Yield is Destiny; Bonds are Back

Investing through the arc of the COVID recovery has hardly been a cakewalk, and the event horizon is hardly clearing for 2023. But as bond investors, we shouldn’t lose sight of the fact that bond yields have experienced a historic increase to what will likely prove to be generational highs. This is the positive side of the 2022 market rout: with bonds, yield is more or less destiny. These higher yields should easily push bond returns in the coming decade to twice, if not three times, higher than those recorded over past decade (Figure 1).

As a result of the COVID recovery, markets have turned back the clock 20 years, pushing yields back up to 2002 levels and setting bonds up for solid returns in the years ahead. While current conditions suggest yields may remain around current levels in the weeks and months ahead, longer-term fundamentals suggest some decline in yields is likely as growth and inflation eventually recede from their current generational highs. In any event, some of the future returns embodied in current market yields will be pulled forward in the form of capital appreciation. In other words, we appear to be at a strategic buy point for bonds.

Figure 1: Yield is destiny (more or less) for long-term fixed income over extended periods of time. Returns from 1992-2012 ended up slightly higher than starting yields as rates generally fell, while returns from 2012 to 2022 were a bit less than starting yields as rates rose at the end of the period. At present, we see the near-term outlook for rates as finely balanced, but mildly bullish longer term. Based on past relationships, broad bond market returns could easily be two to three times those of the last decade. (%)

Source: PGIM Fixed Income. Yields and returns based on Bloomberg US Aggregate Bond Index.

Looking back over the decades, we can see that yields have passed through various paradigms, as indicated by the low, moderate, and high periods in Figure 2. Reviewing the factors that drove the transitions between outlier periods may give us some insight into where we are now, how we got here, and where we are headed.

Figure 2: Pegging Yields: Where Should They Be? (%)

Source: PGIM Fixed Income; 1875-1961, Robert Shiller, Yale; 1962-Present, Bloomberg.

What’s normal?

Over time, the central tendency for long-term U.S. Treasury yields seems to land in the vicinity of 4% (I: the “normal” range in Figure 2). Conceptually, this might stem from the relationship between nominal GDP and private sector borrowing rates as Treasury yields in this zone generally allow a natural equilibrium in debt markets’ supply and demand.

What caused the ultra-low yields during World War II?

The low yields of the Great Depression continued through the second World War as the Fed capped Treasury yields to facilitate government borrowing (Period II in Figure 2). This policy continued into the 1950s as the government feared that without ongoing monetary stimulus, the economy might slip back into recession or even depression. However, the Fed—more concerned with inflationary pressures—eventually won its independence and began shifting policy back towards higher rates and running the kind of counter-cyclical monetary policy observed in subsequent years.

Why were rates so high in the 1970s-1980s?

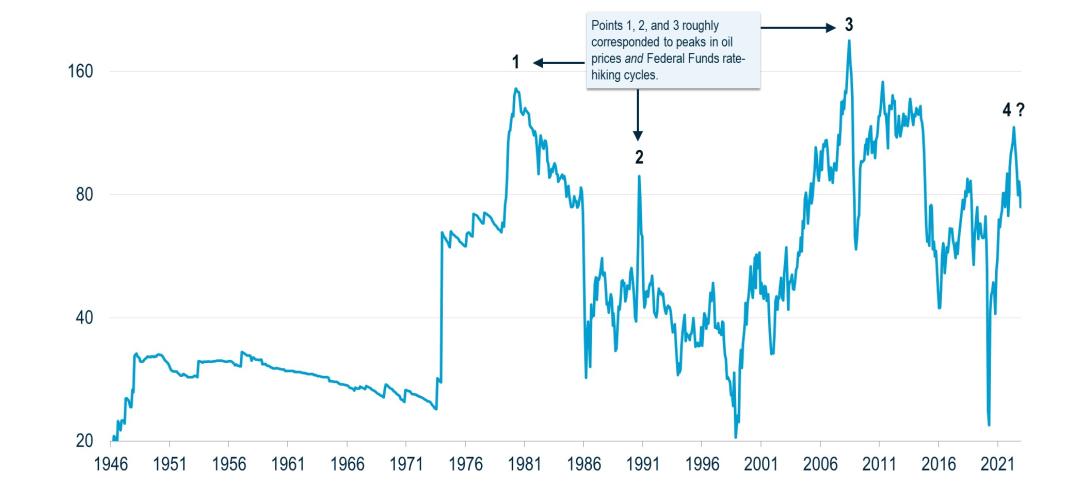

Most of the blame for rising rates in the 1970s is cast on the pre-Volcker Fed chiefs allowing inflation to get out of control. The 1980’s high, albeit falling, rates were regarded as the legacy of Fed Chairs Volcker and Greenspan waging and finishing the war on inflation. Yet, it’s worth highlighting another major part of the story: rising oil prices in the 1970s and falling oil prices in the 1980s (Figure 3). While this may seem superfluous, the fact of the matter is that the COVID recovery has seen negative supply shocks from supply chain disruptions and the Russia/Ukraine war, both of which are analogous to the oil shocks of the 1970s. As a result, we should not under-estimate the potential for inflation to decline if and as these supply constraints and higher input costs ease, just as inflation receded in the 1980s as the price of oil fell.

Figure 3: The COVID recovery has seen negative supply shocks from supply chain disruptions and the Russia/Ukraine war, both of which are analogous to the oil shocks of the 1970s. As a result, we should not underestimate the potential for inflation to decline if and as these supply constraints and higher input costs ease, just as inflation fell in the 1980s. ($)

Source: PGIM Fixed Income and Bloomberg.

As a result of this inflation shortfall, central banks’ administered rates were kept at unusually low levels. In some cases, they were complemented by aggressive quantitative easing and low-rate lending programs, the combination of which drove developed market term structures to unnaturally low levels (Period IV of Figure 2). With inflation seemingly stuck below target and central banks determined to ease policy until they achieved their targets, it looked like interest rates were doomed to an ultra-low future for as far as the eye could see.

Then came the post-COVID explosion in growth, inflation, and interest rates…

The emergence from the COVID crisis provided two reasons for higher rates. The first was the booming growth and inflation. The combination of stimulus and reopening enthusiasm boosted demand, while supply remained muted due to a host of factors, including labor shortages and supply chain interruptions. The second “enabler” of higher rates, if you will, was the repaired damage from the GFC and its sluggish, debt-laden, Reinhart-and-Rogoff conditions.1 Consumer balance sheets and financial institutions’ capital positions were once again strong. That combination has resulted in surprising economic resilience even in the face of substantial central bank tightening in many countries and the higher repricing in long-term interest rates.

Rates are up; but they are just back up to normal levels …

Although rates have risen, a quick review of history reveals that they are not particularly high. Rather, they have just reverted to more normal levels. With the problems of the post-GFC era in the past, maybe the time has come for rates to transition, and the COVID recovery simply provided the impetus for that normalization. If that’s the case, we should not be surprised to see the expansion continue despite the shift back to a higher range of interest rates (Period V of Figure 2).

Are post pandemic periods stronger than usual, and will that keep rates higher for longer?

Another element worth considering: Are post-pandemic periods—such as the plague years as well as the 1918 and 1957 flu pandemics—different? History shows that post-pandemic periods have tended to experience extended periods of strong growth and, in some cases, higher inflation.2 While this is a more speculative aspect of current conditions, nonetheless, it could be playing a role in the resilience of growth in the face of higher rates, inflation, and geopolitical uncertainty.

So, where to for rates? Short-term outlook balanced …

At present, the rate outlook appears quite balanced. High inflation, ongoing growth, and low unemployment will keep central banks biased to raise rates. But the combination of significant hikes to date as well as signs that growth and inflation are beginning to moderate suggest that most of the rate hikes are behind us and that upside risk from current levels is limited. Should growth or inflation decline, however, the potential for a drop in rates would also seem limited given the high starting point for inflation and the low level of unemployment.

But longer term? Bullish bias …

Near-term uncertainties notwithstanding, looking a few years into the future, it seems clear that given the demographic and productivity paths of most DM economies, the pace of growth and inflation will be lower. Therefore, rates may maintain a downward bias, albeit in the normal range. In the event, fixed income returns could not only consist of current yield levels but may also be topped off by capital gains.

Conclusion

Yields progress through varying regimes, and 2022 brought a jarring revaluation. The repricing triggered by the COVID recovery catapulted rates from the unnatural lows of the post-GFC era back into the historically normal range. Over the near to intermediate term, rates are likely to hover around current levels until inflation pressures abate and central bank rate-hiking cycles end. But from a longer-term perspective, DM economies are almost certainly at what will prove to be generational highs in growth, inflation, and bond yields. While the growth uncertainties created by the surge in rates may be a liability for more growth-sensitive investments, the opposite is likely to hold for fixed income where a growth shortfall may very well boost performance.

In summary, the historic increase in long-term rates from the COVID lows to levels not seen for decades will provide a formidable tailwind for fixed income. After all, for bonds, yield is tantamount to destiny, and the recent explosion in yields has turned back the clock two decades, setting bonds up for strong returns in the decade ahead.

1 Reinhart, Carmen M. and Rogoff, Kenneth S., “This Time is Different Eight Centuries of Financial Folly,” Princeton university Press, 2009.

2 “Social and Economic Impacts of the 1918 Influenza Epidemic,” The Digest, No. 5, May 2020, National Bureau of Economic Research.

Read More from PGIM Fixed Income

The comments, opinions, and estimates contained herein are based on and/or derived from publicly available information from sources that PGIM Fixed Income believes to be reliable. We do not guarantee the accuracy of such sources or information. This outlook, which is for informational purposes only, sets forth our views as of this date. The underlying assumptions and our views are subject to change. Past performance is not a guarantee or a reliable indicator of future results.

Source(s) of data (unless otherwise noted): PGIM Fixed Income as of December 20, 2022.

PGIM Fixed Income operates primarily through PGIM, Inc., a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended, and a Prudential Financial, Inc. (“PFI”) company. Registration as a registered investment adviser does not imply a certain level or skill or training. PGIM Fixed Income is headquartered in Newark, New Jersey and also includes the following businesses globally: (i) the public fixed income unit within PGIM Limited, located in London; (ii) PGIM Netherlands B.V., located in Amsterdam; (iii) PGIM Japan Co., Ltd. (“PGIM Japan”), located in Tokyo; (iv) the public fixed income unit within PGIM (Hong Kong) Ltd. located in Hong Kong; and (v) the public fixed income unit within PGIM (Singapore) Pte. Ltd., located in Singapore (“PGIM Singapore”). PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos, and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide.

These materials are for informational or educational purposes only. The information is not intended as investment advice and is not a recommendation about managing or investing assets. In providing these materials, PGIM is not acting as your fiduciary. Clients seeking information regarding their particular investment needs should contact their financial professional. These materials represent the views and opinions of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Fixed Income is prohibited. Certain information contained herein has been obtained from sources that PGIM Fixed Income believes to be reliable as of the date presented; however, PGIM Fixed Income cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Fixed Income has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy or accept responsibility for errors. All investments involve risk, including the possible loss of capital. These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. No risk management technique can guarantee the mitigation or elimination of risk in any market environment. Past performance is not a guarantee or a reliable indicator of future results and an investment could lose value. No liability whatsoever is accepted for any loss (whether direct, indirect, or consequential) that may arise from any use of the information contained in or derived from this report. PGIM Fixed Income and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Fixed Income or its affiliates.

The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients or prospects. No determination has been made regarding the suitability of any securities, financial instruments or strategies for particular clients or prospects. For any securities or financial instruments mentioned herein, the recipient(s) of this report must make its own independent decisions.

Conflicts of Interest: PGIM Fixed Income and its affiliates may have investment advisory or other business relationships with the issuers of securities referenced herein. PGIM Fixed Income and its affiliates, officers, directors and employees may from time to time have long or short positions in and buy or sell securities or financial instruments referenced herein. PGIM Fixed Income and its affiliates may develop and publish research that is independent of, and different than, the recommendations contained herein. PGIM Fixed Income’s personnel other than the author(s), such as sales, marketing and trading personnel, may provide oral or written market commentary or ideas to PGIM Fixed Income’s clients or prospects or proprietary investment ideas that differ from the views expressed herein. Additional information regarding actual and potential conflicts of interest is available in Part 2A of PGIM Fixed Income’s Form ADV.

In the United Kingdom, information is issued by PGIM Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 193418). In the European Economic Area (“EEA”), information is issued by PGIM Netherlands B.V., an entity authorised by the Autoriteit Financiële Markten (“AFM”) in the Netherlands and operating on the basis of a European passport. In certain EEA countries, information is, where permitted, presented by PGIM Limited in reliance of provisions, exemptions or licenses available to PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. These materials are issued by PGIM Limited and/or PGIM Netherlands B.V. to persons who are professional clients as defined under the rules of the FCA and/or to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II). In certain countries in Asia-Pacific, information is presented by PGIM (Singapore) Pte. Ltd., a Singapore investment manager registered with and licensed by the Monetary Authority of Singapore. In Japan, information is presented by PGIM Japan Co. Ltd., registered investment adviser with the Japanese Financial Services Agency. In South Korea, information is presented by PGIM, Inc., which is licensed to provide discretionary investment management services directly to South Korean investors. In Hong Kong, information is provided by PGIM (Hong Kong) Limited, a regulated entity with the Securities & Futures Commission in Hong Kong to professional investors as defined in Section 1 of Part 1 of Schedule 1 (paragraph (a) to (i) of the Securities and Futures Ordinance (Cap.571). In Australia, this information is presented by PGIM (Australia) Pty Ltd (“PGIM Australia”) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). PGIM Australia is a representative of PGIM Limited, which is exempt from the requirement to hold an Australian Financial Services License under the Australian Corporations Act 2001 in respect of financial services. PGIM Limited is exempt by virtue of its regulation by the FCA (Reg: 193418) under the laws of the United Kingdom and the application of ASIC Class Order 03/1099. The laws of the United Kingdom differ from Australian laws. In Canada, pursuant to the international adviser registration exemption in National Instrument 31-103, PGIM, Inc. is informing you that: (1) PGIM, Inc. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration requirement under National Instrument 31-103; (2) PGIM, Inc.’s jurisdiction of residence is New Jersey, U.S.A.; (3) there may be difficulty enforcing legal rights against PGIM, Inc. because it is resident outside of Canada and all or substantially all of its assets may be situated outside of Canada; and (4) the name and address of the agent for service of process of PGIM, Inc. in the applicable Provinces of Canada are as follows: in Québec: Borden Ladner Gervais LLP, 1000 de La Gauchetière Street West, Suite 900 Montréal, QC H3B 5H4; in British Columbia: Borden Ladner Gervais LLP, 1200 Waterfront Centre, 200 Burrard Street, Vancouver, BC V7X 1T2; in Ontario: Borden Ladner Gervais LLP, 22 Adelaide Street West, Suite 3400, Toronto, ON M5H 4E3; in Nova Scotia: Cox & Palmer, Q.C., 1100 Purdy’s Wharf Tower One, 1959 Upper Water Street, P.O. Box 2380 - Stn Central RPO, Halifax, NS B3J 3E5; in Alberta: Borden Ladner Gervais LLP, 530 Third Avenue S.W., Calgary, AB T2P R3.

© 2022 PFI and its related entities.

2022-8212

Sign Up Now for Full Access to Articles and Podcasts!

Unlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in