DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

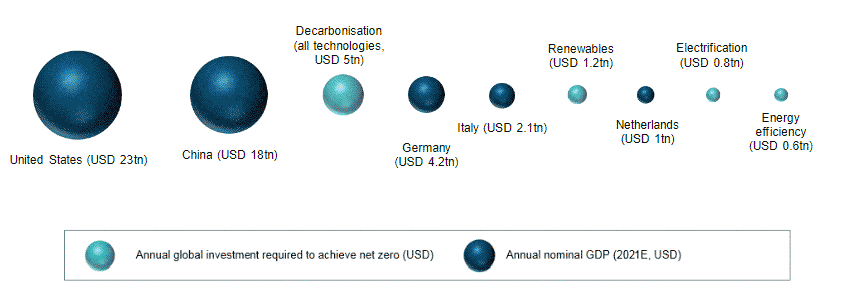

Economic Transition: As the global economy recovers, the effects of the pandemic continue to weigh on the outlook amid supply-demand bottlenecks, with the risk of new Covid variants jeopardising growth. Fiscal and monetary policy have played a central role in supporting the recovery but may have also increased vulnerabilities, with higher debt and asset prices contributing to an uncertain outlook for inflation, interest rates and return expectations in the medium term. Despite the risk of a more volatile and divergent economic environment, Covid-19 is acting as a catalyst for a deep social and economic transition converging on decarbonisation, technological change, and sustainable growth. With infrastructure at the centre of this transformation, these three trends are anticipated to provide investors with more opportunities for alpha generation. Decarbonisation Accelerating: Decarbonisation has become the world’s third largest economy, behind the U.S and China, with annual investments in excess of USD 5 trillion or 4.5% of world GDP by 2030.1 At the COP26 Climate Change Conference in November 2021, several governments announced ambitious initiatives to reach net zero emissions, but these pledges would limit global warming to 1.8°C, a level still above the Paris Agreement target of 1.5°C.2 Therefore, in the medium term we anticipate policy commitment to grow, contributing to an even wider infrastructure investment gap.

Source: DWS, IEA “Net Zero by 2050”, IRENA “World Energy Transitions Outlook: 1.5° C Pathway”, as at October 2021. Notes: F = forecast, E = expected. There is no guarantee the forecast shown will materialise. Forecasts are based on assumptions, estimates, views and hypothetical models or analyses, which might prove inaccurate or incorrect.

Climate financing is increasingly at the top of the policy agenda across mature and emerging economies. Governments are allocating a substantial share of their recovery packages to climate change mitigation policies to decarbonise energy and transportation. However, with public debt reaching new highs across both advanced and new economies, private capital is expected to contribute materially to decarbonisation. Therefore, although we anticipate increased flow of public investment in traditional infrastructure sectors supported by Covid-19 recovery packages, we also expect an increase in the use of Public-Private-Partnerships (PPPs).

In the United States, the Infrastructure Investment and Jobs Act is expected to deliver USD 550 billion of new investments into infrastructure projects over the next five years.3 The E.U. is expected to dedicate at least 37% of the EUR 750 billion recovery fund to green investments.4 Moreover, the E.U. is progressing with a roadmap to introduce an extensive package of new directives and regulations labelled EU ‘Fit for 55’, anticipated to drive a further acceleration of decarbonisation in Europe.

The E.U. reform proposal includes an expansion of the existing EU Emission Trading Scheme (ETS). The proposal aims to accelerate decarbonisation objectives, extend the scope of the EU ETS to include the shipping sector gradually from 2023, and to gradually phase out free allocations for the aviation sector by 2026. The EU Commission also plans to regulate road transport and building emissions through a new, separate trading system anticipated to come into force by 2026.5 Over the past decade, the EU ETS has contributed to a partial coal-to-gas switch for power generation. The recent reform proposals have contributed to expectations around a material acceleration of energy transition policies and higher power prices in Europe, with carbon emission pricing exceeding EUR 79/tonne in December 2021 (from EUR 32/tonne in January 2021),6 and long-term renewables power purchase agreements (PPAs) exceeding EUR 60/MWh (from EUR 38/MWh in December 2020), as investors focus on hedging against the risk of power prices increasing further.7

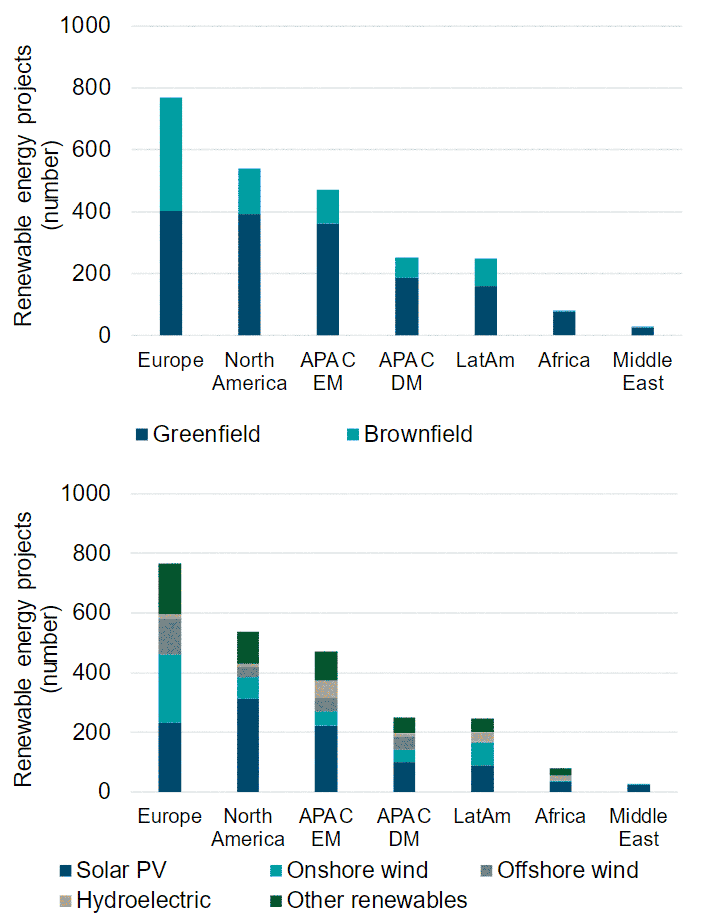

The last decade was marked by an initial shift from thermal power generation to renewables. We anticipate the pipeline for large-scale renewables to expand, as renewable energy increasingly achieves grid parity amid higher power prices, with developed markets continuing to lead in terms of investment volumes, supported by a comparatively mature regulatory framework. However, we expect distributed generation and small-scale renewables to form an essential part of the pipeline over the coming decade. Regulation supports small-scale renewables through a range of measures, such as feed-in-tariffs, tax reliefs and grants that vary by country. This supports the installation of rooftop solar and energy efficiency technologies including smart meters, battery storage, efficient boilers, and the electrification of heating and cooling systems.3

Source: Inframation, as at November 2021. For illustrative purpose only. Past performance is not a guide for future results.

Technological Innovation: Ambitious decarbonisation policies, stronger public investment and robust renewables growth will not be sufficient: achieving net-zero emissions may require more significant transformational changes and larger investments in sectors spanning from transportation to industry, with the adoption of innovative technologies and private capital playing a pivotal role. Covid-19 appears to have accelerated the adoption of digitalisation and innovative technologies. Technology is contributing to a reshuffling of the structure of our economies and changing the way consumers and industries operate. Importantly, technology is contributing to the emergence of sustainable, low emission solutions expected to play a pivotal role in achieving net zero, with digital infrastructure, battery storage, transport electrification, new mobility services, green hydrogen solutions, smart cities, logistics automation and decentralised water services at the centre of the development of a new economic platform and innovative business models. As new business models emerge, the competitive environment is changing, with transportation companies, utilities, Oil & Gas companies, new entrants and even telecom companies aiming to capture a share of this rapidly evolving market.

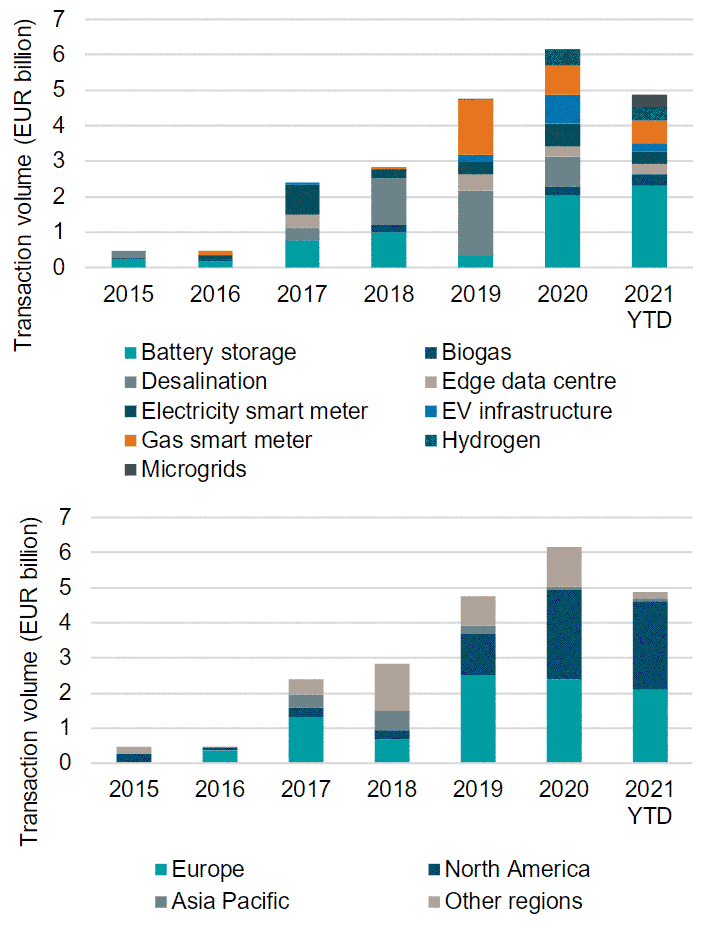

In our view, private infrastructure investors will play a central role in providing the capital needed to support the transition to a greener and more innovative infrastructure platform, with transaction volumes in emerging infrastructure sectors already showing signs of growth. As emerging technologies and business models gradually mature further, we anticipate growing interest from private infrastructure investors in emerging infrastructure sectors, a broadening of the investment pipeline, and more strategies focusing on the small and lower-middle end of the infrastructure market, where the pipeline for these opportunities is anticipated to be stronger. Emerging infrastructure sectors are likely to offer an opportunity for alpha generation, platform strategies and capital appreciation, but also will likely be exposed to higher volatility and an initial lack of historical return track-record. As a result, we anticipate investors will increasingly focus on portfolio construction and diversification.

Source: Infranews, as at November 2021. Past performance is not indicative of future results.

Beyond emerging investment opportunities, technological change will, in our view, also create a base for implementing value-enhancing asset management initiatives and for improving the sustainability profile of existing infrastructure assets. For example, public transportation may benefit from electrification of bus fleets to reduce emissions, sensors to improve asset efficiency, and digital connectivity solutions to integrate with smart city multi modal transport.

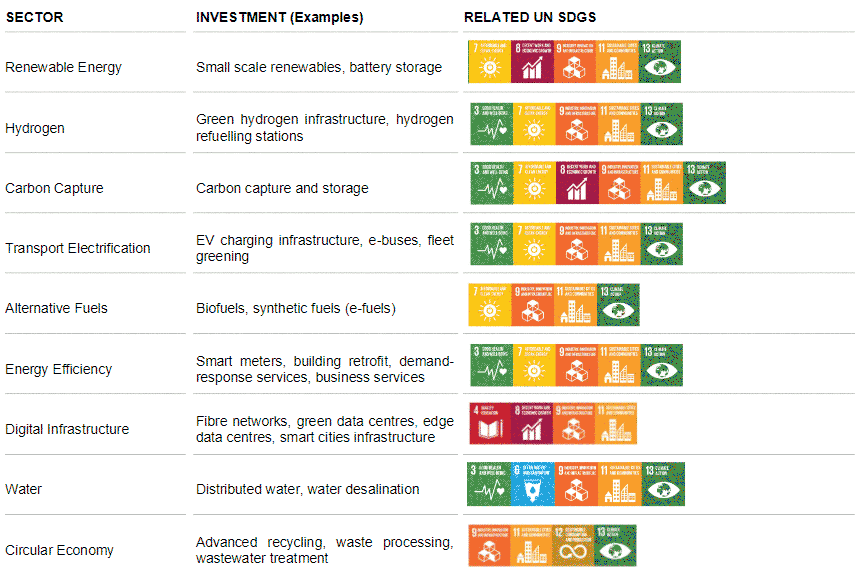

Sustainability and Infrastructure: Infrastructure plays a pivotal role in the achievement of a more sustainable global economy. The UN Sustainable Development Goals (SDGs), established by the UN General Assembly in 2015, introduced 17 global objectives that include climate action, but are more broadly focused on an inclusive improvement in quality of life around the world. Infrastructure, either directly or indirectly, influences the attainment of the Sustainable Development Goals (SDGs), including 72% of the targets.8 SDGs are increasingly contributing to orientating policymaking and private investors’ capital allocation decisions. Even though most efforts and capital flows have historically focused on investment in renewable energy, we now observe stronger policy making and private capital focus in supporting emerging infrastructure sectors that will play an essential role in supporting SDGs. For example, water security has been widely identified as one of the major global risks, with UN’s SDG 6 aiming to ensure access to safe water sources and SDG 14 focused on safeguarding ocean and marine resources sustainability. Over the next 30 years, an estimated USD 6.7 trillion may be required just to upgrade ageing water infrastructure across OECD markets and sanitation for all by 2030.9 With technological innovation in the form of new decentralised water supply and treatment systems offering innovative solutions for the provision of water and wastewater sanitation services, we anticipate strong focus from policymakers and private capital in supporting governance frameworks enabling the financeability of innovative water infrastructure projects.

Over the coming decade we anticipate the adoption of innovative infrastructure technologies to play an unparalleled role for the achievement of several key SDGs, requiring a considerable investment flow into supporting infrastructure such as small-scale renewables, battery storage, transport electrification, green hydrogen infrastructure, carbon capture, alternative fuels, energy efficiency services, or advanced recycling. In our view, these emerging infrastructure assets tend to be outside of the traditional remit of public investment; however, as these technologies mature further, and regulatory and contractual frameworks standardise, we anticipate private infrastructure capital to play a pivotal role in providing investment needed to contribute to the achievement of key SDGs.

Source: DWS, as at December 2021. This information is intended for informational purposes only and does not constitute investment advice, recommendation, an offer or solicitation. Forecasts are based on assumptions, estimates, views and hypothetical models or analyses, which might prove inaccurate or incorrect.

1 IEA, “Net Zero by 2050”, May 2021.

2 Bloomberg, “Top Energy Agency Says COP26 Pledges Signal 1.8°C of Warming”, 4 November 2021.

3 Reuters, “Biden signs $1 trillion infrastructure bill into law”, 16 November 2021

4 Reuters, “Germany to spend 90% of EU recovery money on green, digital goals”, 27 April 2021.

5 European Commission, “European Green Deal: Commission proposes transformation of EU economy and society to meet climate ambitions”, 14 July 2021.

6 ICE, December 2021.

7 Pexapark Euro Composite, 29 November 2021.

8 University of Oxford, “Infrastructure needed to achieve 72% of Sustainable Development Goal targets”, 2 April 2019, citing Nature Sustainability, “Infrastructure for sustainable development” (2019).

9 ECD, “Principles of Water Governance”, June 2015.

This information is subject to change at any time, based upon economic, market and other considerations and should not be construed as a recommendation. Past performance is not indicative of future returns. Forecasts are not a reliable indicator of future performance. Forecasts are based on assumptions, estimates, opinions and hypothetical models that may prove to be incorrect. Investments come with risk. The value of an investment can fall as well as rise and your capital may be at risk. You might not get back the amount originally invested at any point in time. Source: DWS Investment GmbH

The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries, such as DWS Distributors, Inc., which offers investment products, or DWS Investment Management Americas, Inc. and RREEF America L.L.C., which offer advisory services. There may be references in this document which do not yet reflect the DWS Brand. Please note certain information in this presentation constitutes forward-looking statements. Due to various risks, uncertainties and assumptions made in our analysis, actual events or results or the actual performance of the markets covered by this presentation report may differ materially from those described. The information herein reflects our current views only, is subject to change, and is not intended to be promissory or relied upon by the reader. There can be no certainty that events will turn out as we have opined herein.

Marketing Material. In EMEA for Professional Clients (MiFID Directive 2014/65/EU Annex II) only; no distribution to private/retail customers. In Switzerland for Qualified Investors (art. 10 Para. 3 of the Swiss Federal Collective Investment Schemes Act (CISA)). In APAC for institutional investors only. Australia and New Zealand: For Wholesale Investors only. In the Americas for Institutional Client and Registered Rep use only, not for public viewing or distribution. Israel: For Qualified Clients (Israeli Regulation of Investment Advice, Investment Marketing and Portfolio Management Law 5755-1995). *For investors in Bermuda: This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda.

IMPORTANT INFORMATION

For North America: The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries, such as DWS Distributors, Inc., which offers investment products, or DWS Investment Management Americas, Inc. and RREEF America L.L.C., which offer advisory services. This material was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. It is intended for informational purposes only. It does not constitute investment advice, a recommendation, an offer, solicitation, the basis for any contract to purchase or sell any security or other instrument, or for DWS or its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein. Neither DWS nor any of its affiliates gives any warranty as to the accuracy, reliability or completeness of information which is contained in this document. Except insofar as liability under any statute cannot be excluded, no member of the DWS, the Issuer or any office, employee or associate of them accepts any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage whether direct, indirect, consequential or otherwise suffered by the recipient of this document or any other person. The views expressed in this document constitute DWS Group’s judgment at the time of issue and are subject to change. This document is only for professional investors. This document was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. No further distribution is allowed without prior written consent of the Issuer. Investments are subject to risk, including market fluctuations, regulatory change, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you might not get back the amount originally invested at any point in time. An investment in real assets involves a high degree of risk, including possible loss of principal amount invested, and is suitable only for sophisticated investors who can bear such losses. The value of shares/ units and their derived income may fall or rise. War, terrorism, economic uncertainty, trade disputes, public health crises (including the recent pandemic spread of the novel coronavirus) and related geopolitical events could lead to increased market volatility, disruption to U.S. and world economies and markets and may have significant adverse effects on the global real estate markets. For Investors in Canada. No securities commission or similar authority in Canada has reviewed or in any way passed upon this document or the merits of the securities described herein and any representation to the contrary is an offence. This document is intended for discussion purposes only and does not create any legally binding obligations on the part of DWS Group. Without limitation, this document does not constitute an offer, an invitation to offer or a recommendation to enter into any transaction. When making an investment decision, you should rely solely on the final documentation relating to the transaction you are considering, and not the [document – may need to identify] contained herein. DWS Group is not acting as your financial adviser or in any other fiduciary capacity with respect to any transaction presented to you. Any transaction(s) or products(s) mentioned herein may not be appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understand such transaction(s) and have made an independent assessment of the appropriateness of the transaction(s) in the light of your own objectives and circumstances, including the possible risks and benefits of entering into such transaction. You should also consider seeking advice from your own advisers in making this assessment. If you decide to enter into a transaction with DWS Group, you do so in reliance on your own judgment. The information contained in this document is based on material we believe to be reliable; however, we do not represent that it is accurate, current, complete, or error free. Assumptions, estimates, and opinions contained in this document constitute our judgment as of the date of the document and are subject to change without notice. Any projections are based on a number of assumptions as to market conditions and there can be no guarantee that any projected results will be achieved. Past performance is not a guarantee of future results. The distribution of this document and availability of these products and services in certain jurisdictions may be restricted by law. You may not distribute this document, in whole or in part, without our express written permission.

For EMEA, APAC & LATAM: DWS is the brand name of DWS Group GmbH & Co. KGaA and its subsidiaries under which they do business. The DWS legal entities offering products or services are specified in the relevant documentation. DWS, through DWS Group GmbH & Co. KGaA, its affiliated companies and its officers and employees (collectively “DWS”) are communicating this document in good faith and on the following basis. This document is for information/discussion purposes only and does not constitute an offer, recommendation, or solicitation to conclude a transaction and should not be treated as investment advice. This document is intended to be a marketing communication, not a financial analysis. Accordingly, it may not comply with legal obligations requiring the impartiality of financial analysis or prohibiting trading prior to the publication of a financial analysis. This document contains forward looking statements. Forward looking statements include, but are not limited to assumptions, estimates, projections, opinions, models, and hypothetical performance analysis. No representation or warranty is made by DWS as to the reasonableness or completeness of such forward looking statements. Past performance is no guarantee of future results. The information contained in this document is obtained from sources believed to be reliable. DWS does not guarantee the accuracy, completeness, or fairness of such information. All third-party data is copyrighted by and proprietary to the provider. DWS has no obligation to update, modify or amend this document or to otherwise notify the recipient in the event that any matter stated herein, or any opinion, projection, forecast, or estimate set forth herein, changes or subsequently becomes inaccurate. Investments are subject to various risks. Detailed information on risks is contained in the relevant offering documents. No liability for any error or omission is accepted by DWS. Opinions and estimates may be changed without notice and involve a number of assumptions which may not prove valid. DWS does not give taxation or legal advice. This document may not be reproduced or circulated without DWS’s written authority. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction, including the United States, where such distribution, publication, availability, or use would be contrary to law or regulation or which would subject DWS to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions. © 2022 DWS International GmbH Issued in the UK by DWS Investments UK Limited which is authorised and regulated by the Financial Conduct Authority (Reference number 429806). © 2022 DWS Investments UK Limited In Hong Kong, this document is issued by DWS Investments Hong Kong Limited and the content of this document has not been reviewed by the Securities and Futures Commission. © 2022 DWS Investments Hong Kong Limited In Singapore, this document is issued by DWS Investments Singapore Limited and the content of this document has not been reviewed by the Monetary Authority of Singapore. © 2022 DWS Investments Singapore Limited In Australia, this document is issued by DWS Investments Australia Limited (ABN: 52 074 599 401) (AFSL 499640) and the content of this document has not been reviewed by the Australian Securities Investment Commission. © 2022 DWS Investments Australia Limited For investors in Bermuda: This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda. Additionally, non-Bermudian persons (including companies) may not carry on or engage in any trade or business in Bermuda unless such persons are permitted to do so under applicable Bermuda legislation. For investors in Taiwan: This document is distributed to professional investors only and not others. Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed, and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction, or transmission of the contents, irrespective of the form, is not permitted.

© 2022 DWS Group GmbH & Co. KGaA. All rights reserved. (12/21) 083979_2

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in