John Cassedy

Head of Insurance-Americas

+1 617 295 3143, john.cassedy@dws.com

Bernie Ryan

Head of Insurance Business Development-Americas

+1 617 295 2105, bernie.ryan@dws.com

Nestanlin Garcia

Head of Institutional Sales & Insurance-Germany

nestanlin.garcia@dws.com

Alexia Giugni

Head of Client Coverage-EMEA

alexia.giugni@dws.com

Thomas Gillmann

Insurance Advisory & Strategy-Asia Pacific

thomas.gillmann@dws.com

About DWS

Insurance asset management coordinated globally

As a pioneer in insurance asset management, DWS started working with insurance companies in 1929. Trust, knowledge and customized solutions crafted over time are what we deliver insurers.

Our global platform delivers multi-asset investment programs in an insurance context across active and passive fixed-income, equity, alternatives, cash, and sustainable strategies. It is supported by an understanding of the dynamics and complexities of insurance investing in a constrained environment that is subject to state regulations, solvency requirements, rating agency considerations, reporting and accounting standards.

Convexity and prepayment risk

The Navigator: The current state of the commercial real estate market

Dividends and Inflation – Let’s Get Real

CIO Special - Growth vs Value

The Muni Market: What’s in Store for 2024?

Infrastructure Strategic Outlook 2024

U.S. High Yield for Insurance Companies

U.S. Real Estate Strategic Outlook

PODCAST

PODCASTExtending the Concept of Private Credit into Real Assets

Welcome to another edition of the InsuranceAUM.com podcast. Today's topic is real assets, private debt, and we're joined today by Matt Addesa, Private Market Specialist at DWS.

U.S. Real Estate Strategic Outlook

U.S. real estate has responded to higher interest rates. Market prices have dropped about 20% from their Spring 2022 peak. We believe that appraisal values will converge to market levels by year-end.

A Renaissance in U.S. Core Fixed Income: The “Five Percent” Paradox to Start the Year

Despite uncertainties regarding monetary policy and a potential recession, assessing valuations across the bond universe at the start of the year has yielded some interesting fundamentally-driven ideas for 2023, despite the recent bouts of volatility.

Research report - U.S. Real Estate Strategic Outlook January 2023

U.S. real estate investment performance has stumbled in response to rising interest rates. However, property fundamentals are robust. While a mild recession might soften leasing momentum, we believe that markets will remain historically tight as construction slides.

PODCAST

PODCASTLiquidity and Volatility in the Bond Market with Shilpa Lakhani, Head of Portfolio Management-Fixed Income Solutions at DWS

Today's topic is liquidity and volatility conditions in the bond market. And we are joined today by Shilpa Lakhani, Head of Fixed Income Portfolio Solutions in the Americas for DWS.

Time to consider Municipal Bonds again?

2022 has so far been a painful year for fixed income investors. No market has been spared the pain of rising interest rates and the municipal bond market has been no exception.

Solactive launches GBS United States 500 Enhanced Investment Grade with Zurich and DWS

Investors are facing a volatile financial environment amid inflation, ongoing Covid-19 restraints, and geopolitical conflicts. In uncertain times, companies with higher credit scores tend to be more resilient, financially healthier, and suffer less with economic fluctuations than their counterparts with low credit scores. Within this framework, Solactive is pleased to announce the launch of the GBS United States 500 Enhanced Investment Grade Index, which will be used for an investment management mandate from Zurich managed by a global asset manager firm DWS America.

U.S. Real Estate Strategic Outlook Mid-Year 2022

Despite surging interest rates and slumping financial markets, real estate displayed positive momentum in the first quarter of 2022. Fundamentals were robust: Vacancies dropped to an all-time low (since 1988), fueling double-digit Net Operating Income (NOI) growth.

U.S. Real Estate and Inflation: Back to the Future?

Just two years after the onset of COVID, the U.S. has jumped from the proverbial frying pan into the fire. Pandemic restrictions have been lifted and the economy has largely recovered. But fiscal and monetary remedies, tight labor markets, stretched supply chains, and now war in Europe have pushed inflation to a 40-year high.

The Fed, the Inflation Picture, and the Potential Impact on Insurance Fixed Income Portfolios

For much of 2021, the Federal Reserve (the Fed) had expected that inflation would be “transitory.” In previous discussions going back to July 2021, DWS’s outlook for inflation was to the contrary—that it would be longer-lasting and not transitory. Since then, our inflation outlook hasn’t changed.

Upward Oil Shock and Energy Credit Impact

Forecasting “what’s next” and assessing potential credit impact on investment-grade energy sector bonds.

Dynamics and Opportunities of Investment-Grade Credit in 2022

While yields are likely to continue rising, credit fundamentals in the investment-grade market look strong. Earnings and balance sheets look healthy, and higher yields could attract institutional investors.

U.S. Real Estate Strategic Outlook

U.S. real estate performed remarkably well in 2021. Although the year began tepidly amid a surge of COVID infections, the steady rollout of vaccines unleashed a resurgence of economic, leasing, and transactions activity in the spring and summer. By the third quarter, overall vacancy rates had dropped to nearly their lowest levels in more than 30 years.

Infrastructure Strategic Outlook 2022

PODCAST

PODCASTSorting through the income opportunity among private, junior capital credits

U.S. Real Estate Strategic Outlook

U.S. real estate started the year on a strong footing. Fundamentals and prices stabilized as the economy gathered momentum. Investment performance returned to pre-COVID levels.

Exploring the financial materiality of social factors

_ Covid-19 has led many types of inequalities to widen over the past year with implications for economic growth, investment returns, government policies and meeting the Sustainable Development Goals (SDGs)

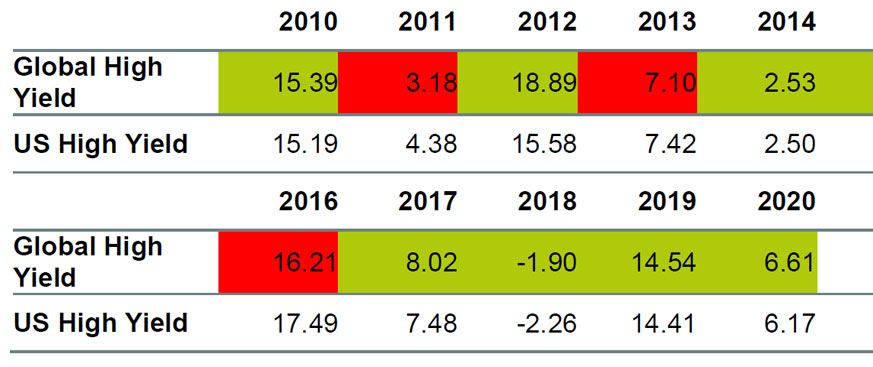

Why Global High Yield is here to stay

Selectivity and diversification – Two key elements in managing high yield bonds to protect on the downside and take advantage of market dislocations. Going global offers diversification and alpha opportunities, not only during times of volatility and uncertainty.

PODCAST

PODCASTFixed Income ETFs: Passing the test and making more sense

Research report Asian credit for European Insurers

Asian Investment Grade Bonds: An Attractive Fit For European insurers?

Research report: Opportunities in Structured Finance

For insurers interested in casting the net wider in the search for income, delving a little deeper into non-established parts of Structured Finance or down in the stack of established segments might have the potential to provide increased income.

Solvency II under review: EIOPA’s Final Opinion on the 2020 Review

In its final opinion on the 2020 Review of Solvency II, EIOPA proposes changes to various parts of the Delegated Regulation.

The Opportunities and Risks of Investing in Fallen Angels for Insurance Companies

Insurance companies have historically allocated toward higher quality yield instruments. Over the past decade, amid a persistent low interest rate environment, insurance companies have gradually increased their allocations outside of investment grade bonds into primarily the higher quality end of the high yield corporate bonds.

U.S. Investment-Grade Credit: Actively Managing the Investment Opportunity

With the emergence of the COVID-19 pandemic and the resulting policy response, 2020 has been a tumultuous year for the U.S. investment-grade market. Yield spreads widened dramatically when the pandemic was declared but recovered quickly when the Federal Reserve launched various programs to support this asset class and other segments of the fixed income market.

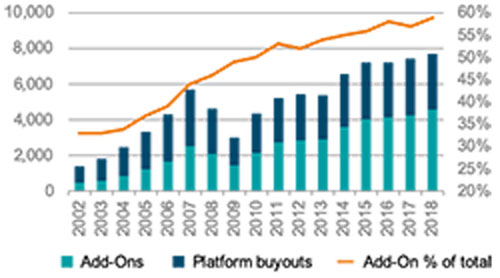

The 4th LP: Investing Between The Silos

By any metric, it has been a great run in buyout PE over the past 20 years. Strong performance relative to public markets over this period has driven impressive industry growth with buyout NAV at $1.7T as of the end of 20181. The performance has attracted a wave of capital. Dry powder in the space in excess of $700B represents almost 3X the LTM deal volume2. Rising PE allocations have driven valuations up as more capital competes for deal flow. As a result, it has been a great “seller’s market” with consistently strong investment returns. But what happens when a sponsor is not a seller but a committed “buyer” of a portfolio investment they have been managing for a few years?

Exploring The Various Uses of Private Real Estate Debt in an Insurance Portfolio

The real estate debt asset class can provide debt investment options that may outperform traditional benchmarks while potentially offering attractive returns, downside protection, diversification benefits, and lower volatility.

The Potential Impacts of the Trump Tax Bill on Municipal Bond Investing

The bill approved by Congress on December 20, 2017, should have significant supply and demand effects on the municipal bond market, and the changes in relative value in relation to the taxable bond market will likely require insurers to reconsider their portfolio strategies in important ways.

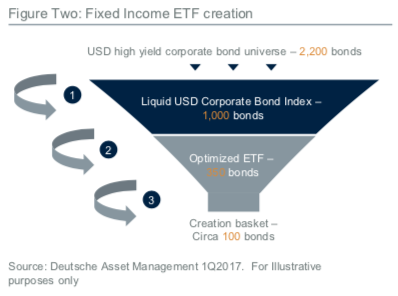

Clarifying The Bond ETF Discussion For Insurance Investing

Bond ETFs are increasingly popular tools for insurers looking for exposure to fixed income without worrying about fluctuations in market liquidity. Recent NAIC accounting guidance could make bond ETFs even more attractive to insurers, since it gives them greater clarity over how to treat the instruments.