In the 10 years since the global financial crisis, low interest rates and declining credit spreads led many U.S. insurers to add more credit risk in their asset allocations in an effort to salvage yield. As a result, insurance portfolios are increasingly exposed to BBB rated securities – the lowest-quality investment grade credit segment.

Today, concerns are building around the deceleration of U.S. growth and potential recession that could drive an increase in credit downgrades, which in turn could have adverse economic, capital, accounting, and other disruptive impacts on insurance company portfolios. Should CIOs and investment teams be worried? We think fears of an avalanche of BBB downgrades are exaggerated, but we also see risks and fragilities that warrant action. Specifically, we believe insurance companies should look to differentiate, diversify, and maintain discipline.

Assessing portfolio allocations and risks

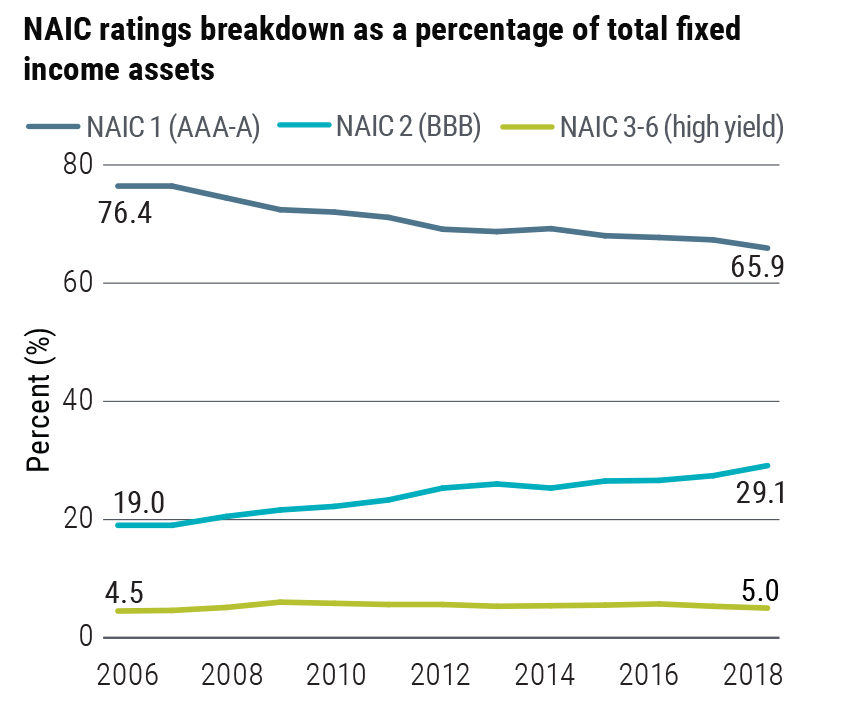

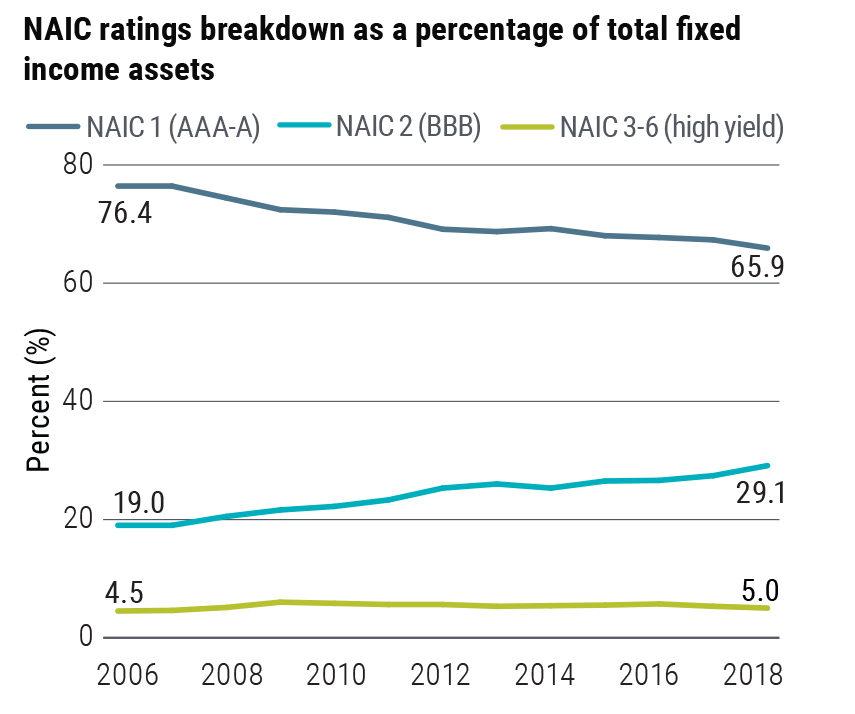

The post-crisis environment has not been friendly to insurers, especially those with interest-rate-sensitive liabilities. Portfolio yields in general have steadily declined as corporate bond yields have fallen. To counter this trend, many insurers have been reducing quality and lowering liquidity. As of December 2018, U.S. insurers held more than $1 trillion in public and private BBB-like exposure, including more than $700 billion in public BBB rated bonds, according to SNL Financial/S&P Global. The cumulative growth of all BBB assets (i.e., those categorized as NAIC 2 by the National Association of Insurance Commissioners) as a percentage of total fixed income holdings in U.S. insurance portfolios since 2006 has been roughly 10 percentage points (see Figure 1), increasing the average NAIC 2 allocation from 20% to just under 30% of total fixed income exposure.

Figure 1: U.S. insurance companies have increased fixed income allocations to BBB-equivalent securities by 10 percentage points since 2006

Source: SNL Financial/S&P Global, PIMCO as of December 2018

Insurers’ choice to maintain higher BBB allocations is supported by relatively stable liabilities, which allow for a longer-term investment orientation that can look through mark-to-market volatility. However, risk-based capital, accounting rules, and other factors create a disincentive to hold a large allocation to high yield bonds. This makes the growing proportion of BBB holdings across insurers more tenuous, as they are exposed to the risk that these bonds will be downgraded to high yield (“fallen angel” risk).

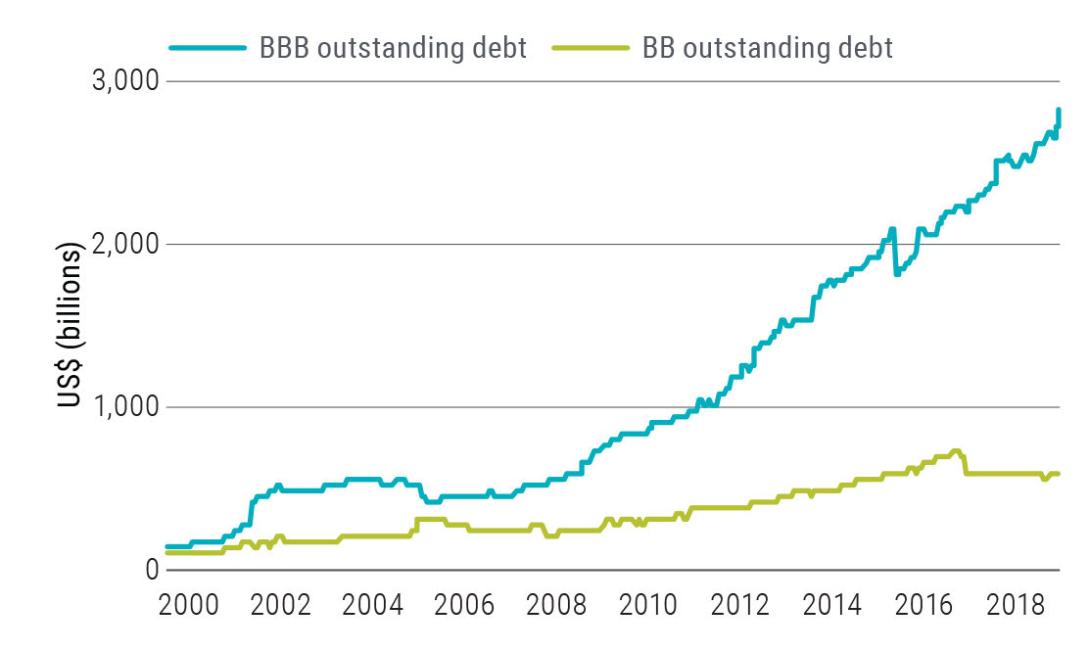

We’ve seen a general increase in net leverage across the U.S. investment grade (IG) corporate bond market as the share of BBBs increased from about 35% of the market in 2008 to about 50% today, according to Bloomberg Barclays corporate bond indices. U.S. BBB debt is also 4.7x larger in dollar terms and about five years longer in average maturity than the BB market one ratings bucket below (see Figure 2). Depending on the severity of the next downgrade cycle, the high yield (HY) market may have to absorb a much larger (and longer-maturity) supply of bonds – potentially exacerbating the likely weakness in prices.

Figure 2: After a decade of growth, U.S. BBB debt outstanding is nearly five times greater than BB debt

Source: J.P. Morgan as of December 2018

While some of the overall increase in credit market leverage and 20 risk is mitigated by higher equity valuations and lower interest rates (resulting in decent net debt/enterprise value ratios and interest coverage metrics), the margin for error has become lower as we advance further into the economic cycle and rating agencies become less lenient toward releveraging actions.

With that said, leverage ratios have plateaued among BBB issuers in the past couple of years, and where leverage has increased, it has often occurred in defensive sectors or as a result of mergers and acquisitions (M&A). Many of these companies can manage debt effectively via dividend reductions, asset sales, or realization of post-acquisition synergies. Rating migration trends help bear this out: In 2018, U.S. BBB upgrades to A/above outpaced BBB downgrades to high yield, while A/above downgrades to BBB outpaced the reverse by roughly three to one.

Also, rating migration risk within the BBB sector has been quite divergent historically; Moody’s ratings data from 1983 through 2016 show the risk of high yield downgrades over a one-year period for low BBB bonds is approximately six times the risk of downgrade for high BBBs.

Bottom line, risk has indeed risen in the IG credit market, but we don’t believe investors should indiscriminately reduce BBB exposure. The current environment argues for greater differentiation and a focus on bottom-up credit selection. We suggest insurance companies look to differentiate, diversify, and exhibit discipline.

Differentiate winners and losers

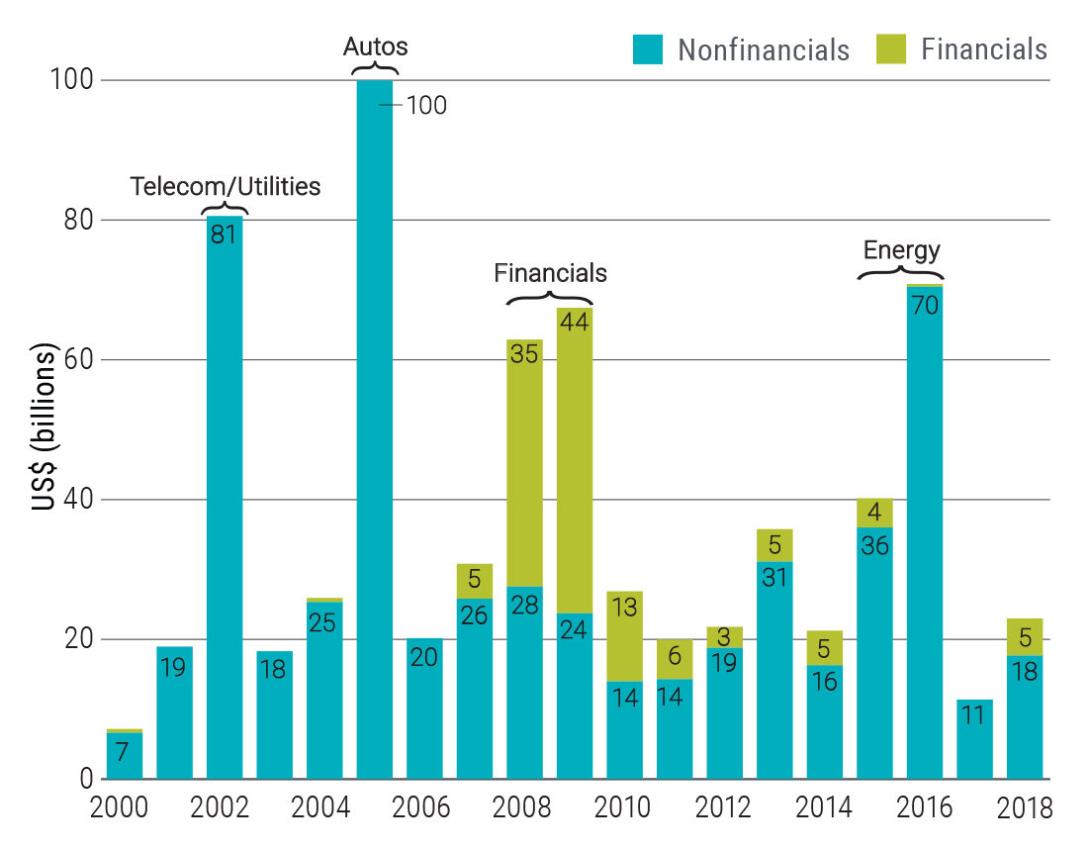

Predicting the timing of a business cycle downturn is difficult, but industry-specific cycles (and related credits likely to benefit or languish) are often easier to identify. Large clusters of HY downgrades since 2000 (both during and outside of recessions) have exhibited industry-specific themes (see Figure 3). This warrants increased sector differentiation and emphasis on managing concentration risk irrespective of business cycle risk.

Figure 3: Past HY downgrade episodes have exhibited pronounced industry themes

Source: J.P. Morgan as of year-end 2018

In an aging expansion, we tend to prefer industries and issuers with stable or deleveraging balance sheets, or those that have flexibility (and willingness) to sell assets or cut dividends amid fundamental weakness. We also favor credits with higher barriers to entry, pricing power, or asset-rich sectors.

In this context, we tend to favor select financials, real estate investment trusts (REITs), and midstream energy issuers. We are cautious on select utilities, chemicals, media, technology, auto, and retail names, many of which may struggle with M&A risk, cyclical vulnerability, or negative secular trends. That said, within all these industries, there exists a spectrum of stronger and weaker issuers. Thorough bottom-up analysis is crucial.

Another way we suggest investors differentiate among credits is maturity. The lack of term premium in the U.S. interest rate curve is one reason to favor shorter-maturity investments, all else equal, but we also see secular risks to traditional business models across many industries (autos, retail, upstream energy, and media) and supersecular climate risks that warrant additional caution and spread premium for longer-duration debt in lower-turnover portfolios.

Even in the absence of these yield curve and industry risks, shorter-maturity BBBs have historically exhibited higher returns per unit of risk (or Sharpe ratios) among broader tenor/ rating combinations across the corporate credit market. For example, over the past 20 years, BBB debt maturing in five years or less has exhibited Sharpe ratios ranging from 0.3 to 0.5, versus a range of 0.2 to 0.3 for single-A debt, per Bloomberg Barclays index data.

Diversify risk factors

Our view of diversification is not necessarily of different asset classes, but of risk factors. Insurance companies with elevated BBB (or credit risk) exposures may benefit from moving into higher-quality securities that provide more exposure to liquidity or complexity risks for comparable yield.

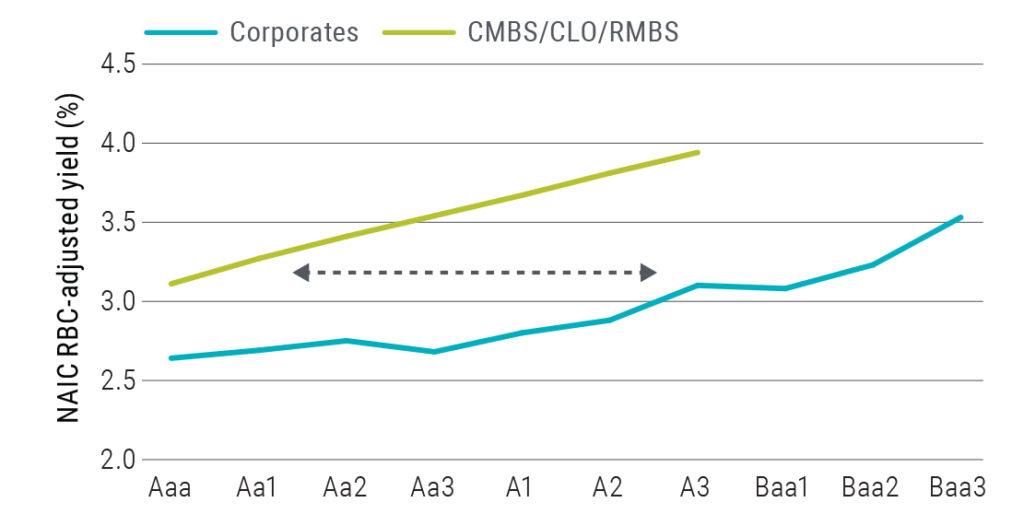

Spreads on BBB corporate credit (adjusted for leverage) are currently near the bottom of the range since 2000, according to Morgan Stanley. Current corporate bond allocations above 40% for the insurance industry as a whole (and 60% for life insurers) may benefit from increased diversification toward select high quality (NAIC 1) structured products such as commercial and residential mortgage-backed securities or loans, as well as collateralized loan obligations (see Figure 4).

Figure 4: Insurance companies can potentially move up in quality without sacrificing yield on a capital-adjusted basis

Source: Bloomberg Barclays, J.P. Morgan, PIMCO as of 31 May 2019. Note: Capital-adjusted yield calculations use current life after-tax RBC (risk-based capital) factors, a 400% RBC ratio, 10% weighted average cost of capital, and a 0.8 covariance adjustment. CMBS = commercial mortgage-backed securities, CLO = collateralized loan obligations, RMBS = residential mortgage-backed securities.

This approach not only diversifies the credit risk factor coming from corporates, but may benefit from favorable capital treatment under certain regimes, enabling replacement of capital-adjusted yields between AAA/AA structured products and A/BBB corporates.

Note, however, that the broad array of collateral types and structures cannot all be generalized as credit-loss-remote, even in the most senior tranches. While we believe insurers with heavier corporate credit exposure should consider greater diversification into structured product markets, there’s no substitute for having access to bottom-up expertise and a disciplined approach within this segment of the market. History may not repeat, but it may rhyme.

Maintain discipline (and dry powder)

Looking across IG index issues that were downgraded to high yield from 2017 to 2018, insurance companies sold close to 20% of their existing stock in these bonds over the six-month period before and after the downgrade event (based on transaction analysis from statutory insurance filings). Given the growth in BBB bonds and insurers’ large ownership of outstanding corporate debt, this forced selling dynamic could exacerbate spread widening and resulting losses. Price movement for fallen angels has historically supported patience; from 2000 to 2018, spreads (on average) recovered approximately 30% of pre-downgrade widening six months following the event (source: Bloomberg Barclays).

Since we believe it’s unrealistic for large investors in BBBs to expect complete avoidance of credit deterioration, a well- defined sell discipline or framework is critical. Key inputs should include setting a risk/capital budget to maintain fallen angels exposure and establishing criteria (based on fundamental, capital, or accounting targets) to guide decisions around potential sales and timing. A well-defined framework is critical to avoid knee-jerk decisions based on incomplete information or headlines.

Discipline applies not only to selling, but also to recognizing when valuations have overshot fundamentals, which may present attractive opportunities for insurers to provide liquidity to the market. Identifying overshoots is dependent on forward-looking fundamental research and valuation methodology. It’s likely we will see episodes of market volatility as political and growth risks persist – so having dry powder is key.

For insurers, dry powder goes beyond holding cash or cash equivalents, which can be expensive with respect to lost income. Firms should consider preparing contingent funding sources along with predefined investment policies and triggers to enable opportunistic purchases outside the current scope of allowable investments. Without these contingencies, glacial policy updates may mean missed market opportunities.

Key takeaways

The growth of U.S. BBB corporate debt creates understandable concern around a potential avalanche of high yield downgrades into a pronounced turn in the credit cycle – but we don’t believe this means investors should start running for the exit. There are both risks and opportunities across this structural component of insurance company portfolios – it’s a call to action to differentiate industries and issuers, diversify risk factors, maintain sell discipline, and create dry powder.

By PIMCO

Chitrang Purani, Portfolio Manager Financial Institutions

Jelle Brons, Portfolio Manager Global Corporate Bonds

Lillian Lin, Portfolio Manager Investment Grade Credit

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity.

High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not.

REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income.

Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations.

Collateralized Loan Obligations (CLOs) may involve a high degree of risk and are intended for sale to qualified investors only. Investors may lose some or all of the investment and there may be periods where no cash flow distributions are received. CLOs are exposed to risks such as credit, default, liquidity, management, volatility, interest rate and credit risk.

Diversification does not ensure against loss.

• There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

• The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/ issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

The Sharpe Ratio measures the risk-adjusted performance. The risk-free rate is subtracted from the rate of return for a portfolio and the result is divided by the standard deviation of the portfolio returns.

• This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2019, PIMCO. pimco.com blog.pimco.com

PC386_64416