- We believe a clearer view on the fed-funds rate should bring more property transactions back to the market and expect transaction volume to pick up toward the latter half of 2024.

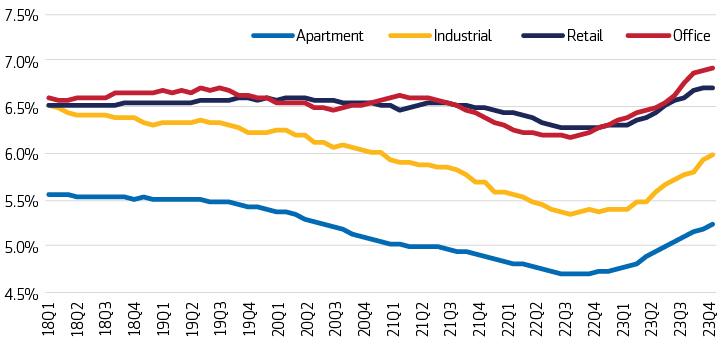

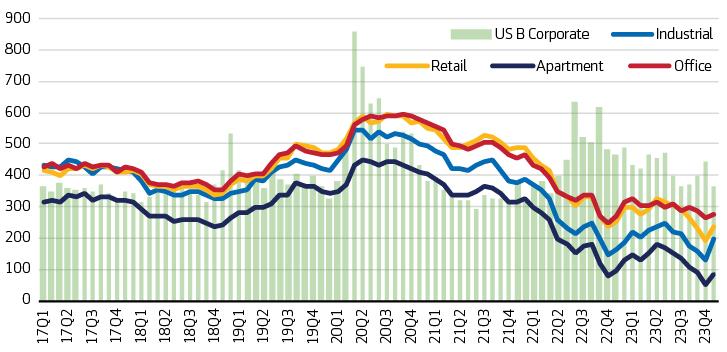

- Cap rates have risen across property types, but spreads have remained low compared to B-rated corporate bond spreads. We remain cautious on pricing and believe cap rates will likely expand further in 2024 before stabilizing during the second half of the year.

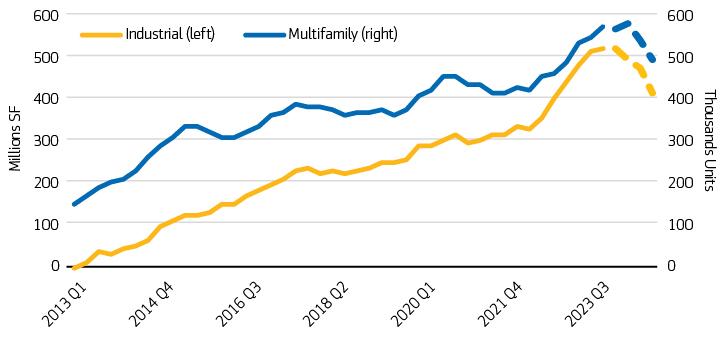

- The dominating force driving both apartment and industrial sector performance in 2024 is likely to remain on the supply side of the story, and how well supply can be digested for each market.

- The retail sector was the surprise darling in terms of performance compared to the other property sectors for 2023 and is likely to remain so for 2024. Office remains the most troublesome sector with the full effect of post-pandemic work arrangements still playing out.

Economic outlook

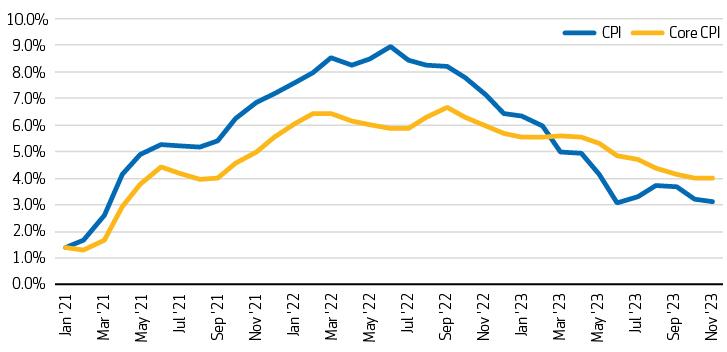

The past two years marked an unprecedented and aggressive tightening of monetary policy by the Federal Reserve (Fed). Since March 2022, the Fed has raised the fed-funds rate from effectively 0% eleven times to the range of 5.25% -5.50%. The need for such extraordinary measures was the result of the post-Covid surge in inflation which peaked at 8.9% in June 2022 as measured by the consumer price index (CPI).1 Despite the Fed’s efforts to curb inflation, it remained stubbornly high for the first half of 2023, but finally declined meaningfully in the fourth quarter. The annual inflation rate as reflected in headline and core CPI both declined markedly. Headline CPI declined to 3.1%, and core CPI declined to 4.0% in November compared to the previous year, the lowest since peaking in the third quarter of 2022.1

Inflation declined meaningfully in 4Q 2023

Statistics, Consumer Price Index as of November 30, 2023

The economy surprised the market to the upside in late 2023, and the expected recession has not materialized as of this writing. The job market remained near full employment, with the unemployment rate ending December at 3.7%.2 Consumer spending was robust, increasing in 10 out of the past 12 months ending in October. Furthermore, businesses and consumers seem to have grown more optimistic with the consumer confidence index registering a healthy 110.7 in December 2023, up from 101.0 in November.3

Though the likelihood of a “soft landing” has improved, Aegon AM’s base case is for sub-trend growth (in other words a growth recession) in 2024. The resumption of student loan payments, potential government shutdown, escalating geopolitical tensions, tighter credit conditions, and challenges in the banking sector are all likely to hinder economic growth heading into 2024. With that backdrop in mind, Aegon AM and forecasters are almost unanimous in thinking that the Fed has completed the tightening cycle it initiated in March 2022.4

US Commercial Real Estate

The sharp rise in interest rates brought the once red-hot capital market to a screeching halt in 2023. Transaction volume ending in November was down 58% compared to the same period in 2022, and was down 47% compared to pre-Covid levels.5 We believe a clearer view on the fed-funds rate should bring more transactions back to the market. However, CRE deals usually take months to close and the path toward closing the transaction gap will take time. We expect transaction volume to pick up in the latter half of 2024.

Cap rates have risen across property types, but spreads have remained low compared to B-rated corporate bond spreads. The ending of the tightening in the fed-funds rate was very well received by the market with the 10-year Treasury dropping from a decade high of 5% to a high 3% range.6 As of year-end 2023, the cap rate spread against B-rated corporate bonds tightened to the narrowest level since the beginning of the Fed’s rate-hike cycle.5,7 However, typically CRE performance responds to rate changes with a lag. We remain cautious on pricing and believe cap rates will likely expand further in 2024 before stabilizing during the second half of the year.

Cap rates have risen across major property sectors

Source: MSCI Real Capital Analytics. December 19, 2023

Cap rate spread* at the narrowest level since beginning of rate hikes

Source: MSCI Real Capital Analytics, Barclay’s Live as of November 30, 2023

*As measured against B-rated corporate spread

Emerging trends in property sectors

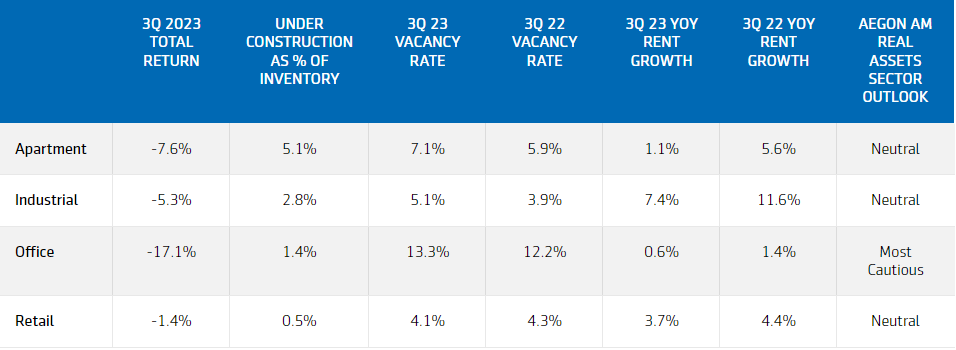

Turning to property sectors, the dominating force driving both apartment and industrial sector performance in 2024 is likely to remain on the supply side of the story, and how well supply can be digested for each market. Strong demand and the low cost of debt drove up construction during past couple years. We believe that both the apartment and industrial sectors are currently close to, if not at the peak of the supply cycle. The development pipeline contracted over the last two quarters of 2023; however, we believe deliveries will remain at an elevated level through 2024 and into 2025 given the current level of projects under construction. The speed at which this supply will get absorbed will vary by location. Nationally, our outlook for both sectors is neutral. We expect the occupancy rate to decline further for both sectors with rent growth remaining muted for apartments and slowing further for industrial properties to pre-Covid levels.

Supply for apartment and industrial sectors are at the peak of the cycle

Source: CoStar Realty Information, 3Q 2023.

The retail sector was the surprise darling in terms of performance compared to the other property sectors for 2023 and is likely to remain so for 2024. Supply side pressure is minimal as developers have been shying away from this sector for the past decade. Meanwhile, the demand side has continued to be robust with many retailers having trouble finding quality spaces to expand. As a result, the retail vacancy rate is at its tightest level ever recorded. In the long-term, we remain cognizant of the structural challenges facing the retail sector as e-commerce is expected to drive retail sales for the foreseeable future. However, our outlook for retail has changed from cautious to neutral. We believe the retail sector’s relatively strong performance should persist even as consumer spending and the broader economy slows.

Finally, the office sector is the most troublesome sector, and we have likely not seen the full effect of post-pandemic work arrangements play out. Employers are actively encouraging employees to return to the office by utilizing properties that are newer vintage, in prime locations, and offer modern amenities. We believe bifurcations between quality will widen further in 2024. Moreover, anecdotal evidence suggests that most office leases have not yet come up for renewal since the pandemic. Our outlook on the sector is most cautious, as when those leases expire, tenants are likely to downsize their floorplan or negotiate for lower rates.

Property sector outlook

Sources: National Council of Real Estate Investment Fiduciaries, CoStar Realty Information Inc., and Aegon Real Assets US. As of September 30, 2023.

Download

1 US Bureau of Labor Statistics. Consumer Price Index. November 30, 2023

2 US Bureau of Labor Statistics. Employment Situation. January 5, 2023

3 The Conference Board. US Consumer Confidence. December 20, 2023

4 Wolters Kluwer. Blue Chip Economic Indicators. December 8, 2023

5 MSCI Real Capital Analytics. December 19, 2023

6 Board of Governors of the Federal Reserve System. January 4, 2024

7 Barclay’s Live. B-Rated Corporate Spread. November 30, 2023

8 CoStar Realty Information, Inc. January 5, 2024

Disclosures

Unless otherwise noted, the information in this document has been derived from sources believed to be accurate at the time of publication.

This material is provided by Aegon Asset Management (Aegon AM) as general information and is intended exclusively for institutional, qualified, and wholesale investors, as well as professional clients (as defined by local laws and regulation) and other Aegon AM stakeholders.

This document is for informational purposes only in connection with the marketing and advertising of products and services, and is not investment research, advice or a recommendation. It shall not constitute an offer to sell or the solicitation to buy any investment nor shall any offer of products or services be made to any person in any jurisdiction where unlawful or unauthorized. Any opinions, estimates, or forecasts expressed are the current views of the author(s) at the time of publication and are subject to change without notice. The research taken into account in this document may or may not have been used for or be consistent with all Aegon AM investment strategies. References to securities, asset classes and financial markets are included for illustrative purposes only and should not be relied upon to assist or inform the making of any investment decisions. It has not been prepared in accordance with any legal requirements designed to promote the independence of investment research, and may have been acted upon by Aegon AM and Aegon AM staff for their own purposes.

The information contained in this material does not take into account any investor's investment objectives, particular needs, or financial situation. It should not be considered a comprehensive statement on any matter and should not be relied upon as such. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to any particular investor. Reliance upon information in this material is at the sole discretion of the recipient. Investors should consult their investment professional prior to making an investment decision. Aegon AM is under no obligation, expressed or implied, to update the information contained herein. Neither Aegon AM nor any of its affiliated entities are undertaking to provide impartial investment advice or give advice in a fiduciary capacity for purposes of any applicable US federal or state law or regulation. By receiving this communication, you agree with the intended purpose described above.

Past performance is not a guide to future performance. All investments contain risk and may lose value. This document contains "forward-looking statements" which are based on Aegon AM's beliefs, as well as on a number of assumptions concerning future events, based on information currently available. These statements involve certain risks, uncertainties and assumptions which are difficult to predict. Consequently, such statements cannot be guarantees of future performance, and actual outcomes and returns may differ materially from statements set forth herein.

The following Aegon affiliates are collectively referred to herein as Aegon Asset Management: Aegon USA Investment Management, LLC (Aegon AM US), Aegon USA Realty Advisors, LLC (Aegon RA), Aegon Asset Management UK plc (Aegon AM UK), and Aegon Investment Management B.V. (Aegon AM NL). Each of these Aegon Asset Management entities is a wholly owned subsidiary of Aegon Ltd. In addition, Aegon Private Fund Management (Shanghai) Co, Ltd., a partially owned affiliate, may also conduct certain business activities under the Aegon Asset Management brand.

Aegon AM UK is authorised and regulated by the Financial Conduct Authority (FRN: 144267) and is additionally a registered investment adviser with the United States (US) Securities and Exchange Commission (SEC). Aegon AM US and Aegon RA are both US SEC registered investment advisers.

Aegon AM NL is registered with the Netherlands Authority for the Financial Markets as a licensed fund management company and on the basis of its fund management license is also authorized to provide individual portfolio management and advisory services in certain jurisdictions. Aegon AM NL has also entered into a participating affiliate arrangement with Aegon AM US. Aegon Private Fund Management (Shanghai) Co., Ltd is regulated by the China Securities Regulatory Commission (CSRC) and the Asset Management Association of China (AMAC) for Qualified Investors only.

©2024 Aegon Asset Management. All rights reserved.

AdTrax: 6188778.1GBL