The Monroe Doctrine at 200: Its New Implications for LatAm Assets

December 2nd, 2023 marked the 200th anniversary of President James Monroe’s State of the Union address in which he proclaimed the Western Hemisphere as America’s domain. What later became known as the Monroe Doctrine was meant to keep “pesky” European powers out of Latin America.

Fast forward 200 years: as the global order fractures and the competition between the U.S. and China intensifies, Latin America is once again taking on a Monrovian importance. The region is now home to advanced economies and governments that exercise self-determination as they trade and ally themselves with partners as they please. Hence, the courtship within Latin America is shifting the dynamics of investing in the region and creating a new set of market opportunities.1

As the power competition between the U.S. and China intensifies, several structural anchors are also giving way. As they do, Latin America is increasingly viewed as a region that can tip the balance of power. For the U.S., the rising stakes in Latin America mean that the writing is on the wall if the country fails to engage the region more. Indeed, Beijing is said to be pursuing military bases in Argentina and Cuba while also seeking stronger ties with Nicaragua.

Given the vast set of geopolitical complexities, we’re focusing on three reasons why the U.S. will likely pursue stronger ties with Latin America going forward.

First, the demand for critical raw materials to facilitate the green energy transition is rising along with the need to secure these critical supply lines. Chile, Peru, and Mexico produce approximately 40% of the world’s copper; Peru is the second largest producer of zinc (after China); Chile produces approximately 30% of all lithium currently mined; and Venezuela has the largest oil reserves in the world—reserves which are still needed to bridge the fossil fuels to renewables gap. As a result, the U.S. will likely go to great lengths to maintain access to these resources due to the country’s enormous needs and in order to prevent their monopolization by an adversary.

Second, the COVID pandemic taught leaders the benefits of "friendshoring" and the need to reduce trade dependency on adversaries.2 For example, President Biden announced "Americas Partnership for Economic Prosperity (APEP)" last year, setting the stage to help integrate the U.S. economy more closely with Latin America, promoting the manufacturing of critical goods, such as semiconductors in Mexico and other Latin American countries.

Third, the need to control migration and secure national borders takes on greater importance prior to the 2024 elections in the U.S., and the topic will remain an issue for the country’s successive administrations. Here, the Biden Administration’s softer "carrot approach" towards Nicolas Maduro’s regime in Venezuela highlights this imperative. Indeed, sanctions on Venezuela were lifted in exchange for free and fair elections, and Chevron was allowed to resume operations in the country last year.

Given the context from these three points, what might an implicit revival of the Monroe Doctrine mean for buyers of Latin American sovereign debt and other financial assets?

Concerns over economic policies, government stability, lack of a regional lender of last resort, and the consequent volatility in asset prices remain significant obstacles for investment in Latin American assets. Nor is China sitting idly by. In addition to the rumored military bases in Cuba and Argentina, Beijing recently doubled the size of the central bank swap line towards Argentina to 70 billion CNY.

Given that opposition however, renewed U.S. engagement can provide investors with confidence that the Federal government and multilateral organizations could provide support in the event of financial stress.

More specifically, the IMF’s activity in Latin America should support bond prices, which also occurred during the institution’s involvement during the pandemic when it expanded its Foreign Credit Lines with Colombia, Peru, and Chile. More broadly, the IMF, World Bank, and other multilateral entities may increasingly become instruments of political influence in the region, hence, extending the floor under financial asset prices. For example, politics may have contributed to the IMF’s recent $830 million Extended Fund Facility with Honduras as the IMF would normally require far more stringent policies from an administration.

Furthermore, the multilateral entities appear to be operating with more leeway recently amid an increasingly fraught geopolitical backdrop. Prior to the election of Javier Milei—a pro-U.S. libertarian—as Argentina’s president, the IMF’s program disbursement of $7.5 billion to the unorthodox Kirchnerists in power seemed lax in comparison to the more stringent prior demands made of Pakistan.

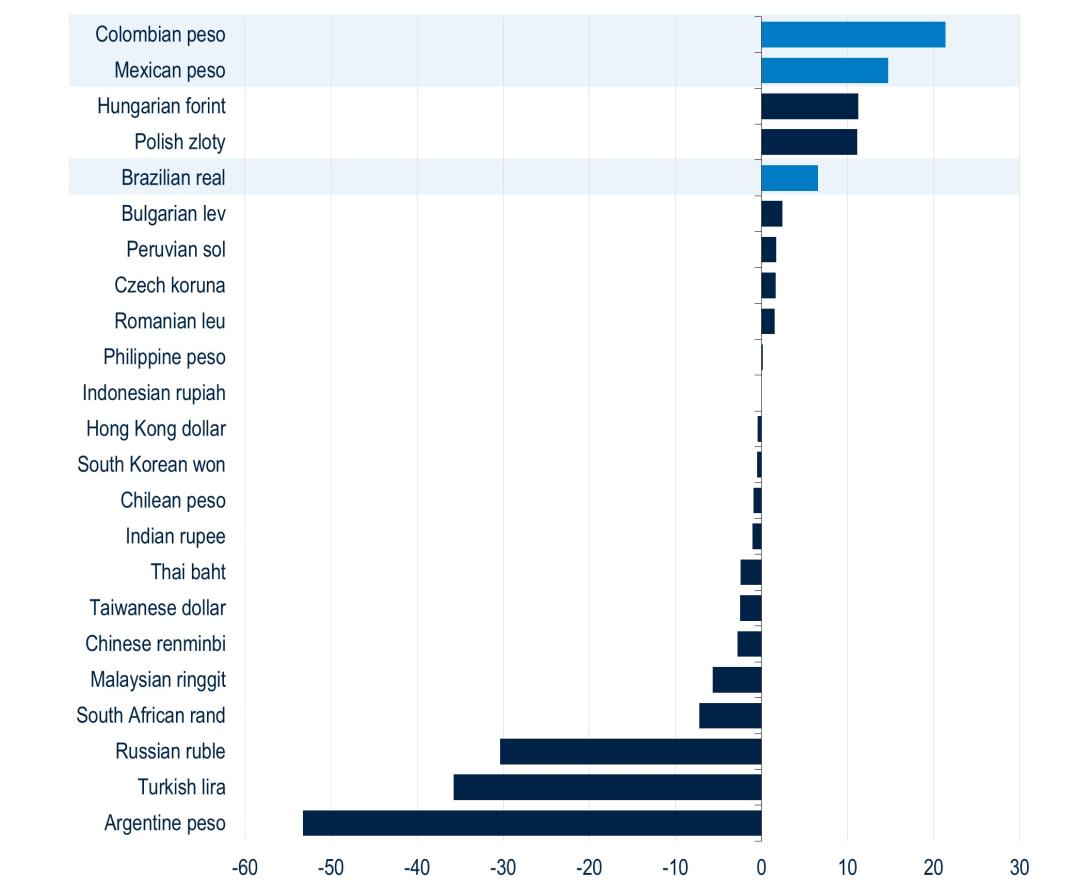

Markets have noted these trends as certain Latin American currencies have been some of the best performing currencies versus the U.S. dollar this year. With U.S. imports from Mexico surpassing those from China for the first time, the Mexican peso has been the star performer. In fact, three of the top five best performing currencies have been Latin American over the past 12 months (Figure 1). While central banks’ proactive inflation fight has been a major driver of this outperformance, trade and investment flows being diverted from Asia towards Latin America are also providing a boost.

FIGURE 1

LatAm currencies have fared well amid its position in the Great Power Competition between the U.S. and China.

Source: PGIM Fixed Income and Bloomberg

This performance occurred despite expectations for a rate hike-induced selloff, which are often associated with Latin American currency wobbles. Recall it was the Fed hikes in 1994 under Chair Greenspan that sent Mexico into the "Tequila Crisis." This time around, currencies are resilient, outperforming, and providing an additional boost to regional confidence.

Beyond currencies, markets perceive stabilizing and improving fundamentals in the region as Latin American sovereign spreads (EMBIG Diversified LatAm sub-index) tightened by approximately 43 bps over the last 12 months. This is not to say Latin America is now immune to defaults or blow ups. Despite Argentina’s promising reserves of lithium, oil, and gas as well as its large agricultural exports, the country still has a nasty debt overhang that the Milei administration will now have to manage.

However, recent political and market developments point to a stark new reality: Latin American countries willing to relationship-build with the U.S. could see the financial support flow without too much difficulty.

With a new Cold War looming, the rules of engagement with the region have changed, and the historical norms that would impede more alignment between Latin America and the U.S. are likely a thing of the past. Hence, the implications of a renewed Monroe Doctrine are significant. An asset repricing is under way, and investors should be ready if these markets behave very differently than past cycles in the quarters and years ahead.

Read More From PGIM Fixed Income

1 This post pertains to the potential evolution of the relationships between Latin American countries and the U.S. For a European perspective on Latin America, please see “Looking to Latin America to Fuel the EU’s Energy Transition,” PGIMFixedIncome.com, August 24, 2023.

2 The supply chain de-risking described in the second reason is another structural anchor that is giving way.

The comments, opinions, and estimates contained herein are based on and/or derived from publicly available information from sources that PGIM Fixed Income believes to be reliable. We do not guarantee the accuracy of such sources or information. This outlook, which is for informational purposes only, sets forth our views as of this date. The underlying assumptions and our views are subject to change. Past performance is not a guarantee or a reliable indicator of future results.

Source(s) of data (unless otherwise noted): PGIM Fixed Income, as of December 12, 2023.

For Professional Investors only. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. All investments involve risk, including the possible loss of capital.

PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.

These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. PGIM Fixed Income as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Investors seeking information regarding their particular investment needs should contact their own financial professional.

These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy.

Any forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fee. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government agency or private guarantor, there is no assurance that the guarantor will meet its obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss.

In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR.PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited including those available under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In Switzerland, information is issued by PGIM Limited, London, through its Representative Office in Zurich with registered office: Kappelergasse 14, CH-8001 Zurich, Switzerland. PGIM Limited, London, Representative Office in Zurich is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA and these materials are issued to persons who are professional or institutional clients within the meaning of Art.4 para 3 and 4 FinSA in Switzerland. In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a regulated entity with the Monetary Authority of Singapore under a Capital Markets Services License to conduct fund management and an exempt financial adviser. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 -Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3.

© 2023 PFI and its related entities.

2023-9053

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in