DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

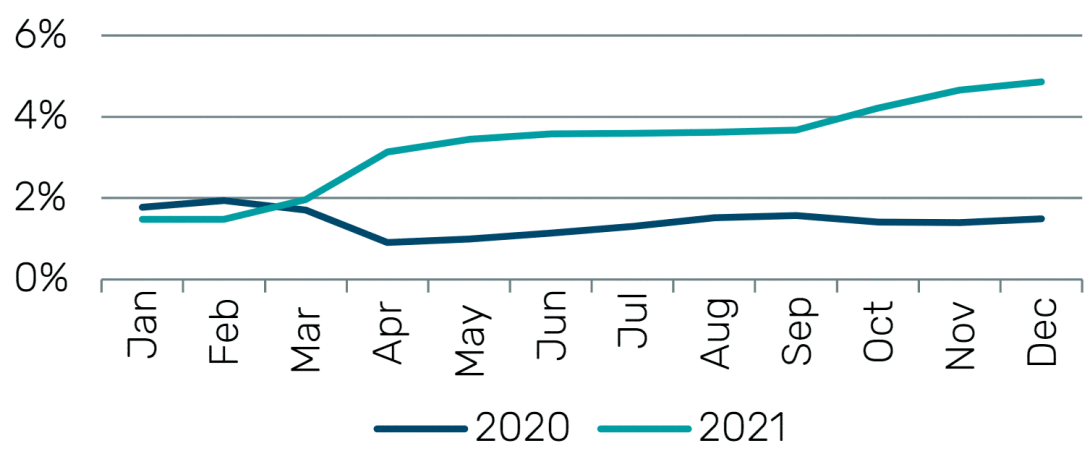

In February 2022, the Bureau of Labor Statistics reported that inflation, as measured by the Consumer Price Index (CPI), accelerated to a 7.5% annualized rate in January 2022, a 40-year high. Prices for food, electricity, and housing were the largest contributors to the rise. The latest increase continues a trend that began in April 2021, when the CPI jumped to an annualized rate of 4.2%. The Fed’s preferred measure of inflation is the core Personal Consumption Expenditure (PCE) Index, which excludes volatile food and energy prices. The core PCE has increased, jumping from 2.0% in March 2021 to 3.1% in April 2021 and climbing steadily to 4.9% in December 2021.

Source: St. Louis Federal Reserve, FRED Database, Personal Consumption Expenditures excluding food and energy (Chain-type Price Index).

In response, Federal Reserve Chairman Jerome Powell has acknowledged that inflationary pressures are no longer “transitory,” and officials have indicated that increases in the federal funds rate are coming in 2022. But this “Powell Pivot” is not unique to the Fed as the rise in inflation is not present just in the U.S. but also overseas, resulting in a shift in thinking from those Central Banks as well.

These concerns about inflation have worsened in recent months, in part due to stronger-than-expected employment data. New jobs totaled 467,000 in January 2022, easily surpassing the median forecast of 150,000.

This data is contributing further to a belief that inflation is not transitory. It remains uncertain how long pricing pressures will persist, but we have all seen inflation in our personal lives, and economists now believe that serious, persistent inflation is here.

In response to rising prices the market appears to be starting to factor in various sizes and pace of future Fed rate hikes. Furthermore, we are seeing a significant lift in yields on longer-duration assets; the reaction to inflation data released in February, which surprised to the upside, saw the yield on the Two-year Treasury note break 150 basis points and the yield on the 10-year Treasury temporarily exceeding 2%.

Based on DWS’s analysis, credit fundamentals in the investment-grade market appear healthy. Earnings have been strong, and we have not seen too much credit damage. That is, we have not seen any leveraging or other trends that are diluting credit holders although there is some growing concern that we could see some more leveraged M&A activity.

During the pandemic, companies engaged in significant deleveraging, and leverage has come down considerably meaning that corporate financial flexibility is strong. The question is, how will companies manage that flexibility? Will they put it into capital expenditures and organic growth, or will they opt for external growth, that is, mergers and acquisitions? And will these transactions be bolt-on acquisitions, or will they be mergers or larger acquisitions?

What we hear from our credit analysts is that "everyone is looking," but high equity valuations are another factor to consider. Therefore, companies may opt to use their cash in another way, such as stock buybacks.

While credit fundamentals appear strong, investor should also be very mindful of the role technical factors can have this year. Supply has been robust, with 2021 being a record year, and the expectation is that 2022 may be strong as well.

Ratings upgrades could also affect supply. The number of “rising stars”–companies moving from the high-yield market into investment-grade–is likely to be larger than the number that dropped from investment-grade into high-yield status during the pandemic. These rising stars would, therefore, be a hidden source of supply, and demand for investment-grade bonds will need to be quite strong to absorb the new issue supply along with the supply coming from rising stars.

While demand has been strong, the sentiment is that yields will be going higher. Investors should take note of several factors affecting demand. First, hedging costs are going up. So, the appeal of investment-grade bonds to foreign investors who need to hedge their exposure to the U.S. Dollar may be hindered by these hedging costs. Consequently, we do expect some softening of this source of demand.

Second, while it was not that long ago that large portions of the global fixed-income market had negative yields, that has been dissipating. Real yields on 10-year sovereign bonds are flirting with positive territory (as of the middle of February 2022). Subsequently, the amount of debt in the market that carries a negative real yield is coming down. This creates an alternative to U.S. Dollar debt, potentially decreasing the demand for investment-grade bonds from non-U.S. investor set.

This could in turn, however, prove to be a “silver lining.” Given the supply and demand dynamics mentioned, DWS’s view is that this could increase yield on credit and in turn bring other investors to the market. The asset class has a dedicated investor base comprised of a large number of institutional and pension plan investors. Given the forecasts of creditworthiness and higher yields, interest can be rekindled from longer-dated bond holders, such as insurers or even certain pensions looking for liability matching options, as they seek higher-quality options.

When might investors take advantage of that opportunity? That will depend on the volatility of the market, their inflation expectations, and view on the future path of interest rates. From our March 2022 vantage point, the most likely scenario where institutional investment criteria and yield opportunities converge will be in the second half of the year.

The investment-grade credit market is not immune to the headwinds facing the bond market in the near future. Inflation, rate hikes by the Fed, and a migration of alternative credit options will weigh on the asset class. Nevertheless, credit fundamentals look strong, and the market is likely to benefit as a rise in yields increasingly draws institutional investors into the market. Download PDF

Tom Farina Portfolio Manager and Head of U.S. Investment Grade Credit

For Institutional Investor use only. Past performance is not indicative of future returns.Forecasts are based on assumptions, estimates, opinions,, and hypothetical models that may prove to be incorrect. Investments come with risk. The value of an investment can fall as well as rise and your capital may be at risk. You might not get back the amount originally invested at any point in time.

Disclaimer DWS is the brand name of DWS Group GmbH & Co. KGaA and its subsidiaries under which they do business. TheDWS legal entities offering products or services are specified in the relevant documentation. DWS, through DWSGroup GmbH & Co. KGaA, its affiliated companies and its officers and employees (collectively “DWS”) arecommunicating this document in good faith and on the following basis. This document is for information/discussion purposes only and does not constitute an offer, recommendation orsolicitation to conclude a transaction and should not be treated as investment advice. This document is intended to be a marketing communication, not a financial analysis. Accordingly, it may notcomply with legal obligations requiring the impartiality of financial analysis or prohibiting trading prior to thepublication of a financial analysis. This document contains forward looking statements. Forward looking statements include, but are not limited toassumptions, estimates, projections, opinions, models and hypothetical performance analysis. No representation orwarranty is made by DWS as to the reasonableness or completeness of such forward looking statements. Pastperformance is no guarantee of future results. The information contained in this document is obtained from sources believed to be reliable. DWS does notguarantee the accuracy, completeness or fairness of such information. All third-party data is copyrighted by andproprietary to the provider. DWS has no obligation to update, modify or amend this document or to otherwise notifythe recipient in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forthherein, changes or subsequently becomes inaccurate. Investments are subject to various risks. Detailed information on risks is contained in the relevant offeringdocuments. No liability for any error or omission is accepted by DWS. Opinions and estimates may be changed without noticeand involve a number of assumptions which may not prove valid.DWS does not give taxation or legal advice. This document may not be reproduced or circulated without DWS’s written authority. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen orresident of or located in any locality, state, country or other jurisdiction, including the United States, where suchdistribution, publication, availability or use would be contrary to law or regulation or which would subject DWS toany registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, suchrestrictions. This document may not be reproduced or circulated without DWS written authority. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. War, terrorism, sanctions, economic uncertainty, trade disputes, public health crises and related geopolitical events have led, and, in the future, may lead to significant disruptions in US and world economies and markets, which may lead to increased market volatility and may have significant adverse effects on the fund and its investments. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisfsdiction, including the United States, where such distribution, publication, availability or use would be contrary to law or regulation or which would subject DWS to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions. © 2022 DWS International GmbH Issued in the UK by DWS Investments UK Limited which is authorised and regulated in the UK by the FinancialConduct Authority. © 2021 DWS Investments UK Limited This document is issued by DWS Investments Hong Kong Limited (“DWS HK”) and is the property and copyright of DWS HK. This document may not be reproduced or circulated without DWS HK’s written consent. The mannerof circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. All rights reserved. © 2022 DWS Investments Hong Kong Limited In Singapore, this document has not been reviewed by any regulatory authority. This ddocument has been prepared solely for informatonal purposes and does not constitute an offer or arecommendation to enter into any transaction. The terms of any investment will be exclusively subject to thedetailed provisions, including risk considerations, contained in the offering documents. When making aninvestment decision, you should rely on the final documentation on relating to the transaction. The value of an investment and any income from it can go down as well as up. Past performance is not a reliable indicator offuture result © 2022 DWS Investments Singapore Limited In Australia, this document is issued by DWS Investments Australia Limited (ABN: 52 074 599 401) (AFSL 499640) and the content of this document has not been reviewed by the Australian Securities Investment Commission. © 2022 DWS Investments Australia Limited In Taiwan, this document is distributed to professional investors only and not others. Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or asolicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed, and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted. For investors in Bermuda This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda. Additionally, non-Bermudian persons (including companies) may not carry on or engage in any trade or business in Bermuda unless such persons are permitted to do so under applicable Bermuda legislation.

© 2022 DWS Group GmbH & Co. KGaA. All rights reserved. I-088429-1

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in