The Implications of China's Far-From-Typical Recovery

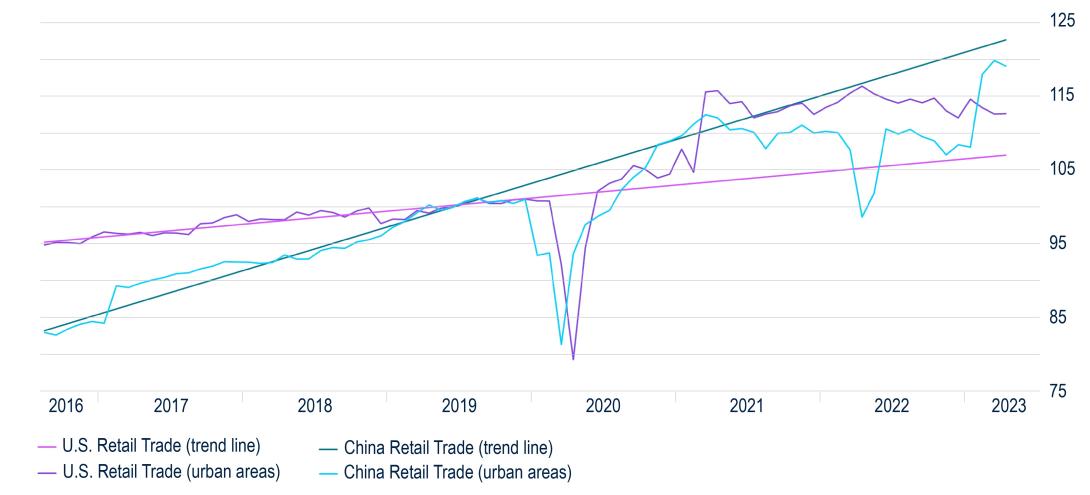

As the global economy lurched from crisis to crisis over the prior decades, China provided a significant source of growth that helped limit the depth and/or the duration of the contractions. However, China's current recovery is emerging unlike its others—a development underscored by this week's cut in key lending rates, the prospects of which we previously flagged —leaving the global economy without the familiar engine to pull it forward as recession concerns linger throughout much of the world.1 China’s traditional method of boosting growth when needed or desired (e.g., after the global financial crisis of 2008) produced beneficial ripple effects throughout the global economy. China opened the credit spigot in order to boost public and private investment, the latter of which was particularly concentrated in real estate. The hard commodities and capital goods needed to drive these investments consequently provided a lift to commodity exporters, such as Chile, Brazil, and Australia, as well as capital goods exporters, such as those in Germany and Eastern Europe. China’s current recovery is taking an entirely different shape. The country is not only experiencing diminishing returns from its investment-driven model (more on that below), but it is also facing the end of the global lockdown-related export boom. As a result, this recovery will increasingly rely on the Chinese consumer. However, recent data show that the rebound in real retail sales activity is already stalling and still far below the pre-2020 trend—the exact opposite of the U.S. recovery (Figure 1).

Figure 1: The Stalling Revival in China's Retail Activity (indexed to 100 as of July 2019)

Source: PGIM Fixed Income and Macrobond. This contrast is not surprising, given that Chinese consumers received far less stimulus support than U.S. or European households, and their limited resources underscore the altered state of China’s current recovery.

The Global Effects

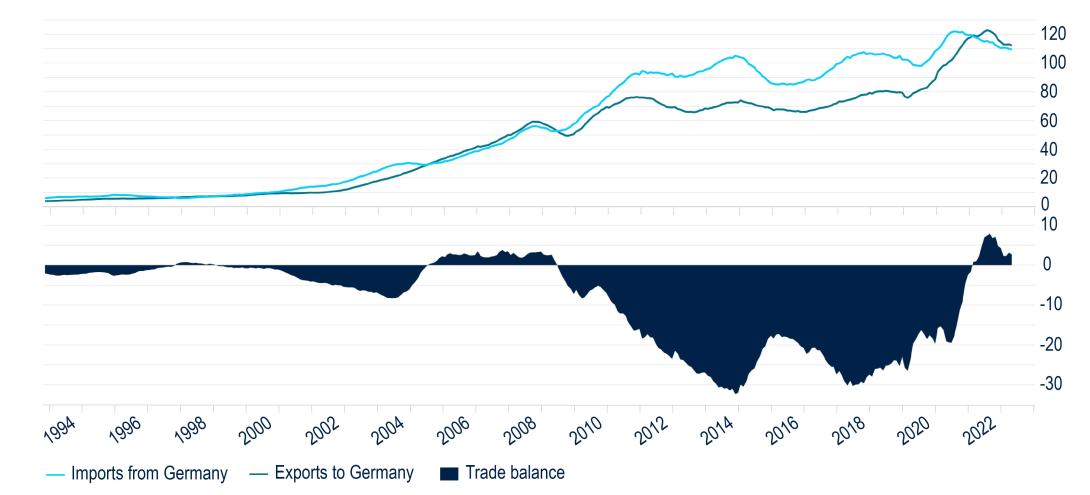

The muted increase in China’s consumer activity has been accompanied by a moderation in its traditional investment indicators, such as demand for hard commodities including copper, iron ore, and cement, as well as its trade activity with Europe. For example, Figure 2 shows that as China’s trade volume with Germany has rolled over, its trade balance with Germany has flipped to a surplus—meaning that Germany’s balance has flipped to a deficit. A significant reduction in auto exports to China is playing a notable role in the trade deficit, especially amid the surge in China’s electric vehicle sales domestically and abroad.

Figure 2: The Changed Trade Dynamic Between China and Germany (USD in billions)

Source: PGIM Fixed Income and Macrobond. While China’s consumers may provide some support for crude oil and food commodities, their focus on real estate investments may have also run its foreseeable course. After years of emphasis, Chinese households own the most property on an internationally comparative basis, and, consequently, the country’s property market became the world’s most expensive.2 Given the sustainability questions arising from these real estate dynamics, China’s authorities cracked down on over-levered property investors as part of their “three red lines” policy during the height of the pandemic. That timing likely exacerbated the massive country-wide shock to the sector, putting a huge dent in consumers’ wealth perception and shattering their concept of property as a store of value. In turn, housing starts declined precipitously—a far worse performance than the U.S. housing market—representing an ongoing source of concern for investors (Figure 3).

Figure 3: Unlike the U.S., China's Housing Starts Remain in the Basement (in thousands)

Source: PGIM Fixed Income, U.S. Census Bureau, National Bureau of Statistics China, and Haver Analytics. Upon observing the scale of the carnage, Chinese authorities launched an initiative at the Communist Party Congress in October 2022 to revive the sector with various incentives. Yet, that only produced temporary improvements at the margins (i.e., the completion of previously started buildings), and demand already appears to be weakening with half of the year still to go.3 China’s property market is unlikely to receive meaningful support from the labor market, which has significantly worsened, particularly for the young and for university graduates. Indeed, the youth unemployment rate has risen to a historic peak of more than 20%—and that is before 10 million+ new graduates hit the labor market at the end of summer of 2023.4

Why Not the Tried and True?

The points above raise the question of why China doesn’t revert to its tried-and-true economic recovery methods. Broadly speaking, the shrinking returns and increasing risks from those methods have made the authorities reluctant to pursue them. Starting at the macro level, by repeatedly flooding the economy with credit, China has placed itself in a cyclical debt dilemma. A debt-to-GDP ratio of roughly 300% with an average interest rate around 5% produces an annual interest expense of 15% of GDP vs. the country’s nominal GDP growth rate in the recent range of 6%-8%. Therefore, from a fundamental credit perspective, China’s annual interest expenses are twice the level of its organic GDP growth—it’s never a great story when a borrower needs to incur additional debt just to pay its interest. That troublesome dynamic is also at the heart of our view on China’s interest-rate policy: rates will need to decline even further in order to facilitate its ongoing debt service. A reduction in interest rates consequently affects the currency exchange rate, which is already on a weakening trend, but can boost the competitiveness of Chinese exports. Moreover, given the risk of backsliding into worse-than-acceptable growth and employment outcomes, we expect the Chinese authorities to reverse course and roll out additional fiscal stimulus over the coming months. Those potential adjustments feed into our higher-than-consensus forecasts for real GDP growth of 5.7% in 2023. However, China’s medium-term growth drivers appear increasingly weak as they consist of excess manufacturing capacity and deteriorating demographics amid a rapidly aging population.5 One way to assess these growth drivers is through total factor productivity, i.e., how effectively a country uses its resources to generate growth. It’s a measure has rapidly declined in China over the past 10 years (Figure 4).

Figure 4: China's TFP Reveals an Increasingly Inefficient Use of Resources (ratio; indexed to 1 as of 2017)

Source: PGIM Fixed Income, Penn World Tables, and Macrobond. Given that the key fundamental drivers of China’s medium-term growth are weakening, our GDP forecast for 2024 indicates a moderation to 4.5% that will likely continue. Over a five-year period, the country’s growth may approach its potential at slightly less than 4%, and its growth potential may subsequently moderate to less than 3% over the coming 10 years. Turing to the geopolitical sphere, the rising tensions between China and the U.S. certainly factor into our view as well.6 Developments in the South China Sea provide an example of why we don’t see conditions improving anytime soon. If China’s leadership views the country as an emerging global power—returning to a position it held in pre-industrial times—that projection is regionally evident in its naval expansion and island building in the South China Sea, which is a major global shipping route. However, the U.S. and its regional allies continue to push back against that expansion. These unaligned views—China’s belief in its right to bolster its regional presence and the U.S. intentions of maintaining post-World War II international norms—are at the basis of these escalating tensions. In an economic context, the geopolitical strain is highlighted by the expanding technology divide between China and much of the developed world where the latter is increasingly hesitant to share advancements and data with China. Although China is a significant market, the divide exposes China’s risk of becoming a data and technology island with its attendant growth implications. When applying these considerations to investment implications, we’ll summarize the points from our recent podcast. Bonds at the sovereign/quasi-sovereign level appear overly rich, and while the corporate sector provides plenty to analyze, we’ve been very defensively positioned across our emerging market and multi-sector portfolios. As we alluded to above, we see further weakening in the Chinese yuan, hence we’re maintaining a slight underweight to the currency as well.

Source: PGIM Fixed Income, Penn World Tables, and Macrobond. Given that the key fundamental drivers of China’s medium-term growth are weakening, our GDP forecast for 2024 indicates a moderation to 4.5% that will likely continue. Over a five-year period, the country’s growth may approach its potential at slightly less than 4%, and its growth potential may subsequently moderate to less than 3% over the coming 10 years. Turing to the geopolitical sphere, the rising tensions between China and the U.S. certainly factor into our view as well.6 Developments in the South China Sea provide an example of why we don’t see conditions improving anytime soon. If China’s leadership views the country as an emerging global power—returning to a position it held in pre-industrial times—that projection is regionally evident in its naval expansion and island building in the South China Sea, which is a major global shipping route. However, the U.S. and its regional allies continue to push back against that expansion. These unaligned views—China’s belief in its right to bolster its regional presence and the U.S. intentions of maintaining post-World War II international norms—are at the basis of these escalating tensions. In an economic context, the geopolitical strain is highlighted by the expanding technology divide between China and much of the developed world where the latter is increasingly hesitant to share advancements and data with China. Although China is a significant market, the divide exposes China’s risk of becoming a data and technology island with its attendant growth implications. When applying these considerations to investment implications, we’ll summarize the points from our recent podcast. Bonds at the sovereign/quasi-sovereign level appear overly rich, and while the corporate sector provides plenty to analyze, we’ve been very defensively positioned across our emerging market and multi-sector portfolios. As we alluded to above, we see further weakening in the Chinese yuan, hence we’re maintaining a slight underweight to the currency as well.

Concluding Thoughts

As the debate and uncertainty about the direction of the global economy continues, China will no longer provide the growth engine that will pull the broader world economy out of any doldrums. In fact, over the medium term, weakening fundamentals and an emphasis on domestic consumption could well imply a pace of growth that rapidly converges with the developed world. That leads us to two further points where we would expect less change—in contrast to claims from much of the punditry. The first addresses the concept that near-shoring initiatives are on the cusp of draining China’s manufacturing demand. Although excess capacity exists, China’s economic structure has made it the world’s factory, and that won’t unravel quickly. For those pointing to other manufacturing bases, such as Vietnam or Mexico, that may experience an increase in manufacturing demand, they will consequently need to import more components from China in order to meet that demand. The second point pertains to the prospect that, over time, the Chinese yuan will usurp the U.S. dollar as the world’s reserve currency. But for any currency to do so, capital needs to flow freely. The steps that China will need to take in order to manage its debt load— notably lower interest rates with a resultant drag on the yuan—require capital controls, lest capital flight becomes an increasingly tangible risk. Indeed, China’s capital account is tightly controlled, which is not something global investors are accustomed to, or want, when deploying capital overseas. Thus, for the foreseeable future, the yuan poses little threat to dollar primacy, particularly as China’s recovery takes a shape unlike those of the past. 1 The People’s Bank of China reduced the rate on seven-day repurchase operations from 2.0% to 1.9% and reduced the rates on its standing lending facility by 10 bps. We anticipate fiscal stimulus measures may follow the latest easing in monetary policy. 2 Based on homeownership percentage by country, home price-to-income ratios, and asset class valuations. These findings are referenced from “Peak China Housing,” National Bureau of Economic Research, August 2020. 3 A similar “red line” scenario unfolded with China’s crack down on its education and technology sectors, with the latter affecting household names, such as Alibaba, Ant, and Tencent. However, since then, it appears there’s been a recognition that the crackdown stifled some of the most innovative and valuable Chinese companies, and the authorities are increasingly cognizant of the effects of standing in their way. 4 Based on Chinese government data. 5 While there are policies to support the labor force, such as increasing the retirement age, such moves jeopardize a popular backlash, which the authorities are very keen on avoiding. 6 Although we do not see an improvement on U.S./China relations over the foreseeable future, we see a relatively low probability of a conflict over Taiwan. However, we anticipate that tensions regarding Taiwan will remain elevated. Read More From PGIM Fixed Income Source(s) of data (unless otherwise noted): PGIM Fixed Income, as of June 13 2023. For Professional Investors only. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. All investments involve risk, including the possible loss of capital. PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide. These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. PGIM Fixed Income as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Investors seeking information regarding their particular investment needs should contact their own financial professional. These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy. Any forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fee. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government agency or private guarantor, there is no assurance that the guarantor will meet its obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss. In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a Singapore investment manager registered with and licensed by the Monetary Authority of Singapore. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 (paragraph (a) to (i) of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 - Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3. © 2023 PFI and its related entities. 2023-4521

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in