DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

Just two years after the onset of COVID, the U.S. has jumped from the proverbial frying pan into the fire. Pandemic restrictions have been lifted and the economy has largely recovered. But fiscal and monetary remedies, tight labor markets, stretched supply chains, and now war in Europe have pushed inflation to a 40-year high.1 The Federal Reserve, which in late-2021 characterized inflation as “transitory”, has responded with interest rate hikes and signaled many more to come, as well as a runoff of its bloated balance sheet.2 Long-term rates have dutifully jumped, although not enough to prevent a flattening of the yield curve, signaling a potential economic slowdown ahead.3

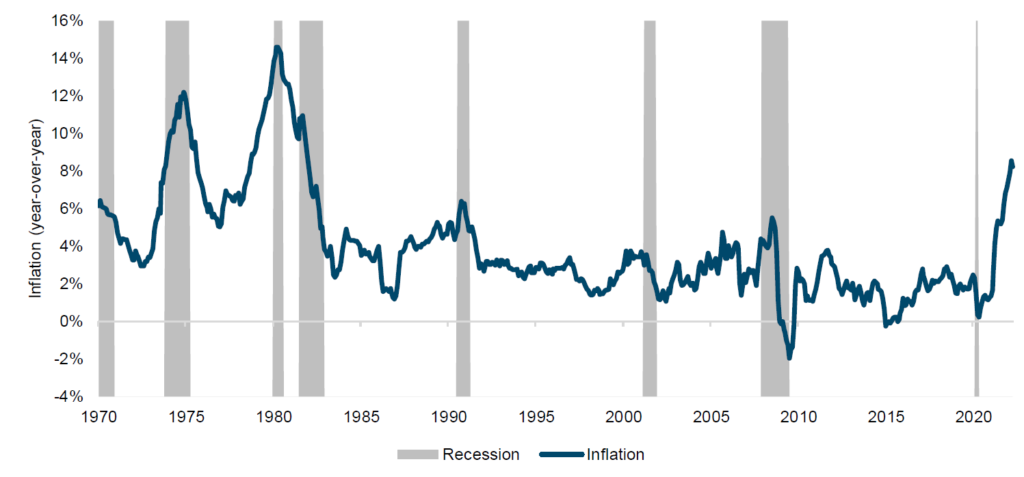

The rapidly shifting financial environment may seem unprecedented to most practicing investors. But we have been here before. Indeed, recent events are reminiscent of another tumultuous period in U.S. economic history: the “stagflation” of the 1970s and early-1980s (see Exhibit 1). From 1970 to 1984 America experienced war (Vietnam, ending in 1975), monetary laxity (after the Gold Standard was abandoned in 1971), two oil shocks (1973 and 1979), spiraling inflation (peaking at 15% in 1980), and surging interest rates (10-year Treasuries topped 15% in 1981).4 Economic growth, though reasonably buoyant overall (averaging 3% annually), was extraordinarily volatile: the period saw four recessions, averaging one every three years, compared with one every nine years in the four decades since.5

Source(s): U.S. Bureau of Labor Statistics (CPI); NBER (recessions) as of April 2022

The analogy is not perfect. The U.S. was arguably more vulnerable to inflation back then: the economy’s energy intensity and union membership were more than double what they are today.6 After 30 years of relative price stability, businesses and workers may be deeply conditioned to expect more of the same, reducing the risk of a wage-price spiral. It is also possible that the Federal Reserve will act more quickly and forcefully to reduce demand, or that geopolitical and other catalysts will abate on their own. But as Mark Twain is reputed to have said, “History does not repeat itself, but it often rhymes.” It is in this spirit that we look to the 1970s for clues about what to expect from real estate in the coming years.

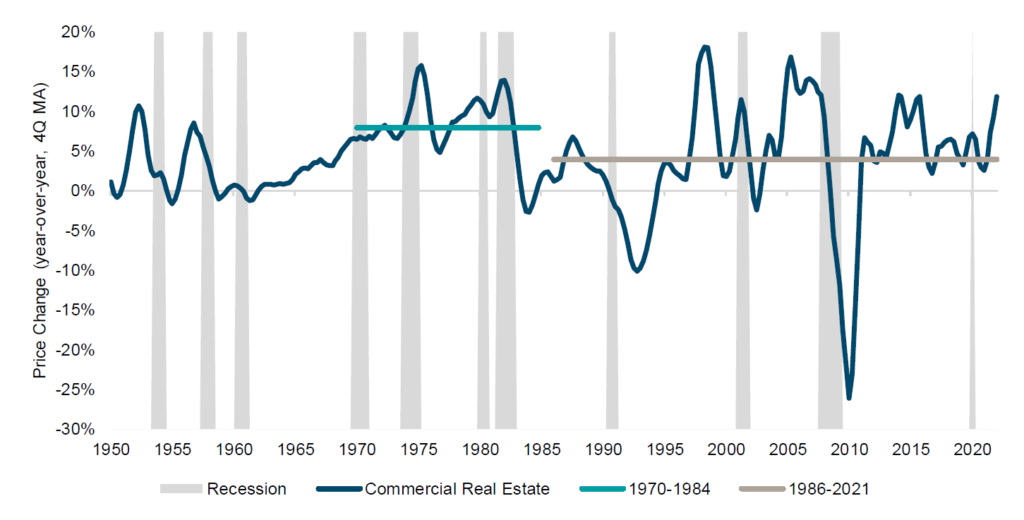

The good news is that despite war, inflation, high interest rates, and economic volatility, the 1970s were quite good for U.S. commercial real estate (see Exhibit 2). History shows that price corrections have always been triggered by recessions (although their magnitude have been influenced by other factors, such as supply and financial conditions).7 Yet the reverse has not always been true: not all recessions have caused prices to fall. Before the COVID recession, which might have passed too quickly to register in real estate valuations, the notable exceptions were the three recessions of the 1970s and early 1980s. True, real estate eventually capitulated after the second leg of the 1980s “double-dip”. But the pullback was mild: 3.5%, only a tenth of the Global Financial Crisis (GFC) slump.8 From 1970 to 1984, real estate prices increased 8% annually, double the average of the past 35 years.9 Cap rates are not available for most of the 1970s, but assuming they were roughly in line with 1980 levels (8%), total returns would have averaged about 15% annually from 1970-1984, compared with 9% for large-cap stocks and 7% for long-term Treasuries.10 On the residential side, growth in single-family home prices remained positive throughout, even as fixed-rate mortgage rates pierced 18% in 1981.11

Source: Federal Reserve (commercial real estate prices); NBER (recessions). As of March 2022.

How could real estate prove so resilient? The historical record does not provide visibility into underlying dynamics, such as vacancies, rents, or cap rates. However, it is possible to draw inferences based on theory and economic circumstances at the time.

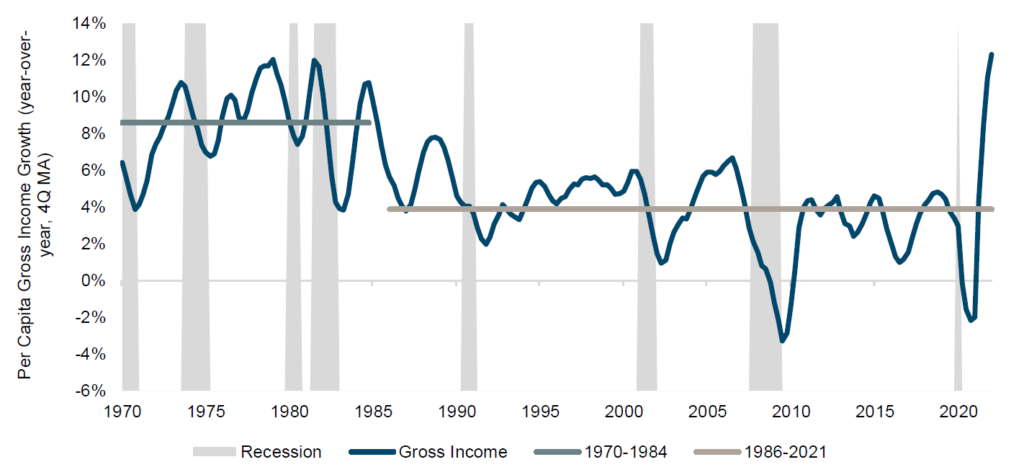

First, per capita incomes increased sharply; they oscillated around recessions, but averaged 8.6% annually over 15 years (see Exhibit 3).12 Although this may seem counterintuitive given the turbulent economy (the unemployment rate increased from 3.9% in 1970 to 10.8% in 1982), it was inherent to systemic inflation: while many people were out of work, the lucky ones who were employed won sizeable pay hikes, both driving (due to higher costs) and allowing (because of higher household incomes) companies to increase prices.13 Rising revenue and wages may have lifted commercial and residential renters’ ability and willingness to pay higher rents.

Source: U.S. Bureau of Economic Analysis (national income); U.S. Census Bureau (population estimates); NBER (recessions). As of March 2022.

Second, inflation pushed up construction costs (see Exhibit 4). Interestingly, commercial and residential development progressed at a healthy pace (averaging about 1.5% of GDP from 1970-1984, compared with 1.0% in 2021).14 However, new projects surely demanded higher rents to compensate for rising costs, which renters were willing and able to absorb as incomes increased. It would be reasonable to assume that higher market rents and replacement costs lifted the values of existing assets.

Source: U.S. Bureau of Labor Statistics (PPI); NBER (recessions). As of March 2022.

Source: U.S. Bureau of Labor Statistics (PPI); NBER (recessions). As of March 2022.

But what about cap rates? Evidence is limited, but the earliest data suggests that real estate yields averaged 8% in 1981 ata time when yields on 10-year Treasuries were 15%.15 Why would investors accept a lower yield on property, subject to leasing and other risks, than on liquid, “risk-free” government bonds? The reason is straightforward: whereas Treasury coupons and principal were fixed, real estate rents and values were not. In theory, cap rates are a function of interest rates (+), a risk premium (+), and expected rent growth (-). Investors might have calculated that high interest rates were a corollary to high inflation, which would feed into stronger rent growth — neutralizing any upward pressure on cap rates.

The economic landscape today betrays striking parallels to the 1970s. Per capita income and average wages increased 8% and 6% year-over-year, respectively, in March 2022.16 The cost of construction materials jumped nearly 18% year-over-year in April and were up nearly 50% since pre-COVID.17 Interest rates are low but rising quickly. The economy is strong — unemployment is near pre-crisis lows — yet a flat yield curve hints at potential volatility ahead.

Investment advisors caution that “past performance does not guarantee future results.” It is unlikely that the 2020s will mirror every twist and turn of the 1970s. Moreover, real estate’s apparent resilience should be taken in perspective. Price gains from 1970 to 1984 were less impressive after adjusting for inflation: values barely increased in real terms.18

Finally, although index numbers are comforting, they obscure vulnerabilities beneath the surface. In the coming years, real estate may be prized more for its inflationary growth than for its yield, particularly if interest rates eclipse cap rates. This shift in financial profile may create instability, as investors with different risk and return objectives, as well as financing structures, react differently to this apparent trade-off. Moreover, if real estate’s resilience is predicated on its ability to generate higher rents, what will happen to buildings occupied on long-term leases at fixed (or nearly fixed) rental rates? And if the next decade is marked by economic volatility, could more frequent recessions undermine occupancies? In short, Inflation 2.0 could bring as many tailwinds as headwinds, but that could still make for a bumpy ride.

Kevin White, CFA

Global Co-Head of Real Estate Research

1 Bureau of Labor Statistics. As of April 2022.

2 FOMC Statements. November 2, 2021 and March 16, 2022.

3 Federal Reserve (yield curve). As of April 2022.

4 Bureau of Labor Statistics (consumer price index); Federal Reserve (10-year Treasury yield). As of April 2022.

5 Bureau of Economic Analysis (GDP); National Bureau of Economic Research (recessions). As of April 2022.

6 U.S. Energy Information Administration (energy intensity); Bureau of Labor Statistics (union membership). As of December 2021.

7 Federal Reserve (commercial real estate prices); National Bureau of Economic Research (recessions). As of March 2022.

8 Federal Reserve (commercial real estate prices). As of March 2022.

9 Federal Reserve (commercial real estate prices). As of March 2022.

10 Ibbotson SBBI US Large Cap Stocks (large cap stocks); Ibbotson SBBI US Long-term (20-Year) Government Bonds (Treasuries). As of March 2022.

11 National Association of Realtors (median single-family home prices); Freddie Mac (30-year Fixed Rate Mortgage). As of March 2022.

12 Bureau of Economic Analysis (income growth). As of March 2022.

13 Bureau of Labor Statistics (unemployment rate). As of March 2022.

14 Bureau of Economic Analysis. As of March 2022.

15 NCREIF (cap rate); Federal Reserve (10-year Treasury yield). A of March 2022.

16 Bureau of Economic Analysis (income); Atlanta Fed (wages). As of March 2022.

17 Bureau of Labor Statistics (construction materials price). As of April 2022.

18 Federal Reserve (commercial real estate price); Bureau of Labor Statistics (consumer price index). As of March 2022.

This information is subject to change at any time, based upon economic, market and other considerations and should not be construed as a recommendation. Past performance is not indicative of future returns. Forecasts are not a reliable indicator of future performance. Forecasts are based on assumptions, estimates, opinions, and hypothetical models that may prove to be incorrect. Investments come with risk. The value of an investment can fall as well as rise and your capital may be at risk. You might not get back the amount originally invested at any point in time. Source: DWS International GmbH.

The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries, such as DWS Distributors, Inc., which offers investment products, or DWS Investment Management Americas, Inc. and RREEF America L.L.C., which offer advisory services. There may be references in this document which do not yet reflect the DWS Brand.

Please note certain information in this presentation constitutes forward-looking statements. Due to various risks, uncertainties and assumptions made in our analysis, actual events or results or the actual performance of the markets covered by this presentation report may differ materially from those described. The information herein reflects our current views only, is subject to change, and is not intended to be promissory or relied upon by the reader. There can be no certainty that events will turn out as we have opined herein.

Marketing Material. In EMEA for Professional Clients (MiFID Directive 2014/65/EU Annex II) only; no distribution to private/retail customers. In Switzerland for Qualified Investors (art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). In APAC for institutional investors only. Australia and New Zealand: For Wholesale Investors only. In the Americas for Institutional Client and Registered Rep use only, not for public viewing or distribution. Israel: For Qualified Clients (Israeli Regulation of Investment Advice, Investment Marketing and Portfolio Management Law 5755 -1995). *For investors in Bermuda: This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda.

For North America:

The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries, such as DWS Distributors, Inc., which offers investment products, or DWS Investment Management Americas, Inc. and RREEF America L.L.C., which offer advisory services.

This material was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. It is intended for informational purposes only. It does not constitute investment advice, a recommendation, an offer, solicitation, the basis for any contract to purchase or sell any security or other instrument, or for DWS or its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein. Neither DWS nor any of its affiliates gives any warranty as to the accuracy, reliability or completeness of information which is contained in this document. Except insofar as liability under any statute cannot be excluded, no member of the DWS, the Issuer or any office, employee or associate of them accepts any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage whether direct, indirect, consequential or otherwise suffered by the recipient of this document or any other person.

The views expressed in this document constitute DWS Group’s judgment at the time of issue and are subject to change. This document is only for professional investors. This document was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. No further distribution is allowed without prior written consent of the Issuer.

Investments are subject to risk, including market fluctuations, regulatory change, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you might not get back the amount originally invested at any point in time.

An investment in real assets involves a high degree of risk, including possible loss of principal amount invested, and is suitable only for sophisticated investors who can bear such losses. The value of shares/ units and their derived income may fall or rise.

War, terrorism, sanctions, economic uncertainty, trade disputes, public health crises and related geopolitical events have led, and, in the future, may lead to significant disruptions in US and world economies and markets, which may lead to increased market volatility and may have significant adverse effects on the fund and its investments.

For Investors in Canada. No securities commission or similar authority in Canada has reviewed or in any way passed upon this document or the merits of the securities described herein and any representation to the contrary is an offence. This document is intended for discussion purposes only and does not create any legally binding obligations on the part of DWS Group. Without limitation, this document does not constitute an offer, an invitation to offer or a recommendation to enter into any transaction. When making an investment decision, you should rely solely on the final documentation relating to the transaction you are considering, and not the document contained herein. DWS Group is not acting as your financial adviser or in any other fiduciary capacity with respect to any transaction presented to you. Any transaction(s) or products(s) mentioned herein may not be appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understand such transaction(s) and have made an independent assessment of the appropriateness of the transaction(s) in the light of your own objectives and circumstances, including the possible risks and benefits of entering into such transaction. You should also consider seeking advice from your own advisers in making this assessment. If you decide to enter into a transaction with DWS Group, you do so in reliance on your own judgment. The information contained in this document is based on material we believe to be reliable; however, we do not represent that it is accurate, current, complete, or error free. Assumptions, estimates, and opinions contained in this document constitute our judgment as of the date of the document and are subject to change without notice. Any projections are based on a number of assumptions as to market conditions and there can be no guarantee that any projected results will be achieved. Past performance is not a guarantee of future results. The distribution of this document and availability of these products and services in certain jurisdictions may be restricted by law. You may not distribute this document, in whole or in part, without our express written permission.

For EMEA, APAC & LATAM:

DWS is the brand name of DWS Group GmbH & Co. KGaA and its subsidiaries under which they do business. The DWS legal entities offering products or services are specified in the relevant documentation. DWS, through DWS Group GmbH & Co. KGaA, its affiliated companies and its officers and employees (collectively “DWS”) are communicating this document in good faith and on the following basis.

This document is for information/discussion purposes only and does not constitute an offer, recommendation, or solicitation to conclude a transaction and should not be treated as investment advice.

This document is intended to be a marketing communication, not a financial analysis. Accordingly, it may not comply with legal obligations requiring the impartiality of financial analysis or prohibiting trading prior to the publication of a financial analysis.

This document contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models, and hypothetical performance analysis. No representation or warranty is made by DWS as to the reasonableness or completeness of such forward looking statements. Past performance is no guarantee of future results.

The information contained in this document is obtained from sources believed to be reliable. DWS does not guarantee the accuracy, completeness, or fairness of such information. All third-party data is copyrighted by and proprietary to the provider. DWS has no obligation to update, modify or amend this document or to otherwise notify the recipient in the event that any matter stated herein, or any opinion, projection, forecast, or estimate set forth herein, changes or subsequently becomes inaccurate.

Investments are subject to various risks. Detailed information on risks is contained in the relevant offering documents.

No liability for any error or omission is accepted by DWS. Opinions and estimates may be changed without notice and involve a number of assumptions which may not prove valid.

DWS does not give taxation or legal advice.

This document may not be reproduced or circulated without DWS’s written authority.

This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction, including the United States, where such distribution, publication, availability, or use would be contrary to law or regulation or which would subject DWS to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

© 2022 DWS International GmbH

Issued in the UK by DWS Investments UK Limited which is authorised and regulated by the Financial Conduct Authority (Reference number 429806).

© 2022 DWS Investments UK Limited

In Hong Kong, this document is issued by DWS Investments Hong Kong Limited and the content of this document has not been reviewed by the Securities and Futures Commission.

© 2022 DWS Investments Hong Kong Limited

In Singapore, this document is issued by DWS Investments Singapore Limited and the content of this document has not been reviewed by the Monetary Authority of Singapore.

© 2022 DWS Investments Singapore Limited

In Australia, this document is issued by DWS Investments Australia Limited (ABN: 52 074 599 401) (AFSL 499640) and the content of this document has not been reviewed by the Australian Securities Investment Commission.

© 2022 DWS Investments Australia Limited

For investors in Bermuda: This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda. Additionally, non-Bermudian persons (including companies) may not carry on or engage in any trade or business in Bermuda unless such persons are permitted to do so under applicable Bermuda legislation.

For investors in Taiwan: This document is distributed to professional investors only and not others. Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed, and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction, or transmission of the contents, irrespective of the form, is not permitted.

© 2022 DWS Group GmbH & Co. KGaA. All rights reserved. (5/22) 090088_1

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in