Weighing passive and active approaches to EM debt investing

Introduction

EM debt remains an asset class in which asset allocators favour an active management approach, but the passive versus active debate continues. As active managers, it will come as little surprise which side of the fence we sit on. Here we outline the key considerations – relating to returns, fees and sustainability – behind our view that passive approaches are sub-optimal for EM debt investors.

Passive approaches extend their reach

Investors face increasing choice across the investment spectrum, with the active versus passive debate extending its reach. In certain asset classes, such as large-cap US equities, passive investing has been the dominant expression of risk, accounting for an estimated 61% of assets under management – up from around a third 10 years ago. In emerging market (EM) debt, however, just one-fifth of assets are managed passively, and the debate continues.1

Proponents of passive approaches typically claim that active managers do not deliver consistent alpha and that passive fees are significantly lower than active. This boils down to the question: can active managers in EM debt add sufficient value to justify the higher fees they charge? We examine the alpha – realised and potential – derived from active management in the asset class and look at the cost-saving potential of passive approaches.

Returns comparison

The theory: EM debt offers significant alpha potential for active managers

The EM debt universe is hugely diverse, encompassing over 70 differing countries, as we noted here, with associated investment strategies incorporating hard currency, local currency, and corporate product offerings, as well as many combinations thereof.

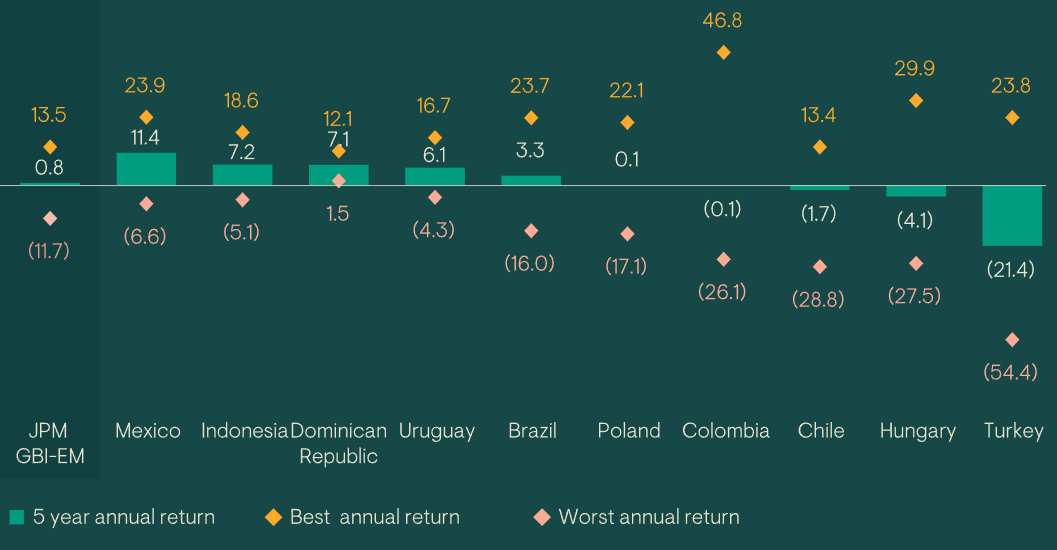

With high cross-sectional regional dispersion, the universe provides active managers with an ever-growing opportunity set to explore in pursuit of alpha. Figure 1 illustrates this dispersion using a sample2 of EM countries within the JP Morgan GBI-EM index - the most widely followed EM benchmark for local currency sovereign strategies.

Figure 1: Dispersion of annualised returns over past five years - local currency debt markets (%)

Source: JP Morgan, Bloomberg, 30 November 2023. Five-year annualised return. For illustrative purposes only. Five years used to encompass an economic cycle. For important information on indices, please see Important information section.

The dispersion in returns is stark. Colombia, for example, has seen annual returns over the last five years range from -26.1% to +46.8%. Turkey’s best annual return in the period was +23.8%; its worst was -54.4%. Looking through a hard currency lens would reveal similar divergences. This reflects not just significant diversity of underlying fundamentals and drivers in these markets; this is an under-researched investment universe, rife with inefficiencies in market pricing and information asymmetry. These factors provide active managers with greater opportunity to generate alpha through market selection than in other, more widely researched markets.

Active selection and relative-value positioning across the investment universe is just one source of potential alpha that passive funds miss out on. Another example is the new-issue premium available in primary issuance, which only active managers can participate in. Our analysis across bonds in the JP Morgan Emerging Market Bond Index3 or ‘EMBI’ - (the main EM hard currency sovereign index) showed a reasonably consistent new-issue premium across high-yield and investment-grade markets in primary issuance relative to other bonds from the same sovereign and index – typically fluctuating between 0.5% and 1.5%, depending on market conditions. Another example is the ability of active managers to take exposure in countries pre-index inclusion. For instance, India’s local currency sovereign bonds will begin a phased inclusion into the JP Morgan GBI-EM Global Diversified index in 2024, to eventually account for 10% of the index; an active manager can pre-empt the sizeable inflows expected from changes to index composition (the ‘passive bid’) and buy ahead of the official inclusion date. These potential alpha sources are amplified in EM, given the evolving nature of the universe.

In practice: active and passive strategy performance

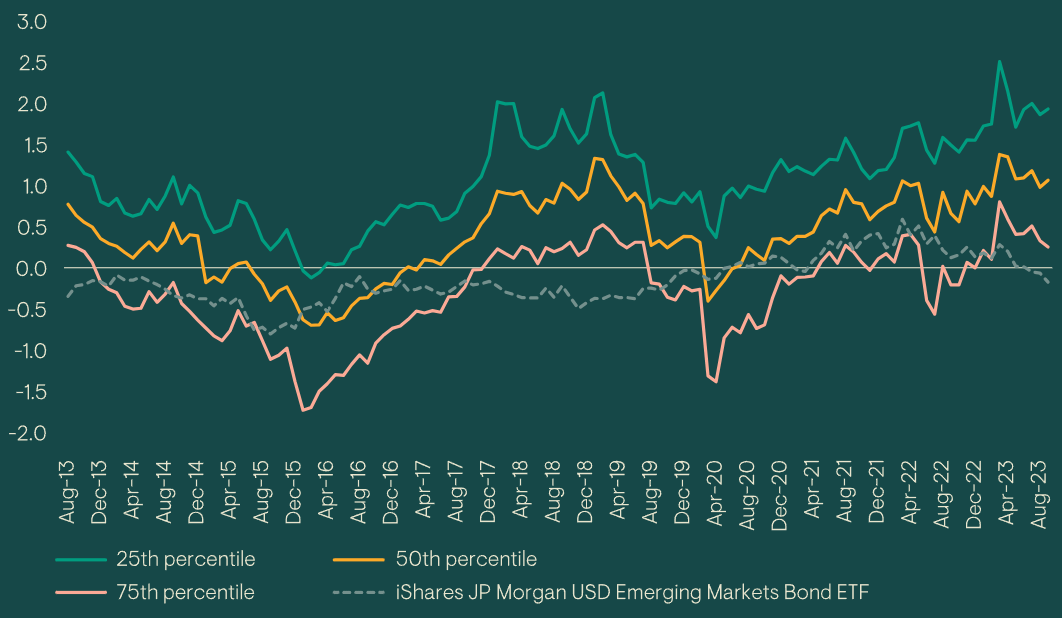

We looked at the eVestment universe, which surveys 144 managers with combined assets under management of US$384 billion (as at the end of Q2 2023). When considering three-year rolling returns in the hard currency EM sovereign universe over the last 10 years4, it is clear that a large proportion of active managers outperformed the passive products that most investors can access, with top-quartile active managers outperforming the index by up to 249 basis points (bps) over the period, gross of fees. Outperformance by at least the median active manager is a clear and consistent trend since January 2017. Similar observations hold for rolling five-year returns, as well as for EM local currency funds, as shown in the Appendix.

Figure 2: Rolling three-year excess returns – EM hard currency debt managers (gross of fees, %)

Past performance does not predict future returns; losses may be made.

Source: eVestment EM HC fixed income universe, from 31 August 2013 to 30 September 2023. Performance is gross of fees (returns will be reduced by management fees and other expenses incurred), income is reinvested, in US dollars.

Winners and losers

While the above points to a broadly favourable comparison between active and passive, it is important to note the significant disparity of performance among active managers. For example, in the three years to June 2022, the top quartile of active managers outperformed passive by 114bps, while the bottom quartile underperformed by 68bps. The upshot is that asset allocators choosing to invest actively in the asset class need to carry out careful due diligence on managers. A similar conclusion can be drawn when looking at the performance of active versus passive in local currency strategies.5 This is a complex investment universe to navigate and requires a specialist skill set.

When active works best

Even for active managers with the relevant skills, tools and expertise, not all environments are conducive for alpha generation. When macro drivers dominate market moves, pushing dispersion down and correlations up, fundamentals focused active investment approaches can struggle to generate alpha. At such times, the relative appeal of passive approaches rises, and the active/passive debate reignites, as it has done in recent months. Yet we believe the environment is shifting; as the end of the US rate hiking cycle appears on the horizon and the dominance of US monetary policy decisions in the context of investment flows starts to fade, we believe EM fundamentals are returning to the fore.

Cost considerations

Passive is (somewhat) cheaper, but does that mean value for money?

A frequently touted advantage of passive investment vehicles is their lower fees when compared to actively managed strategies. While this holds for some asset classes – fees can be as low as 15bps for some US equity ETFs – in EM debt, the picture is less stark. According to our analysis of Morningstar’s passive hard currency EM debt ETF peer group, the average expense ratio is 39bps, compared with 101bps for active funds, as shown in Figure 3 below. Furthermore, while passive funds are still broadly cheaper, we question how the cost advantage stacks up relative to the historical and potential returns of active management. Figure 3 also reveals a clear trend in outperformance by the active strategies when comparing returns over various periods, and leads us to conclude that the cost advantage of passive approaches does not offset the value added through active management. Similar observations hold for EM local currency funds, as shown in the Appendix.

Figure 3: Fee and performance comparison of EM hard currency debt strategies (%)

Past performance does not predict future returns; losses may be made.

Source: Morningstar Direct, October 2023. Net expenses and performance are based on simple averages of US dollar-denominated EM Debt ETFs and Active Manager products. These are defined as the US Emerging Market Bond Category (inc. ETFs) where the underlying benchmark is JP Morgan EMBI or equivalent Hard Currency index. Sample size 179 managers.

Factors constraining passive approaches

The fact that fees on passive EM debt strategies are relatively high is perhaps unsurprising. EM debt is a complex and relatively costly asset class to invest in, regardless of the investment approach, making it more challenging than in other asset classes to offer low-cost products in this space. Emerging markets are typically less liquid and more volatile than developed markets – factors that can also lead to a higher tracking error for passive EM strategies. This is evident in the divergent performance of EM ETFs, which can deviate meaningfully from the benchmark – with annualised tracking errors ranging from 0.74% to 1.04% in the hard currency market, and even more in the local currency markets (up to 3.54%).6

Relative to other asset classes, the higher transaction costs, wider bid/offer spreads, frequent index re-balancing costs, and the inability to perfectly replicate the benchmark index are all factors that are more relevant in emerging markets and diminish the cost-advantages of a passive investment approach, in our view.

Sustainable investing

Investing in emerging markets can make a real difference. Over more than 20 years of managing EM debt portfolios, we’ve witnessed positive change across many developing countries – better healthcare, education and environmental stewardship, and improved quality of life for citizens. For long-term investors, we believe that investing in developing countries with sustainable development paths can contribute to a positive risk-return outcome; countries with improving sustainability/ESG metrics tend to build more sustainable economies and unlock higher productivity, which can lead to outperformance of their assets.

One key sustainability trend is the shift to net-zero carbon emissions, and this is particularly relevant for investors in EM debt. Almost 60% of markets in the JP Morgan EMBI GD index are commodity-exporting economies and – as noted here – the dominance of emerging markets in global emissions highlights both the need for EM economies to make progress towards net zero and the potential for EM debt investors to make a positive real-world contribution to the global transition. The challenge is finding the right tools and approaches to successfully forecast future sustainability trends.

Most passive EM strategies do not incorporate sustainability considerations, and those that do typically rely on ESG ratings that are backward looking and do not provide a complete or accurate picture of a country’s sustainability progress or future objectives. Active investors can focus on countries committed to improving sustainability, develop more meaningful approaches to assessing sustainability trends, and seek to influence policymakers and company management through targeted engagements. From a borrower’s perspective, a better understanding of investors’ approaches to sustainability can help them to formulate sustainability strategies and create meaningful sustainable development for the future. This two-way engagement is only possible with active management and, in our view, is the right way to think about sustainable investing.

In summary

While passive ETFs have grown in popularity as a low-cost way to access various asset classes, our analysis suggests that the average passive EM debt ETF has been unable to compete with the returns of an active manager or take account of sustainability considerations in such a meaningful way. Passive products are sub-optimal vehicles for accessing less liquid markets, have generally underperformed comparable active managers, and are limited to a constrained opportunity set. We firmly believe that active management, underpinned by the right expertise and toolkit, can help investors get the most out of the EM debt asset class.

Appendix

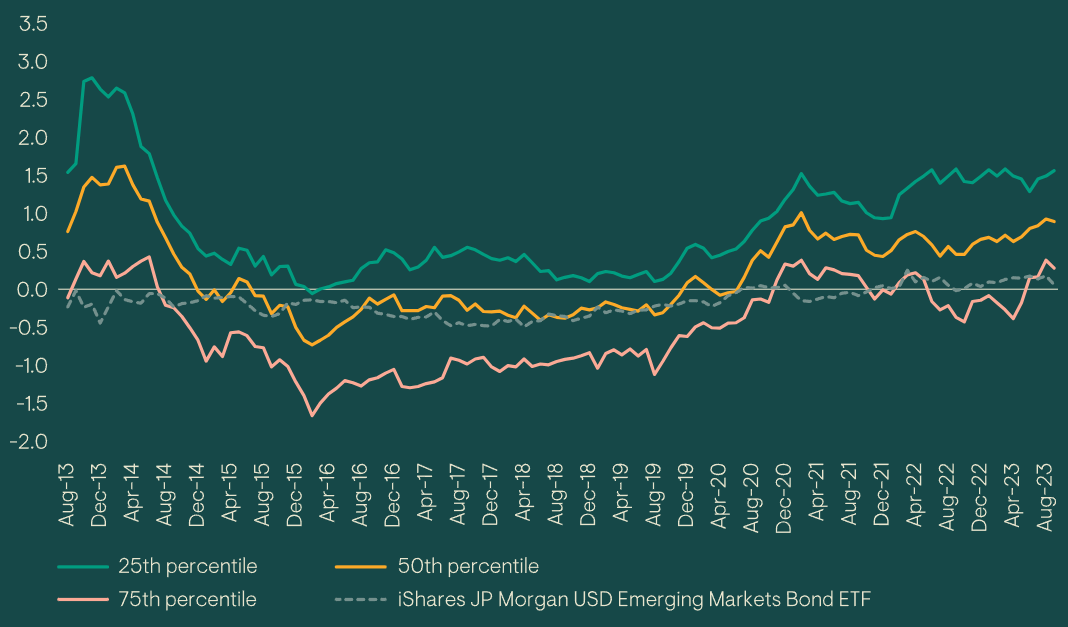

Active vs passive performance in other EM asset classes draws a similar conclusion – the active manager broadly outperforms.

Hard currency returns (gross of fees)

Rolling 3-year chart shown earlier in this piece.

Figure 4: Rolling five-year excess returns – EM hard currency debt managers (gross of fees, %)

Source: eVestment EM HC fixed income universe, as at 30 September 2023. EM Hard Currency Funds – Active manager performance vs iShares JP Morgan EM HC index. Performance is gross of fees (returns will be reduced by management fees and other expenses incurred), income is reinvested, in USD.

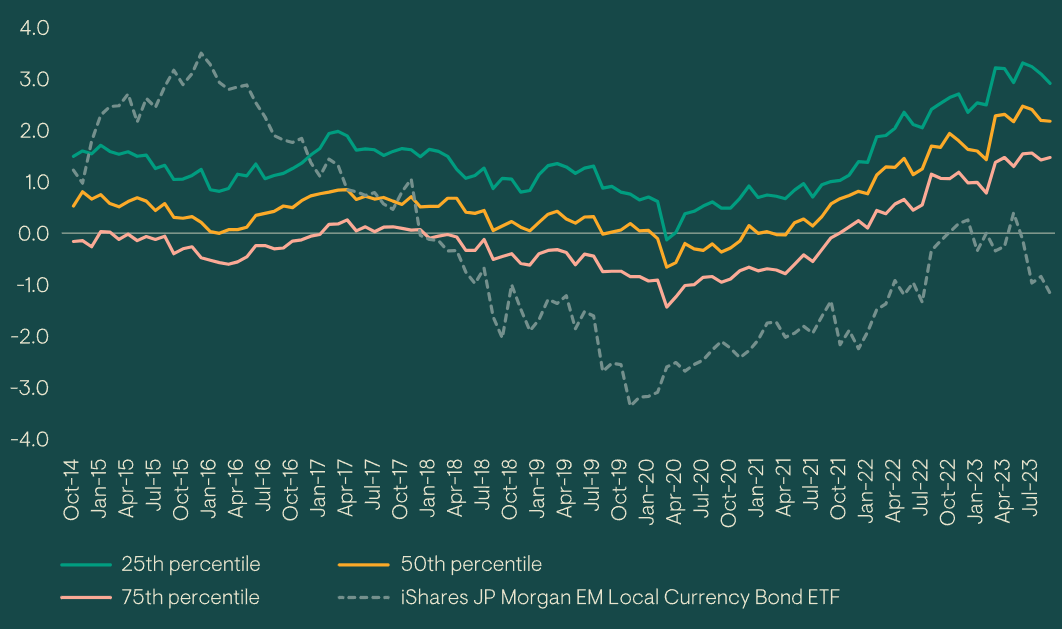

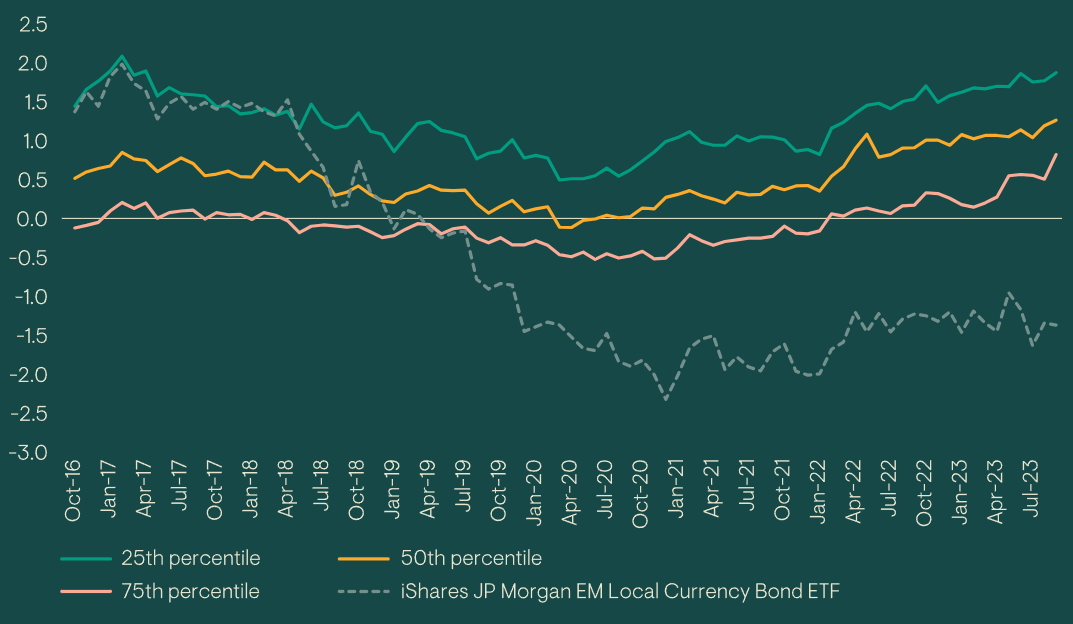

Local currency returns

Figure 5: Rolling three-year excess returns – EM local currency debt managers (gross of fees, %)

Please see below the next chart for source and date.

Figure 6: Rolling five-year excess returns – EM local currency debt managers (gross of fees, %)

Past performance does not predict future returns; losses may be made.

Source: eVestment EM LC fixed income universe, as at 30 September 2023. EM Local Currency Funds – Active manager performance vs iShares JP Morgan EM LC index7. Performance is gross of fees (returns will be reduced by management fees and other expenses incurred), income is reinvested, in USD.

Performance net of fees

Figure 7: Fee and performance comparison of EM local currency debt strategies (%)

Source: Morningstar Direct, October 2023. Average returns based on simple average of USD denominated EMD ETF and EMD Active Manager. ETF & Managers defined as the US Emerging Markets Local Currency Bond Category (inc. ETFs) where the underlying benchmark is JP Morgan GBI-EM or equivalent Local Currency index. Sample size of 68 managers.

1 Broadridge data as of 30 June 2023, compiled EM hard currency, local currency, blended and corporate debt funds

2 The best and worst performers within the index over the most recent five-year period (to 30 November 2023).

3 Ninety One study analysing all bonds in the JP Morgan EMBI (excluding restructured bonds) since 2013.

4 Rolling 3 years is the time period typically considered by our institutional clients. The hard currency universe is the largest component of the EM debt universe.

5 See Appendix for local currency returns comparison, as well as returns on a five-year rolling basis

6 Annualised trailing tracking error, eVestment, October 2013 - Sept 2023.

7 Dating back to inception of JPM iShares EM Lcl Govt Bd ETF $ Acc.

General risks. The value of investments, and any income generated from them, can fall as well as rise. Past performance does not predict future returns, losses may be made. Environmental, social or governance related risk events or factors, if they occur, could cause a negative impact on the value of investments.

Specific risks. Default: There is a risk that the issuers of fixed income investments (e.g. bonds) may not be able to meet interest payments nor repay the money they have borrowed. The worse the credit quality of the issuer, the greater the risk of default and therefore investment loss. Interest rate: The value of fixed income investments (e.g. bonds) tends to decrease when interest rates rise. Emerging market (inc. China): These markets carry a higher risk of financial loss than more developed markets as they may have less developed legal, political, economic or other systems.

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in