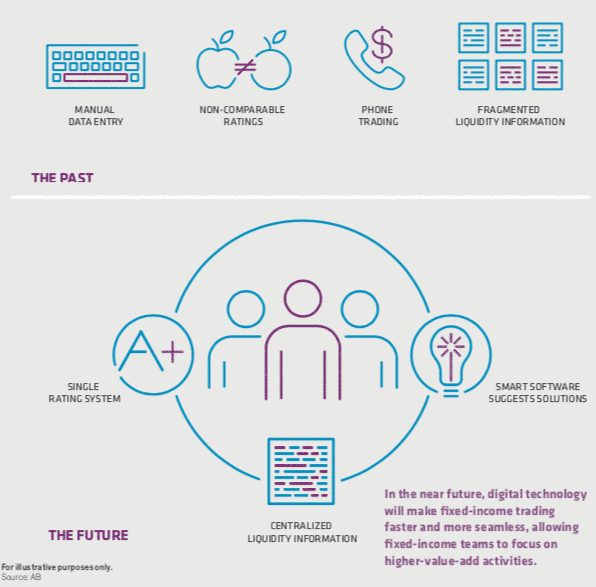

STILL TRADING LIKE IT'S 1989

For many fixed-income managers, technology is stuck in the land that time forgot. Roughly 80% of US corporate bond trades, measured by notional value, are still executed over the phone. The biggest innovation in credit research until very recently? Microsoft Excel. And that was back in 1985.

While the rise of electronic trading platforms has increased market efficiency for smaller trades, larger trades—both notionally and in terms of the number of line items—can take anywhere from several hours to several days. Electronic trading platforms get the best trade execution when the request is for less than $1 million per bond and for fewer than 30 bonds. Even then, fulfilling each list can take up to an hour from start to finish.

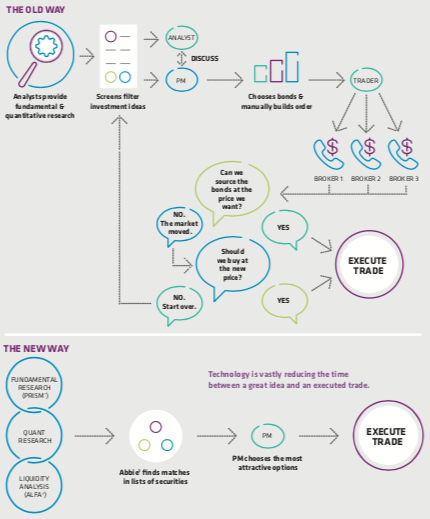

Then there’s the inefficiency of the investment process itself, which has looked something like this for the last few decades (Display 1):

Step 1: A research analyst develops a differentiating view on a credit and discusses it with a portfolio manager (PM), weighing the positives and negatives and a range of potential outcomes. This takes a lot of back and forth, because most of the facts reside within the analyst’s head or in a desktop spreadsheet.

Step 2: The PM also needs to incorporate inputs from other research teams, such as regional, macro or quantitative analysts. There may be discrepancies among the teams, forcing the PM to engage in more back and forth to gain confidence in the buy or sell decision.

Step 3: Here is where the process can break down further. The PM asks the trader to buy XYZ bond, but the market has already moved or liquidity in the bond has dried up. That means going back to square one.

Multiply this process across the hundreds of securities in a typical bond portfolio and the inefficiencies add up. Things take a lot longer—and timing is everything when yields and liquidity are low. The process also consumes resources and bandwidth that could be directed toward activities that improve outcomes.

Display 1: From Idea To Trade – A Shorter, Simpler Path

For illustrative purposes only. | Source: Alliance Bernstein (AB)

* See page 13 | † See page 12 | ‡ See page 14

Our trader quickly worked with our banking analyst to frame our combined fundamental and valuation view, and together they presented their recommendation to the PM. We capitalized on the dislocation: AB purchased BNDES in expectation of the market normalizing. It did so within six weeks, a boon for our clients, who were able to buy low and sell high (Display 2).

Display 2: Seizing An Opportunity In An Undervalued Credit

For illustrative purposes only. | Source: AB

AB recently partnered with Algomi,1 a financial technology firm, to commercialize the data aggregator component of ALFA. As other firms adopt this technology, fixed-income markets will become more stable, transparent and efficient, which in turn should enhance overall market liquidity. That will benefit all investors trading in today’s less liquid world—a world in which even relatively small events can create huge changes in prices very quickly.

ONE-TOUCH ACCESS TO CREDIT RESEARCH

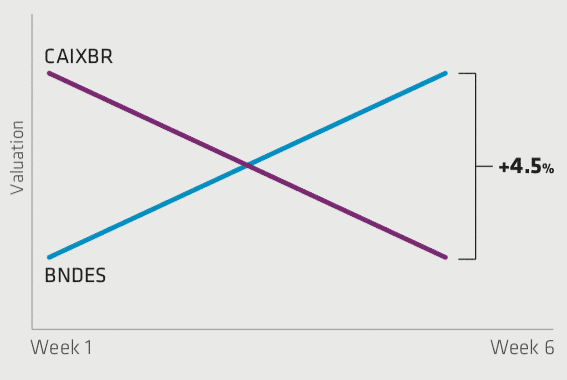

Getting a faster and more accurate picture of market liquidity is just the beginning. To generate better returns for clients, firms need to know not only which bonds are available in a market, but also which bonds are attractive (Display 3). Buying just any bond doesn’t improve performance—it has to be a bond that helps achieve a portfolio’s strategic goals.

Display 3: Technology Plays Matchmaker

For illustrative purposes only. | Source: AB

Firms that digitalize and centralize information can both identify the right bonds and take advantage of pockets of liquidity to buy them in sufficient quantity. PMs and traders no longer need to track down individual analysts to get their views. Fundamental credit research and rating processes need to live in a consistent, accessible framework. That way, traders and PMs can grasp at a glance an analyst’s assessment of a bond’s risks and opportunities and more easily compare assessments of two or more similar bonds.

This ability was the goal when AB rolled out the Prism credit rating and scoring system in 2016. With Prism, our credit analysts can share their views on individual issuers in a consistent, comparable, quantifiable way across industry sectors, ratings categories and geographies. Analysts evaluate each company on several key business-related and governance/structure-related dimensions, resulting in the final proprietary credit rating for the issuer.

Any fixed-income PM or analyst at the firm can access Prism from a desktop, getting a concise overview of our analysts’ recommendations for each company, including a summary investment thesis and a graphical depiction of the company’s score on more than 20 specific risk factors. With Prism’s consistent framework, we can quickly and effectively compare the merits of similar issuers during portfolio construction.

The goal, of course, is straightforward: better and faster information should empower better decisions and result in stronger portfolios.

BRINGING IT TOGETHER: INTEGRATING ARTIFICIAL INTELLIGENCE TO CREATE REAL ALPHA

Finally, in order to fully harness technological advances to build better portfolios and maximize the generation of alpha, silos have to be dismantled. Firms need to integrate research and trading platforms so the entire investment team can tap into shared knowledge and insights on individual bonds (Display 4).

Display 4: Going Digital – Bringing Fixed Income Into The 21st Century

When credit research views and pricing/liquidity data reside on a single platform, they provide a more complete picture of an issuer and can interact with and play off each other, to tremendous effect. Take for example a tool that can communicate both with research systems to understand what research analysts find attractive, and with liquidity and pricing tools to know what’s available at any given time. We created that technology, and her name is Abbie.

Abbie is a virtual assistant that works with our PMs, assistant PMs and traders. Originally, “she” started out as a chatbot that could be directed to build orders more quickly and with fewer errors than a human, who is prone to fat-thumb mistakes even when he or she is being extremely careful.

Just as humans get better at their jobs, Abbie is constantly learning new skills with the help of our talented developers and investment teams. We’ve taught her to “read” research ratings on Prism and liquidity information on ALFA to help our professionals generate lists of bonds that meet the standards of research analysts and are available to buy at an attractive price. These lists can serve as starting points for analysts and PMs, who can then dedicate more time to decisions that add value.

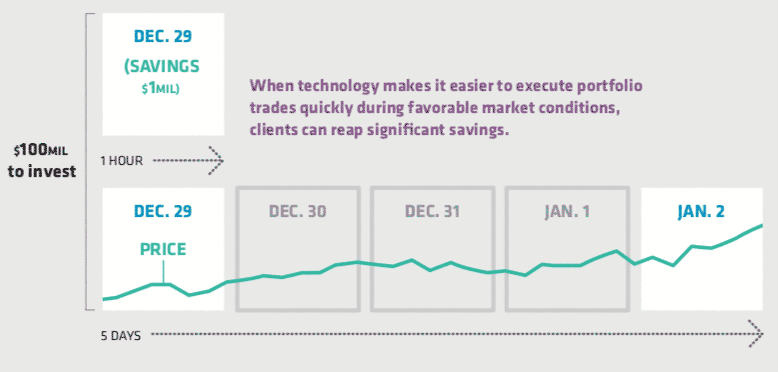

For example, Abbie’s true value becomes apparent if you consider what happened on December 29, 2017, the last business day of the year. Our high-yield portfolio received a $100 million inflow that our PMs wanted to put to work. Investing such a sum would typically require buying between 100 and 300 bonds, which would historically take hours or even days of discussions between PMs and analysts, and as many as 200 phone calls by our traders to check the availability of potential investments. Using traditional technology and investment processes, it would have been extremely unlikely that we could come to market on our clients’ behalf before year-end.

Our investment professionals didn’t have to wait to act, however. They scoured Prism and ALFA for opportunities, directed Abbie to build the appropriate orders, and executed a trade for a basket of securities the same day. As a result, they were able to obtain the bonds they wanted for $1 million less than they would have had they waited until January 2, 2018, the first business day of the new year (Display 5).

Display 5: Putting $100 Million Into The Market – Five Days vs. An Hour

For illustrative purposes only. | Source: AB

Abbie has learned a lot since then. Had this event happened today, she would be able to work even faster. Given a set of parameters from our investment professionals, she could comb through ALFA and Prism on her own and suggest securities to buy, giving our professionals more time to think about how each investment fits their broader strategic goals.

In the future, she might alert our investment professionals to new inflows and analyze portfolios on her own to generate an initial list of potential investments. Or she might see a great opportunity on ALFA that screens well on Prism and proactively nudge our investment staff to look into it. Once she gets smart enough to understand trading parameters, she may even trade with bots just like her at other financial institutions.

She’ll also monitor activity in portfolios, looking for unusual behavior that could indicate that a human had made a mistake. One day, she may even answer simple questions for our clients about their exposure to certain credits or risks. Humans will always retain control over key decisions and complex client interactions, but Abbie can give them a head start and, in some cases, a range of options to consider.

THE COMING AGE OF THE “IRON MAN” AND “IRON WOMAN”

Technology is undoubtedly changing fixed-income markets, and firms that ignore this fact do so at their peril. But technology isn’t a panacea. The firm with the shiniest, most expensive technology isn’t destined to lead the pack. It’s not how much tech you have but how you use it that really matters.

So what’s the right way to use it? As we see it, the future of alpha generation in fixed income is a team of talented humans augmented with smart machines–“Iron Men” and “Iron Women”. Start with talented portfolio teams and arm them with the technology they need to find better bonds, build better portfolios and deliver better outcomes.

The time is ripe for augmented human intelligence. Central bank tightening is unleashing greater volatility—and therefore, greater opportunity—into the market. But it can also cause markets to seize up suddenly, leaving bond managers who aren’t prepared stuck in positions their clients would prefer to be out of. Managers will need to deploy technology to monitor every corner of the market every minute of every day, uncovering and quickly acting on unexpected opportunities.

FASTER, SMARTER, MORE FLEXIBLE: HOW FIXED-INCOME INVESTORS WILL WIN IN THE DIGITAL AGE

The advanced fixed-income investor of tomorrow will capitalize on the division of labor between human and machine. Computers will crunch mountains of data at breakneck speeds and instantly tease out patterns from a swirl of numbers. Humans will do the abstract thinking and high-level strategy planning that’s still very hard to code—and they’ll have more time to do it.

But this synergy is really just a means to an end. The end result is the ability to get to market and execute faster, to integrate and leverage unique investment insights—even when markets are frozen in shock—and to convert the benefits of the combination of man and machine into the following tangible benefits for investors:

- Better, faster bond selection. By centrally integrating the collective insights of teams of expert credit-research analysts and by evaluating bonds within a consistent framework that puts everything on a level playing field with explicit numerical comparisons, bond managers will be vastly more effective in selecting which bonds to buy and sell.

- Capturing more buy/sell opportunities. In the post-crisis era, liquidity is scarce, and even relatively small events can freeze bond markets. Even under normal conditions, a bond that appears available can disappear moments later, and the appetite for a particular security can fade just as fast. With a centralized feed of market liquidity information and a combination of machine and human intelligence to monitor that feed, investment professionals will have an edge when it comes time to grab a coveted bond or unload one that no longer serves the portfolio. That ability will be especially critical during a liquidity crunch, when the first to transact often wins.

- Getting the best prices. Under scarce liquidity conditions, tools that can survey the entire bond market won’t just help investors find the bonds they need. They’ll also help investment professionals ensure they’re getting the best prices without having to spend precious hours calling multiple brokers for quotes.

The direct effects of tools like ALFA, Prism and Abbie are exciting enough, but things really start to get interesting when one considers the second-order effects of a more thorough, efficient investment process:

- Empowering humans to spend more time finding differentiated insights. If one of the biggest benefits of a more efficient investment process is that it gives talented humans more time to do the things machines cannot, the logical next question is: What exactly are those things? For an investor, the most important thing technology can do is free human investment managers to ask the right questions in the right places.

Machines are great at spotting patterns in and teasing out predictions from mind-bogglingly huge data sets, but the output is only as good as the input. It’s up to humans to find new, unique sources of data and, in many cases, to figure out how to ask machines to analyze that data in clever ways that competitors haven’t thought of yet. It gives them time to try out more hypotheses and run more models.

That’s not to say that all data comes in binary code, of course. When the investment process is more efficient, it gives analysts and PMs more time to meet with humans who may also have differentiated insights: the officials who run municipalities and foreign Treasuries, for example, or the management teams running companies of all sizes. All of this translates into better odds for creating alpha.

- More time for investment professionals to interact with clients. Investment teams have many priorities, but client interaction should always be one of the most important. Investors’ priorities are always shifting, and it’s up to an investment manager to ensure that he or she not only understands those shifts, but also that the investor feels comfortable with the strategy his or her manager is pursuing. That means answering questions at all hours about performance, how market events affect positioning, and a portfolio’s exposure to the megatrends shaping the world economy. But this isn’t a one-way street. Clients and investment managers often work closely together to design and develop new investment solutions. More time to devote to such creative partnerships can pay real dividends.

- Lower overall trading costs. A more efficient investment process will ultimately result in savings for investors. While growth in assets typically results in higher trading costs and the need for additional personnel, technology pushes costs in the other direction.

Bond investors face a perfect storm of more regulation, less liquidity, more competition and the next phase after a decades-long bull market. To deliver alpha in a low-liquidity, low-yield environment, humans and machines will need to work more closely than ever to plumb every liquidity puddle, instantly compare opportunities, gauge pricing on less-liquid securities and predict changing liquidity—and do so faster and more efficiently.

By this point in the digital age, the consequences of not adopting an Iron Man or Iron Woman mind-set are clear. It’s like standing out on the street in the pouring rain trying to hail a cab instead of ordering a ride-share service. Or searching through a library card catalog for a book that will answer a question instead of asking a virtual assistant. Like carrying dozens of paper maps in the glove box instead of getting the fastest route through traffic from a mapping app.

For a long time, fixed-income investors were stuck with these kinds of low-efficiency choices by default. Now, they have options. And with those options comes the need for a different mind-set. Creating alpha is no longer just about who has the most intelligent humans or the most advanced quant algorithms. It’s about both of those things, as well as a process that incorporates technology at every turn to enable humans to make smarter, faster investment decisions. It’s about choosing a firm that has a track record of innovating to solve thorny problems and that empowers its employees at every level to contribute ideas that will lead to even more innovation in the future.

The future–let’s dwell there for a moment. We’re used to a world in which machines are programmed to do the things we want them to do. Already, however, machines fed a steady diet of data are starting to learn things on their own. And they’ll get even smarter and faster. They’ll start teaching us things. Who will capitalize on that? Who will know how to deploy new capabilities we can’t yet imagine with the right mix of caution and gusto? The firms that have enthusiastically and intelligently incorporated technology into their DNA. The firms that have a vision for how their people will work alongside their machines now and in the future.

Technology will never solve all our problems, and a human hand should always remain on the wheel. But what technology can do is make investors smarter, faster and more creative if they know what to do with it.

CHECKLIST: IS YOUR ASSET MANAGER READY FOR THE DIGITAL FUTURE?

Wondering whether your asset manager has the right technological tools and innovative attitude to succeed in the fixed-income world of the future? Here are some questions to ask to gauge his or her preparedness.

- In the last five years, how, specifically, has technology changed the way you do business? What changes are you contemplating for the next five years? Your asset manager should be able to provide specific examples of how they have improved client outcomes using technology they built or bought. They should also have an explicit technology strategy that anticipates new developments in artificial intelligence, machine learning and fixed-income market conditions.

- Can you describe your organization’s culture and attitude toward technology? An organization that truly values technology should have a track record of integrating technology into its investment process, as well as a bottom-up approach to innovation in which the people who encounter everyday problems and inefficiencies are empowered to suggest new technological solutions. Senior management should view fixed-income technology as a top priority.

- What problems are your most compelling technology tools solving? What problems do you think technology can solve in the future? Technology is a way to develop an edge in the marketplace, not on the bottom line. The end goal of integrating technology into the investment process should not be a headcount reduction. Technology should be solving the real-world problems that impede the best client outcomes.

- What is your organization’s approach to the changing liquidity conditions in the marketplace? When liquidity is fleeting and scarce, seconds can matter. If firms don’t see liquidity conditions as a problem with a potential technological solution, they’re going to be left out in the cold the next time markets seize up.

- Do you see your tools as standalone improvements or as part of a more holistic strategy? Standalone improvements are commendable, but the real value to an investor lies in tools that can “talk” to one another. Now that artificial intelligence and machine learning are upon us, firms should have either digitized all their data into machine-readable formats or have a plan for doing so. This is the first step toward developing a technology suite that is more than the sum of its parts.

- How do you think the interaction between man and machine will evolve at your organization over the next five years? Too often, technology is presented as an alternative to human intelligence rather than as a way to empower it. Firms should have a clear answer as to how machines will empower their existing employees and what new talent they will be looking to hire in the future as their needs evolve.

- Name three of your developers. A sure sign that technology is fully integrated into the investment process? Your PM consults developers so frequently to solve research and investment problems that he or she knows exactly who they are.

By AllianceBernstein

Gershon M. Distenfeld, Co-Head—Fixed Income; Director—Credit

Scott DiMaggio, Co-Head—Fixed Income; Director—Global Fixed Income

Jeff Skoglund, Chief Operating Officer—Fixed Income

James Switzer, Head—Credit Trading

1Algomi was founded in 2012, and through its Honeycomb, Synchronicity and Algomi ALFA technology, creates the bond information network that enables all market participants to securely and intelligently harness data to make valuable financial trading connections. Algomi has 120 employees with offices in New York, London and Hong Kong.

NEW YORK 1345 Avenue of the Americas | New York, NY 10105 | (212) 969 1000

LONDON 50 Berkeley Street | London W1J 8HA | United Kingdom | +44 20 7470 0100

SYDNEY Level 32, Aurora Place | 88 Phillip Street | Sydney NSW 2000 | Australia | +61 2 9255 1200

TORONTO Brookfield Place | 161 Bay Street, Suite 2700 | Toronto, Ontario M5J 2S1 | (416) 572 2534

TOKYO Hibiya Park Front Building 14F 2-1-6 | Uchisaiwaicho, Chiyoda-ku Tokyo 100-0011 | Japan | +81 3 5962 9000

HONG KONG 39th Floor | One Island East Taikoo Place | 18 Westlands Road | Quarry Bay, Hong Kong | +852 2918 7888

SINGAPORE One Raffles Quay | #27-11 South Tower | Singapore 048583 | +65 6230 4600

Past performance, historical and current analyses, and expectations do not guarantee future results. There can be no assurance that any investment objectives will be achieved. Diversification does not eliminate the risk of loss.

Important Note: Investing in the bond market is subject to risks, including market, interest-rate, issuer, credit, inflation and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low-interest-rate environment increases this risk. Note to All Readers: The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates. Note to Canadian Readers: This publication has been provided by AB Canada, Inc. or Sanford C. Bernstein & Co., LLC and is for general information purposes only. It should not be construed as advice as to the investing in or the buying or selling of securities, or as an activity in furtherance of a trade in securities. Neither AB Institutional Investments nor AB L.P. provides investment advice or deals in securities in Canada. Note to European Readers: This information is issued by AllianceBernstein Limited, a company registered in England under company number 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA–Reference Number 147956). Note to Readers in Japan: This document has been provided by AllianceBernstein Japan Ltd. AllianceBernstein Japan Ltd. is a registered investment-management company (registration number: Kanto Local Financial Bureau no. 303). It is also a member of the Japan Investment Advisers Association; the Investment Trusts Association, Japan; the Japan Securities Dealers Association; and the Type II Financial Instruments Firms Association. The product/service may not be offered or sold in Japan; this document is not made to solicit investment. Note to Australian Readers: This document has been issued by AllianceBernstein Australia Limited (ABN 53 095 022 718 and AFSL 230698). The information in this document is intended only for persons who qualify as “wholesale clients,” as defined in the Corporations Act 2001 (Cth of Australia), and should not be construed as advice. Note to Singapore Readers: This document has been issued by AllianceBernstein (Singapore) Ltd. (“ABSL”, Company Registration No. 199703364C). ABSL is a holder of a Capital Markets Services Licence issued by the Monetary Authority of Singapore to conduct regulated activity in fund management and dealing in securities. AllianceBernstein (Luxembourg) S.à r.l. is the management company of the portfolio and has appointed ABSL as its agent for service of process and as its Singapore representative. This document has not been reviewed by the MAS. Note to Hong Kong Readers: This document is issued in Hong Kong by AllianceBernstein Hong Kong Limited (聯博香港有限公司), a licensed entity regulated by the Hong Kong Securities and Futures Commission. This document has not been reviewed by the Hong Kong Securities and Futures Commission. Note to Readers in Vietnam, the Philippines, Brunei, Thailand, Indonesia, China, Taiwan and India: This document is provided solely for the informational purposes of institutional investors and is not investment advice, nor is it intended to be an offer or solicitation, and does not pertain to the specific investment objectives, financial situation or particular needs of any person to whom it is sent. This document is not an advertisement and is not intended for public use or additional distribution. AB is not licensed to, and does not purport to, conduct any business or offer any services in any of the above countries. Note to Readers in Malaysia: Nothing in this document should be construed as an invitation or offer to subscribe to or purchase any securities, nor is it an offering of fund-management services, advice, analysis or a report concerning securities. AB is not licensed to, and does not purport to, conduct any business or offer any services in Malaysia. Without prejudice to the generality of the foregoing, AB does not hold a capital-markets services license under the Capital Markets & Services Act 2007 of Malaysia, and does not, nor does it purport to, deal in securities, trade in futures contracts, manage funds, offer corporate finance or investment advice, or provide financial-planning services in Malaysia. Important Note for UK and EU Readers: For Professional Client or Investment Professional use only. Not for inspection by, distribution or quotation to, the general public.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P. © 2018 AllianceBernstein L.P., 1345 Avenue of the Americas, New York, NY 10105

181001115841 | FIX–7718–1018 | www.AllianceBernstein.com

ABOUT AB

AllianceBernstein (AB) is a leading investment-management firm with over $550 billion in client assets under management. We provide a forward-looking perspective, independent research and investment discipline across all asset classes, leveraging our extensive forward-looking footprint built over five decades. Our collective insights drive innovation and lead to better outcomes. Every day, we work with clients to earn their trust, move their vision forward and help keep them AHEAD OF TOMORROW.®

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in