- The US Federal Market Operating Committee (FOMC) agreed to hold interest rates steady for the fourth consecutive time at its meeting in January, leaving its benchmark interest rate at a target range of 5.25% to 5.50%.1

- The 10-year US Treasury notched a sixteen-year high in October and has since eased to just over 4% as of late February. The decline in long-term rates stem from the expectation that the US Federal Reserve (Fed) will not be raising interest rates as many times in 2024 as investors initially thought. The Fed still expects rate cuts to occur in the second half of 2024, but they seem to be delaying any premature cuts until they see signs that inflation has permanently cooled.1

- Inflation, as measured by the core personal consumption expenditure (PCE) index, declined meaningfully to 2.9% in December but remained higher than the Fed’s 2% goal. As a result, most economists surveyed by the Blue-Chip Economic Indicators are now expecting rate-cuts to occur later into 2024, as well as fewer cuts to happen within the year overall.2,3

- Within commercial real estate debt, commercial mortgage loan spreads are adjusting, albeit at a slower pace, and at the time of this writing were in the 150 to 215 bps range. Life companies have remained disciplined in their lending standards with most having similar allocations in 2024 compared to 2023.

- Property transaction volume was down 41% during 4Q 2023 compared to a year earlier. Transaction volume was down 51% in 2023 compared to 2022.4

- Property values were essentially flat for the past three quarters of 2023. However, property prices still declined by 5.9% in December compared to the previous year.4

- NCREIF National Property Index (NPI) returned -7.9% in 4Q 2023 compared to a year earlier. Capital appreciation was reported as -11.8%, with income return at 4.3%.5

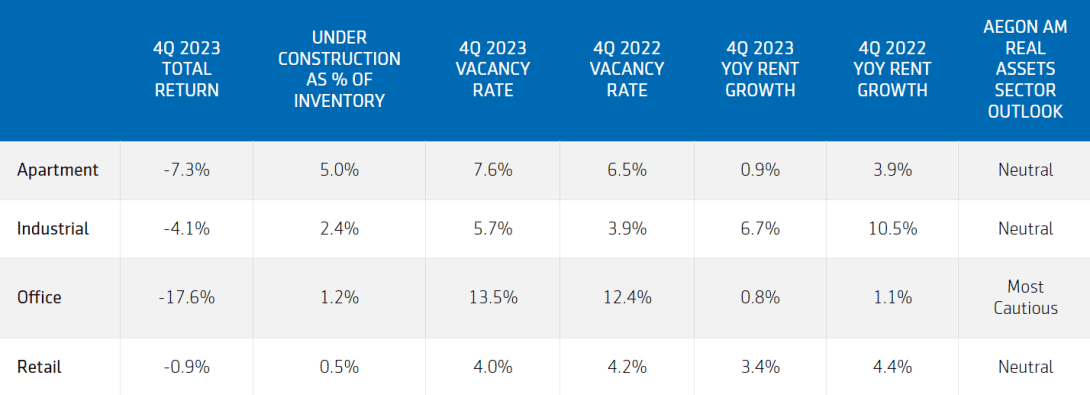

Property sector outlook

Sources: National Council of Real Estate Investment Fiduciaries, CoStar Realty Information Inc., and Aegon Real Assets US. As of December 31, 2023.

Apartment

The apartment sector continues to face cyclical supply headwinds with demand fundamentals remaining healthy. While supply headwinds are affecting the majority of the top 50 markets, the magnitude of new supply and performance across these markets differs significantly. Given strong demand supported by low homeownership affordability and the necessity of housing, we believe apartment sector performance will likely stabilize towards the end of 2024.

Industrial

The industrial sector remained relatively tight in 4Q 2023 but performance softened heading into 2024 as a near-record amount of new supply hit the market and demand continued to moderate. Elevated supply levels are projected to be above trend and likely to push vacancy rate upwards over the next several quarters. However, recent pullback in starts signaled supply side pressure is expected to recede by early 2025.6 Longer-term growth prospects continue to be supported by supply chain reshoring, near-shoring, and e-commerce driven consumption.

Office

The office sector continues to face structural challenges with the hybrid work model not showing any signs of ending in most metros. Roughly a quarter of existing office leases are expected to expire in 2024 and 2025, with more than 80% of these leases being executed before the pandemic.7 We believe office tenants are likely to negotiate for lower rates or downsize to smaller square footage if the overall sentiment on office use does not improve.

Retail

The retail sector continues to demonstrate resilience as its vacancy rate declined to the lowest recorded level in 4Q 2023. Rent growth remained solid as the demand for retail space remains high supported by a strong and resilient labor market that continues to drive up consumer spending as wage growth outpaces inflation. Real estate fundamentals in the retail sector are expected to remain strong in 2024 due to very little new construction deliveries over the past decade, and availability rates are expected to continue to be tight through 2024.6

1 Board of Governors of the Federal Reserve System. January 31, 2024

2 Wolters Kluwer. Blue Chip Economic Indicators. February 9, 2024

3 US Bureau of Economic Analysis. Personal Income and Outlays. January 26, 2024

4 MSCI Real Capital Analytics. January 23, 2024

5 National Council of Real Estate Investment Fiduciaries. December 31, 2023

6 CoStar Realty Information, Inc. January 31, 2024

7 Compstak. October 4, 2023

Download PDF

This material is provided by Aegon Asset Management (Aegon AM) as general information and is intended exclusively for institutional and wholesale investors, as well as professional clients (as defined by local laws and regulation) and other Aegon AM stakeholders.

This document is for informational purposes only in connection with the marketing and advertising of products and services, and is not investment research, advice or a recommendation. It shall not constitute an offer to sell or the solicitation to buy any investment nor shall any offer of products or services be made to any person in any jurisdiction where unlawful or unauthorized. Any opinions, estimates, or forecasts expressed are the current views of the author(s) at the time of publication and are subject to change without notice. The research taken into account in this document may or may not have been used for or be consistent with all Aegon Asset Management investment strategies. References to securities, asset classes and financial markets are included for illustrative purposes only and should not be relied upon to assist or inform the making of any investment decisions. It has not been prepared in accordance with any legal requirements designed to promote the independence of investment research, and may have been acted upon by Aegon AM and Aegon AM staff for their own purposes.

The information contained in this material does not take into account any investor's investment objectives, particular needs, or financial situation. It should not be considered a comprehensive statement on any matter and should not be relied upon as such. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to any particular investor. Reliance upon information in this material is at the sole discretion of the recipient. Investors should consult their investment professional prior to making an investment decision. Aegon AM is under no obligation, expressed or implied, to update the information contained herein. Neither Aegon Asset Management nor any of its affiliated entities are undertaking to provide impartial investment advice or give advice in a fiduciary capacity for purposes of any applicable US federal or state law or regulation. By receiving this communication, you agree with the intended purpose described above.

Past performance is not a guide to future performance. All investments contain risk and may lose value. This document contains "forward-looking statements" which are based on Aegon AM's beliefs, as well as on a number of assumptions concerning future events, based on information currently available. These statements involve certain risks, uncertainties and assumptions which are difficult to predict. Consequently, such statements cannot be guarantees of future performance, and actual outcomes and returns may differ materially from statements set forth herein.

©2024 Aegon Asset Management. All rights reserved.

AdTrax: 6418879.1GBL