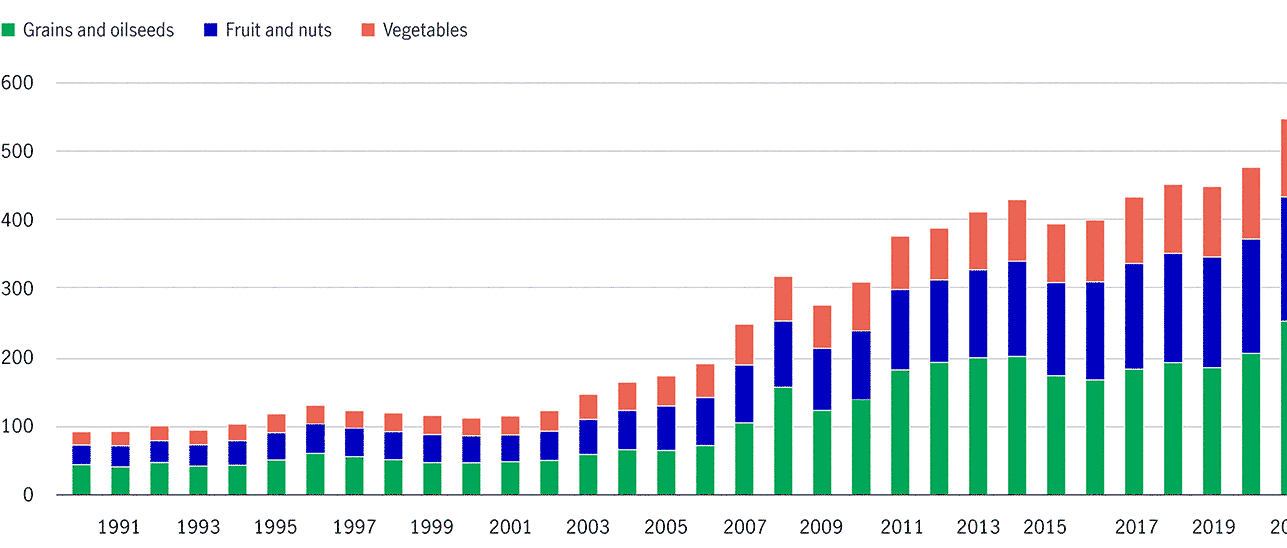

Source: ITC Trade Map, as of August 31, 2023. While there are challenges associated with trading in agriculture, there are also opportunities. The loss for the U.S. soybean sector was a gain for Brazil, which has replaced the United States as China’s leading soybean supplier, even after a truce was reached between the United States and China in 2020. And when China imposed tariffs on U.S. farm products, U.S. almonds were also affected, with increasing consumption of almonds in China relying on imports to meet its vast domestic demand. Australia, the largest almond production region in the southern hemisphere, increased its almond exports to China in 2018 and 2019, resulting in its negligible pre-2018 exports to China rising to an average of $250 million from 2019 to 2022. In this case, the challenges experienced by one region’s exports once again resulted in lasting opportunities for another market.

Source: ITC Trade Map, as of August 31, 2023. While there are challenges associated with trading in agriculture, there are also opportunities. The loss for the U.S. soybean sector was a gain for Brazil, which has replaced the United States as China’s leading soybean supplier, even after a truce was reached between the United States and China in 2020. And when China imposed tariffs on U.S. farm products, U.S. almonds were also affected, with increasing consumption of almonds in China relying on imports to meet its vast domestic demand. Australia, the largest almond production region in the southern hemisphere, increased its almond exports to China in 2018 and 2019, resulting in its negligible pre-2018 exports to China rising to an average of $250 million from 2019 to 2022. In this case, the challenges experienced by one region’s exports once again resulted in lasting opportunities for another market.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship and the full resources of our parent company to serve individuals, institutions, and retirement plan members worldwide. Headquartered in Toronto and Boston, our leading capabilities in public and private markets are strengthened by an investment footprint that spans 19 countries and territories. Our private markets strategies include private equity and credit, real estate, infrastructure, timber, and agriculture. Responsible stewardship is integral to our business and culture, and we seek to be a global leader in creating long-term, sustainable, value for our stakeholders.

Amy Theuninck

Managing Director, Insurance Solutions

atheuninck@manulife.com

857-328-6425

197 Clarendon St, Boston, MA 02116

United States