- The optimism seen earlier this year on interest rates has not translated into a rebound in transaction volume. We believe buyers and sellers need to come to a better agreement on pricing before we see meaningful improvement.

- The sharp rise in interest rates since early 2022 is raising the risk of refinancing for maturing commercial real estate loans. Given where we are in the current cycle, Aegon Asset Management expects that distress will certainly rise as more loans mature and face difficulty refinancing. However, the magnitude of distress may not be as severe as the market fears.

- The office sector continues to find minimal demand for space, with vacancies rising another 20 basis points to a new record high of 13.7%.1 Newer vintage offices continue to see positive absorptions, and we believe bifurcations in performance will widen further as leases renew.

Property sector outlook

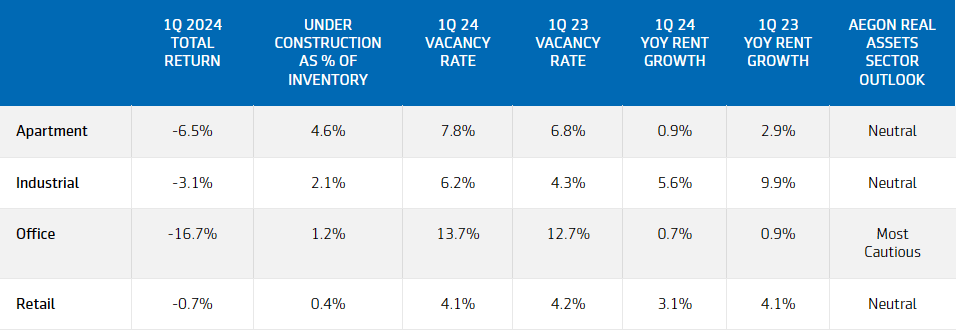

Sources: National Council of Real Estate Investment Fiduciaries, CoStar Realty Information Inc., and Aegon Real Assets US. As of March 31, 2024.

Apartment

Apartment sector fundamentals are likely to improve as supply and demand come to a better balance in 2024. During the first quarter of 2024, apartment supply continued to outpace demand. However, demand continued to grow, registering the highest level since late 2021. By the end of 2024, current supply projections show an almost 32% pullback from the record high posted in 2023. With apartment demand on the rise, this could be an opportunity for the sector to stabilize and recover in the latter half of this year.1

Industrial

The industrial sector is still digesting the massive wave of unleased properties delivered over the past year, with the current vacancy rate rising by 50 bps over the past quarter. Despite near-term supply pressure, the vacancy rate remains near the historical norm. In addition, new supply for industrial properties has plummeted since last fall. The current construction pipeline suggests new deliveries are expected to reach a 10-year low in mid-2025.1

Office

The office sector continues to find minimal demand for space, with vacancies rising another 20 bps to a new record high of 13.7%. Newer vintage offices continue to see positive absorptions, and we believe bifurcations in performance will widen further as leases renew.1

Retail

The first quarter of 2024 saw a slight softening of the retail sector, but it remained close to the tightest level ever. With minimal supply-side pressure, demand remained robust, and many retailers struggled to find quality spaces for expansion.1

1 CoStar Realty Information, Inc. March 31, 2024.

Download PDF

Important disclosures

This material is provided by Aegon Asset Management (Aegon AM) as general information and is intended exclusively for institutional and wholesale investors, as well as professional clients (as defined by local laws and regulation) and other Aegon AM stakeholders.

This document is for informational purposes only in connection with the marketing and advertising of products and services, and is not investment research, advice or a recommendation. It shall not constitute an offer to sell or the solicitation to buy any investment nor shall any offer of products or services be made to any person in any jurisdiction where unlawful or unauthorized. Any opinions, estimates, or forecasts expressed are the current views of the author(s) at the time of publication and are subject to change without notice. The research taken into account in this document may or may not have been used for or be consistent with all Aegon Asset Management investment strategies. References to securities, asset classes and financial markets are included for illustrative purposes only and should not be relied upon to assist or inform the making of any investment decisions. It has not been prepared in accordance with any legal requirements designed to promote the independence of investment research, and may have been acted upon by Aegon AM and Aegon AM staff for their own purposes.

The information contained in this material does not take into account any investor's investment objectives, particular needs, or financial situation. It should not be considered a comprehensive statement on any matter and should not be relied upon as such. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to any particular investor. Reliance upon information in this material is at the sole discretion of the recipient. Investors should consult their investment professional prior to making an investment decision. Aegon AM is under no obligation, expressed or implied, to update the information contained herein. Neither Aegon Asset Management nor any of its affiliated entities are undertaking to provide impartial investment advice or give advice in a fiduciary capacity for purposes of any applicable US federal or state law or regulation. By receiving this communication, you agree with the intended purpose described above.

Past performance is not a guide to future performance. All investments contain risk and may lose value. This document contains "forward-looking statements" which are based on Aegon AM's beliefs, as well as on a number of assumptions concerning future events, based on information currently available. These statements involve certain risks, uncertainties and assumptions which are difficult to predict. Consequently, such statements cannot be guarantees of future performance, and actual outcomes and returns may differ materially from statements set forth herein.

©2024 Aegon Asset Management. All rights reserved.

AdTrax: 6418879.3