The role of EM debt in multi-sector credit strategies

An allocation to multi-sector credit does not automatically give investors the exposure to EM debt that they want or need.

Introduction

As the appeal of multi-sector credit strategies grows among asset allocators, some are questioning whether these negate the need for direct allocations to EM debt, for example. Here’s why a standalone allocation to EM debt still makes sense.

Multi-sector credit strategies gain momentum

Multi-sector credit strategies have rapidly increased in prominence over the last decade as investors reconsider the optimal expression of their strategic asset allocation relative to their investment objectives. This has reflected a growing trend for investors to substitute a portion of their traditional growth allocation (bonds and equities) with a credit-oriented strategy that offers yield, dynamic asset allocation and improved diversification. The reset in global yields over the past year has further increased appetite for such strategies.

In our experience, multi-sector credit allocations are typically made by investors who are either evolving their core investment-grade and high-yield corporate allocations (to access a broader spectrum of growth fixed income assets) or from those looking to de-risk or diversify their equity exposure.

Today, more than 100 strategies follow a multi-sector credit approach, investing more than US$240 billion in total.1 It is perhaps not surprising then that as the adoption of multi-sector credit strategies has grown, investors and their consultants have increasingly questioned whether direct allocations to the individual components within these remain necessary.

Why EM debt is worthy of a structural allocation

As an earlier piece in our Deliberating EM debt series outlined, over the past 20 years, EM debt has delivered attractive returns, especially relative to the asset class’s underlying credit quality. While over the past decade there have been periods when the market (particularly local currency debt) has struggled to contend with the relentlessly strong US dollar, the diversification and return arguments have remained intact. Notwithstanding these benefits, many investors have questioned whether they already get exposure to the return and growth dynamics of emerging markets via their existing allocations and specifically through a Global Aggregated allocation or via multi-sector credit. We explore the role EM debt may play in a Global Aggregated mandate in a separate paper; in this piece we discuss EM debt in the context of multi-sector credit.

Multi-sector credit strategies may provide sub-optimal exposure to EM debt

The majority of multi-sector credit funds (c.60% of the eVestment universe) are constructed in a benchmark-agnostic fashion. However there is still a significant portion (c.40%) aligned to more traditional benchmark indices. Interestingly, only a fifth of this cohort has a benchmark allocation to EM debt. Therefore, from a starting-point perspective, EM debt is a core opportunity for only a few multi-sector credit managers. Even among those managers that do allocate to EM debt, the average allocation is only 10%. As multi-sector credit is typically a subset of an investor’s overall fixed income allocation, it follows that total exposure to EM debt is typically extremely low among investors who rely entirely on their multi-sector credit allocation for their EM debt exposure.

This is an important consideration for those investors looking to align their strategic asset allocation with global macroeconomic and investment trends. Longer-term global economic momentum is shifting away from advanced western economies, with emerging markets constituting a larger share of economic activity.

From a more tactical perspective, a common characteristic of some multi-sector credit approaches is an inherent bias towards the manager’s home market. While many multi-sector credit approaches are designed to be dynamic, the average allocation to EM debt has been incredibly stable through time, with a minimum average allocation across managers of c.7.5% and a maximum of c.12.5%. This underscores how EM debt is often perceived as a peripheral allocation, and the stability of allocations suggests a reluctance to allocate dynamically. Investors should ask whether their multi-sector credit manager will really seize the opportunity when the structural and cyclical stars align on EM debt.

Another main consideration is that most EM debt allocations within multi-sector credit portfolios typically only focus on hard currency sovereign and corporate debt, thus totally ignoring the much larger and more liquid local currency EM debt opportunity. We believe that the inclusion of local currency debt, alongside hard currency debt, adds an entirely different dynamic and return driver to the portfolio which is far less correlated to core developed market rates. Perhaps one reason why multi-sector managers are reluctant to allocate to local currency EM debt is that this could dilute what is seen to be the primary return driver of these portfolios – credit spread. As a result, for these managers, the inclusion of local currency EM debt could be perceived as style drift. For those investors seeking a truly diversified allocation to EM debt, a standalone allocation may be the only sensible way of achieving this.

Additionally, within the more specialist and opportunistic component of most multi-sector credit approaches, the opportunity set within EM is the broadest – and arguably most compelling – when each of the EM debt sub-components (EM corporate credit, EM hard currency sovereign debt and EM local currency sovereign debt) is considered in its own right.

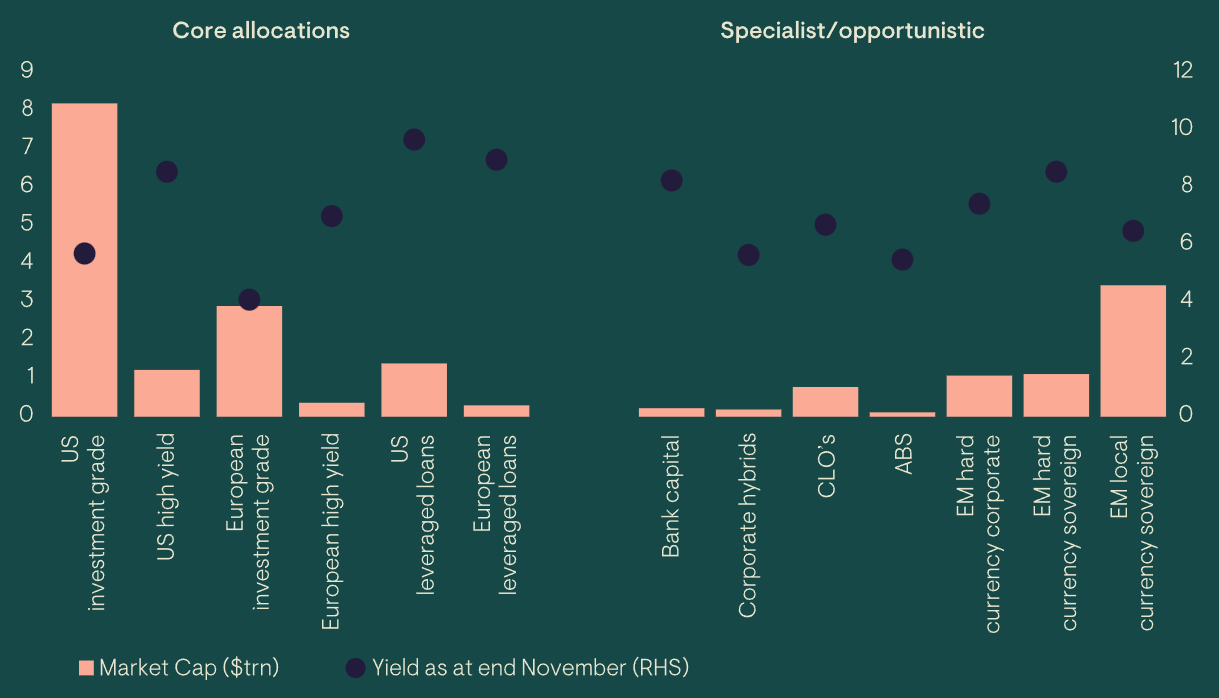

Figure 1: Credit market size and yields

Source: JP Morgan, BofA, as at 30 November 2023. US investment grade: ICE BofA US Investment Grade Index; US high yield: ICE BofA US High Yield Index; European investment grade: ICE BofA European Investment Grade Index; European high yield: ICE BofA European High Yield Index; US leveraged loans: JP Morgan Leveraged Loan Index; European leveraged loans: JP Morgan European Leveraged Loan Index; Bank capital: ICE BofA Contingent Capital Index; Corporate hybrids: ICE BofA Global Hybrids Index; CLO’s: JP Morgan CLOIE Index; ABS: Bloomberg US Agg ABS Index; EM hard currency corporate: JP Morgan CEMBI Broad Div; EM hard currency sovereign: JP Morgan EMBI Global Div; EM local currency sovereign: JP Morgan GBI-EM. For further information on indices, please see Important information section.

Given their higher levels of growth and investment, emerging markets should continue to offer attractive and diversified opportunities. This is especially the case as the world transitions to net-zero carbon emissions, which requires enormous investments into emerging markets to both mitigate the effects of climate change, and to develop the natural resources and technologies required for the transition. We believe that investors relying solely on a multi-sector strategy for EM exposure are likely to be underexposed to these long-term trends and significant commercial opportunities.

A highly diverse peer group

The multi-sector credit strategy peer group is a far from homogeneous, with significant variability in both targeted outcomes and investable universes. While most managers include the more traditional sub sectors of credit markets (e.g., global high yield, leveraged loans and global investment grade), the allocation to more specialist areas (e.g., structured credit, bank capital and corporate hybrids) is more variable. EM debt sits in the more specialist bucket, where allocations vary according to investment objectives, breadth of investment universe, and manager comfort/skill. This, alone, means careful consideration is warranted when considering whether your multi-sector credit allocation captures the necessary breadth of credit markets.

Conclusion

While some multi-sector credit strategies give investors exposure to EM debt, this exposure is typically low and focused purely on hard currency EM debt, thus ignoring the significantly larger, more liquid and uncorrelated local currency opportunity. Investors who rely solely on their multi-sector credit strategies for their EM debt exposure should scratch beneath the surface to understand if the allocation reflects the breadth of the EM opportunity set and the structural benefits. They should also consider whether the allocation is sized appropriately for their overall return, risk and diversification objectives.

1 As at 31 March 2023. Products assigned to the primary universe eVestment Multi-Asset Credit Fixed Income.

General risks. The value of investments, and any income generated from them, can fall as well as rise. Past performance does not predict future returns, losses may be made. Environmental, social or governance related risk events or factors, if they occur, could cause a negative impact on the value of investments.

Specific risks. Default: There is a risk that the issuers of fixed income investments (e.g. bonds) may not be able to meet interest payments nor repay the money they have borrowed. The worse the credit quality of the issuer, the greater the risk of default and therefore investment loss. Interest rate: The value of fixed income investments (e.g. bonds) tends to decrease when interest rates rise. Emerging market (inc. China): These markets carry a higher risk of financial loss than more developed markets as they may have less developed legal, political, economic or other systems.

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in