DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

The meteoric rise in oil prices over the past few months reflects tighter physical market fundamentals as the post covid recovery in crude demand kept surprising to the upside, OPEC+ producing fewer barrels vs expectations and OECD crude stocks declining. The surge in oil prices also reflects fears about the potential spare production capacity in a rapidly worsening geopolitical environment amidst a higher possibility of output disruptions. The removal of Russian oil and gas volumes from the market is likely to send energy prices soaring, exacerbate already-high inflation, and slow economic growth globally, a move that would be detrimental to many nations outside of Russia. Volatility in oil prices has also been exceptional because the underlying demand and supply curves are inelastic. Demand is inelastic due to long lead times for right-sizing the levels of fuel-consuming inventory. Supply is inelastic in the short term because it takes some time to alter the production coming out of oil wells.

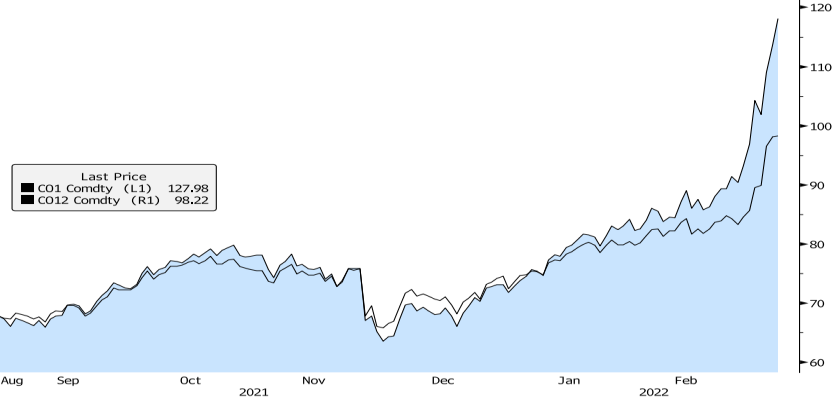

Source: Bloomberg, March 2022

According to EIA’s latest estimates, the Brent price will average $117/b in March, $116/b in 2Q22, and $102/b in 2H22. Finally, settling down around ~$89/b in 2023. However, these estimates remain highly uncertain in the short term. Actual price outcomes will be dependent on the degree to which existing sanctions imposed on Russia, any potential future sanctions, and independent corporate actions affect Russia’s oil production or the sale of Russia’s oil in the global market. In addition, the degree to which other oil producers respond to current oil prices, as well as other macro developments. Investors can see from the chart above that the oil market is currently in steep backwardation, where there is a premium for physical delivery of oil “now”. Oil futures are signaling a very tight physical market and there is a 12-month backwardation of around $30/b. Given the numerous market forces at play, the ultimate landing spot for prices is extremely difficult to determine.

Source: Bloomberg, March 2022

Russian oil embargo Crude oil recently touched $130/b (intraday), as the U.S. announced a Russian oil embargo. The U.S. imports less than 3% of crude oil from Russia and less than 8% when including all petroleum products. Russian production accounts for 10% of the world’s oil (10 mmbd) and it is the 2nd largest exporter behind Saudi Arabia at 7-7.5 mmbd. Russia supplies around 4.5 mmbd (30%) of European demand and 1.7 mmbd (12%) of Chinese demand. Europe also relies on Russian natural gas for 30-40% of supply depending on the country. The key exportable oil grade is Urals blend, a medium sour crude. Further oil disruption risks:

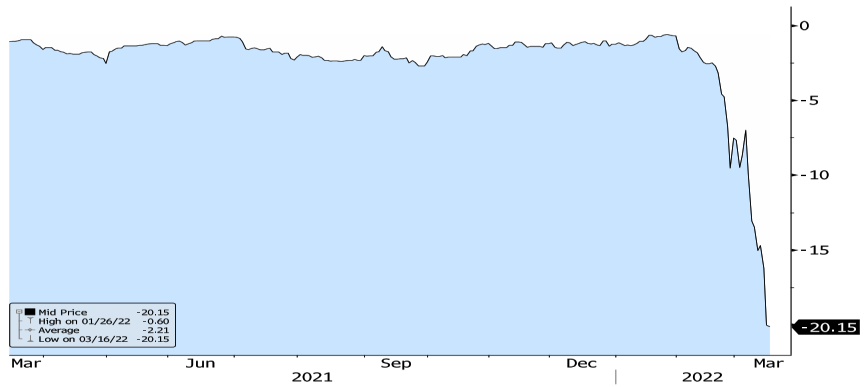

As some exports of Russian crude oil are being avoided, it is driving massive discounts ~$20/b for Urals vs. Brent and some unsold exports could struggle to find buyers.

Source: Bloomberg, March 2022

Fundamentals

Demand – According to EIA’s latest forecasts, global consumption of petroleum and liquid fuels will average 100.6 mmbd for all of 2022, up 3.1 mmbd from 2021. It forecasts that consumption will increase by 1.9 mmbd in 2023 to average 102.6 mmbd.

Supply – While global oil supply rose to 98.7 mmbd in January according to the IEA, the uptrend was slowed by a consistent OPEC+ under-performance vs targets. Some of the supply shortfall risks, could be reduced if producers in the Middle East with spare capacity were to compensate for those running out. A further 1.3 mmbd of Iranian crude supply could gradually be brought to market should sanctions be lifted.

According to EIA, recent crude oil price increases will push the U.S. average gasoline price to $4.10/gal on average in 2Q22, which would be the first time that gasoline prices have reached at least $4/gal since July 2008. Gasoline and diesel prices are closely tied to crude oil prices. The agency forecasts gasoline prices will average $3.71/gal in 2H22 – with a big caveat – should things normalize. As such, risk remains to the upside where there could be higher costs for refiners (passed on to consumers), due to sourcing and shipping potential offsets to Russian crude.

Policy

Domestic production – we are yet to see anything meaningful or comprehensive from the Biden administration regarding increasing domestic energy production. E&P companies are hesitant to “stick their necks out” and start bringing sizeable production online without getting any assurances or guarantees in return from the government, since investing in “future capex” based on today’s bubble-like prices can be a “recipe for disaster” down the road. Thus, any further investment has to be based on much lower $/b.

Source: EIA, March 2022

Source: EIA, March 2022

Windfall tax – Sen. Elizabeth Warren said she was working with Senate Democrats on a new tax proposal. The bill would target windfall profits, sudden and unusually large profits for oil companies, in light of the Russian invasion. “Energy security” vs ESG – will be a major topic of debate across several nations, where “energy security” is likely to be prioritized over “climate change initiatives”, at-least in the short-term. With the EU considering issuing a sizeable bond to finance energy and defense spending, it is vital to realize the likely “stickiness” of some of these policy shifts.

Potential demand destruction remains in focus, as longer-term elevated commodities prices have an adverse demand impact, although it is too early to gauge demand elasticity at this point in the economic recovery.

Also, this crisis is likely to involve energy, metals and food and will be more severely felt in Europe vs. the U.S. While several countries are rapidly decoupling from Russian financial markets, it will take longer to decouple from Russia in physical markets. Commodity supply will likely remain restricted until the conflict is resolved/sanctions ease or until some flows are redirected into Asia.

We could also see increased self-sanctioning along the oil supply chain. Fears over further sanctions and ambiguity over banking sanctions has resulted in some market participants avoiding Russian crude, reflected in the widening differentials, Urals vs. Brent, rising insurance and shipping costs.

| Bear case |

|---|

| Full disruption of Russian crude exports 5 mmbd by (U.S & Europe) countries backing the sanctions and/or weaponization of energy by Russia |

| Oil price – $150-$200/b |

| Base case |

| Partial disruption of Russian Crude and some flows re-directed into Asian markets |

| Oil price – $100-$150/b |

| Bull case |

| Cease fire and/or partial disruption of Russian crude offset by a combination of supply response from Gulf States/Iran/Venezuela/U.S. |

| Oil price – $70-$100/b |

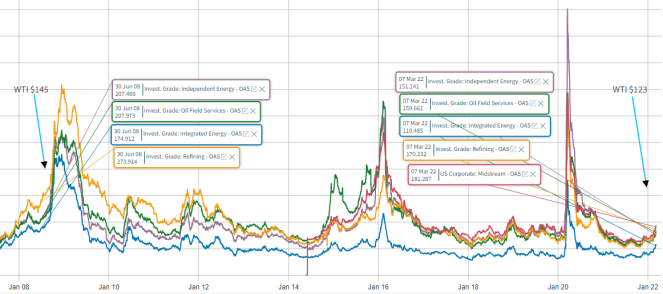

Using historical context, over the last 30 years, there have been only two instances where WTI prices breached $120/b: 1) Leading up to the 2008 financial crisis, where crude prices crashed from $145/b to $37/b in less than 6 months, and 2) the current geopolitical crisis. It is extremely hard to say how this episode will end, but in DWS’s view this volatility will drag on for a while and will likely get worse before it gets better.

Source: Barclays Chart, March 2022

Energy sector impact Commodity price tailwinds – While E&P companies will continue to benefit the most from higher oil prices and the majority having shed their hedge books leaving full upside, the current price environment provides tailwinds for the entire energy sector. This should further strengthen companies’ operating metrics and generate peak financial performance.

Refiners – Loss of Russian feedstocks will have a limited impact. The U.S. ban on Russian oil will require them to find alternative sources of crude and we expect that refinery utilization rates will remain largely intact. U.S. refiners should eventually benefit from increased export opportunities if Russia’s oil and refined products exports continue to decline or even cease.

Impairments are likely for oil majors exiting Russia – Exxon, BP and Shell all announced that they will be exiting their assets in Russia following the invasion of Ukraine. These exits will lead to sizeable impairments in most instances given the uncertainty regarding the potential to recover any value from these assets. Nevertheless, these companies have very strong balance sheets and continued high oil prices should mitigate credit-negative effects.

Potential rating upgrades – In DWS’s conversation with the agencies, we got the sense that any sector-wide upgrades are unlikely to materialize and will only happen on a case-by-case basis. As such, even though agencies anticipate that higher oil & gas price assumptions will lead to improved near-term leverage metrics at all rating levels, they remain focused on companies’ financial policies and commitment to improving balance sheets through debt reduction; as such DWS does not expect any wholesale upgrades to the sector.

Sid Bhartiya

Senior Research Analyst-Fixed Income

Thomas Farina

Portfolio Manager and Head of U.S. Investment Grade Credit

For Institutional Investor use only. Past performance is not indicative of future returns.Forecasts are based on assumptions, estimates, opinions,, and hypothetical models that may prove to be incorrect. Investments come with risk. The value of an investment can fall as well as rise and your capital may be at risk. You might not get back the amount originally invested at any point in time.

Disclaimer

DWS is the brand name of DWS Group GmbH & Co. KGaA and its subsidiaries under which they do business. TheDWS legal entities offering products or services are specified in the relevant documentation. DWS, through DWSGroup GmbH & Co. KGaA, its affiliated companies and its officers and employees (collectively “DWS”) arecommunicating this document in good faith and on the following basis.

This document is for information/discussion purposes only and does not constitute an offer, recommendation orsolicitation to conclude a transaction and should not be treated as investment advice.

This document is intended to be a marketing communication, not a financial analysis. Accordingly, it may notcomply with legal obligations requiring the impartiality of financial analysis or prohibiting trading prior to thepublication of a financial analysis.

This document contains forward looking statements. Forward looking statements include, but are not limited toassumptions, estimates, projections, opinions, models and hypothetical performance analysis. No representation orwarranty is made by DWS as to the reasonableness or completeness of such forward looking statements. Pastperformance is no guarantee of future results.

The information contained in this document is obtained from sources believed to be reliable. DWS does notguarantee the accuracy, completeness or fairness of such information. All third-party data is copyrighted by andproprietary to the provider. DWS has no obligation to update, modify or amend this document or to otherwise notifythe recipient in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forthherein, changes or subsequently becomes inaccurate.

Investments are subject to various risks. Detailed information on risks is contained in the relevant offeringdocuments.

No liability for any error or omission is accepted by DWS. Opinions and estimates may be changed without noticeand involve a number of assumptions which may not prove valid.DWS does not give taxation or legal advice. This document may not be reproduced or circulated without DWS’s written authority. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen orresident of or located in any locality, state, country or other jurisdiction, including the United States, where suchdistribution, publication, availability or use would be contrary to law or regulation or which would subject DWS toany registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, suchrestrictions.

This document may not be reproduced or circulated without DWS written authority. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. War, terrorism, sanctions, economic uncertainty, trade disputes, public health crises and related geopolitical events have led, and, in the future, may lead to significant disruptions in US and world economies and markets, which may lead to increased market volatility and may have significant adverse effects on the fund and its investments.

This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisfsdiction, including the United States, where such distribution, publication, availability or use would be contrary to law or regulation or which would subject DWS to any registration or licensing requirement within such jurisdiction not currently met within such jurisdiction. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions.

© 2022 DWS International GmbH

Issued in the UK by DWS Investments UK Limited which is authorised and regulated in the UK by the FinancialConduct Authority.

© 2021 DWS Investments UK Limited

This document is issued by DWS Investments Hong Kong Limited (“DWS HK”) and is the property and copyright of DWS HK. This document may not be reproduced or circulated without DWS HK’s written consent. The mannerof circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. All rights reserved.

© 2022 DWS Investments Hong Kong Limited

In Singapore, this document has not been reviewed by any regulatory authority. This ddocument has been prepared solely for informatonal purposes and does not constitute an offer or arecommendation to enter into any transaction. The terms of any investment will be exclusively subject to thedetailed provisions, including risk considerations, contained in the offering documents. When making aninvestment decision, you should rely on the final documentation on relating to the transaction. The value of an investment and any income from it can go down as well as up. Past performance is not a reliable indicator offuture result

© 2022 DWS Investments Singapore Limited

In Australia, this document is issued by DWS Investments Australia Limited (ABN: 52 074 599 401) (AFSL 499640) and the content of this document has not been reviewed by the Australian Securities Investment Commission.

© 2022 DWS Investments Australia Limited

In Taiwan, this document is distributed to professional investors only and not others. Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or asolicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed, and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

For investors in Bermuda

This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda. Additionally, non-Bermudian persons (including companies) may not carry on or engage in any trade or business in Bermuda unless such persons are permitted to do so under applicable Bermuda legislation.

© 2022 DWS Group GmbH & Co. KGaA. All rights reserved. I-088802-1

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in