DWS

Bernard F. Ryan, CFA

Insurance Coverage

bernie.ryan@dws.com

617-295-2105

dws.com/InsuranceAM

875 Third Avenue

New York, NY 10022

The real estate debt asset class can provide debt investment options that may outperform traditional benchmarks while potentially offering attractive returns, downside protection, diversification benefits, and lower volatility.

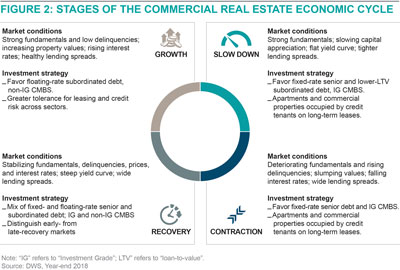

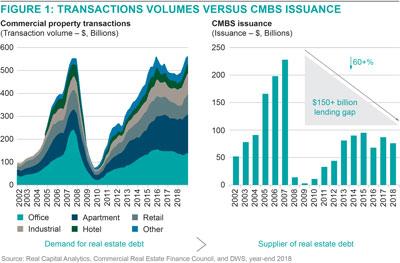

The debt secured by commercial real estate has been dominated historically by traditional lenders such as banks and institutional investors. However, banks have been forced to cut back on their leverage and boost their regulatory capital to comply with the regulatory reforms implemented in the wake of the financial crisis. Their demand for CMBS and CRE lending fell at a time of rising investment in the commercial real estate sector, causing a funding gap. (See Figure One.)

Since the financial crisis, annual CMBS issuance has remained less than half of 2006 and 2007. The current size of the commercial real estate debt market is about $4 trillion, with around $1 trillion of this maturing over the next several years, requiring refinancing or recapitalization (estimates from Board of Governors of Federal Reserve and Moody’s Analytics, as of year-end 2018).

The potential mismatch of supply and demand for debt as these maturities approach should allow nontraditional private debt lenders, like insurance companies and others, to increase their debt activity and seek attractive returns.

Firms with developed real estate platforms can therefore help craft specific strategies that meet the needs of these investors with loans to institutional-quality borrowers and properties.

As noted earlier, the share of commercial real estate debt from alternative lenders is now about 9%, which is up over 57% from 2013. The trade publication Commercial Mortgage Alert estimated in early June that there were nearly 160 firms and funds providing subordinate debt, private debt, preferred equity and other types of commercial real estate financing. However, despite their interest in CRE assets, many of these are not consistent market participants. They may be active when conditions are favorable, but withdraw when the environment becomes more challenging. Consistent success requires a firm that is active in commercial real estate debt in all phases of the cycle, with deep relationships and a good reputation in the market with borrowers, co lenders, brokers, banks and other participants. This allows certainty of execution and a consistent discipline in underwriting through all market cycles.

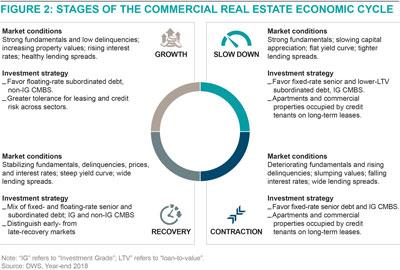

The commercial real estate debt market is currently in the classic late stage of its cycle, described in the upper right quadrant of Figure Two, but with some unique attributes. As shown below and described earlier, there are various opportunities within each stage of a cycle.

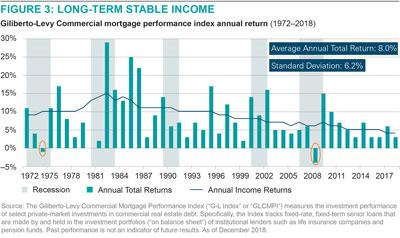

From a credit perspective, delinquencies continue to be low. We have not seen excessive loan-to-value creep or undisciplined underwriting standards, which is a very positive sign at this point in the cycle. We believe the cycle still has more time to run. Nonetheless, it has already been a very long cycle and DWS is taking a more defensive late-cycle approach in its commercial real estate lending. Even so, we believe there are still valuable opportunities. In fact, since 1974 there have only been two years, 1974 and 2008, where returns were negative. (See Figure Three.) That illustrates the long term stability of the asset class.

Investors often tend to think of the senior mortgage market when considering real estate debt. While that is the largest part of the market, and mostly dominated by banks and CMBS, the growing activity of non-bank investors has created more access points to get exposure in ways that might offer better returns.

Generally speaking, the real estate debt space consists of any fixed income or credit structure that is ultimately backed by real property. For example, if you owned a mid rise multi family property worth $100, someone might be willing to make you a senior loan on that property of up to $60 in order to earn a reasonably low return that nonetheless represents a slight premium to corporate bonds (as of the end of June 2019). Alternatively, if a lender understood the risk of that property, market and sponsor really well, and wanted to achieve a higher return, it could make a mezzanine subordinate to the $60 senior mortgage, which would receive a higher return for the incremental increase in exposure.

These subordinate positions require the same, and often even more, detailed analysis of the creditworthiness of the senior loan. The objective is to find the optimal structure and returns that make sense for investors with varying risk appetites.

Well-structured and underwritten commercial real estate deals offer a number of qualities. These include:

One of the key advantages is stable and current, predictable income. The vast majority of these investments are structured with current pay of contractual income. For investors that are matching liabilities, such as insurance companies and certain others, this is obviously important. Or, if you think that the appreciation in your core equity portfolio is going to be weaker as the cycle extends, shifting to higher income strategies such as CRE debt is an option.

Another benefit of the sector is principal preservation. These investments are collateralized by real assets that carry significant cushion to the lender’s exposure. In the earlier example, if you have a $60 loan in a property that’s worth $100, you stand to achieve the returns you originally expected, unless the value deteriorates by 40% or more. If the loan is supplemented by a 15% mezzanine loan, the total loan basis would be 75%; still exhibiting a 25% cushion in the form of the first loss position of borrower’s equity. Should the market experience a downturn at some point, the investor has insulation and the values can deteriorate somewhat before the investment is impaired. That is an advantage the owner of the property does not have, and a significant benefit to a real estate debt allocation.

A third noteworthy attribute is the ability of different investors to meet their specific risk appetites and sensitivities to duration. While one investor might want a real estate debt strategy that targets, for instance, a long term fixed rate investment grade portfolio that meets its risk appetite and balance sheet needs, another might seek a shorter term floating rate strategy with slightly higher spreads that matches its particular liabilities. A third investor shifting out of a strategy in core equity might be less sensitive to duration but still wants to outperform the NCREIF Property Index.

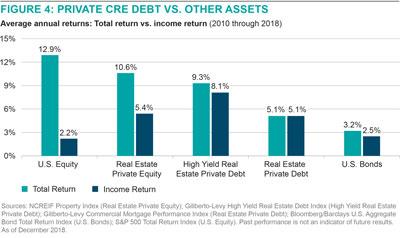

Figure Four represents the composition of returns for various asset classes. Looking at the two primary real estate debt areas, high yield has posted post recession returns of 9.3% represented by the Giliberto-Levy High Yield Real Estate Debt Index, of which almost 90% are comprised of income, while higher-grade mortgage debt is in the 5% range as represented by the Giliberto-Levy Commercial Mortgage Performance Index. Compare that to the NCREIF Property Index, which is the column to the left. The returns are about 130 basis points higher but the income component is only about half, so it enjoys less of the benefit of having a strong income aspect. The forecast for NCREIF is in the low fives for the next five years (total return), so while the performance has been excellent since the great recession, on a forward looking basis, those returns are expected to moderate.

Turning to the groups on the right of Figure Four, both high yield and the mortgage index have significantly outperformed the broader bond index (Bloomberg/Barclays U.S. Aggregate Bond Index). As a complement to fixed income portfolios, history suggests that CRE debt can provide outperformance.

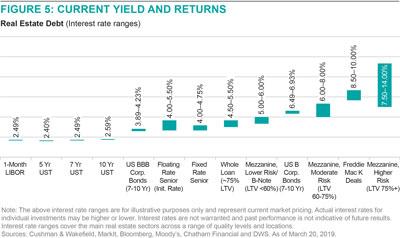

As you can see from the chart in Figure Five, senior fixed-rate mortgage loans of up to approximately 60% LTV have rates between 4% and 5%. Senior “stretch” loans, or whole loans, increase the LTV somewhat, providing rates above this level by 50 to 75 basis points. Lower risk subordinate debt, such as mezzanine loans and B Notes up to 60% LTV have rates in the 5% to 6% range. A moderate risk subordinate loan of 60% to 75% LTV increases the rate to approximately 6% to 8%, and higher risk subordinate debt (greater than 75% LTV) can have rates from 7.5% to the mid-teens depending on structure and property. It is important to note that in each of these loan types, the lender still benefits from the first loss equity position of the sponsor/borrower, providing protection and principal preservation benefits to the lender. Figure Five shows the return ranges for various benchmarks.

Given the point of the cycle, investors could look to utilize an approach which would involve a mix of private debt and public debt, such as CMBS or Freddie Mac K deals, to enhance liquidity. We feel that a combination of medium risk senior loans and low- to medium risk mezzanine loans secured by stable properties with experienced sponsors would create a highly-effective, late-cycle approach.

Also, being in this late stage of the cycle makes it sensible to focus on the most liquid markets. These do not necessarily have to be primary markets; they could be secondary or tertiary markets as long as there is a high level of understanding of that market and liquidity. This could include those with the best relative growth, including in population, rent and employment.

In terms of property types, DWS’s perspectives:

Commercial real estate debt offers a yield premium in many cases to certain other asset classes, with the benefits discussed herein. Given the movement of market participants, as well as the increased standards instituted over the past several years, private commercial real estate debt can be considered an “evergreen” allocation given the range of sub-sectors. With its range of opportunities, investors can look to the asset class for uncorrelated asset class exposure, differing levels of income generation, not to mention it being complementary to other real estate investments such as equity ownership.

By DWS Patrick Kennelly, Portfolio Manager, Real Estate Debt Joe Rado, Head of Asset Management, Real Estate Debt

Please note certain information in this presentation constitutes forward-looking statements. Due to various risks, uncertainties and assumptions made in our analysis, actual events or results or the actual performance of the markets covered by this presentation report may differ materially from those described. The information herein reflect our current views only, are subject to change, and are not intended to be promissory or relied upon by the reader. There can be no certainty that events will turn out as we have opined herein. Forecasts are not a reliable indicator of future returns. Forecasts are based on assumptions, estimates, views and hypothetical models or analyses, which might prove inaccurate or incorrect.

Exploring the various uses of private real estate debt in an insurance portfolio Note: Not all products and services are offered in all jurisdictions and availability is subject to local regulatory restrictions and requirements. Subject to applicable laws and internal policies and procedures.

There is no assurance that investment objectives will be achieved.

For institutional investor and registered representative use only. Not to be shared with the public.

The brand DWS represents DWS Group GmbH & Co. KGaA and any of its subsidiaries such as DWS Distributors, Inc. which offers investment products or DWS Investment Management Americas Inc. and RREEF America L.L.C. which offer advisory services.

The material was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. It is intended for informational purposes only and it is not intended that it be relied on to make any investment decision. It is for professional investors only. It does not constitute investment advice or a recommendation or an offer or solicitation and is not the basis for any contract to purchase or sell any security or other instrument, or for Deutsche Bank AG and its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein.

Please note that this information is not intended to provide tax or legal advice and should not be relied upon as such. DWS does not provide tax, legal or accounting advice. Please consult with your respective experts before making investment decisions.

Neither DWS nor any of its affiliates, gives any warranty as to the accuracy, reliability or completeness of information which is contained. Except insofar as liability under any statute cannot be excluded, no member of DWS, the Issuer or any officer, employee or associate of them accepts any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission or for any resulting loss or damage whether direct, indirect, consequential or otherwise suffered.

This document is intended for discussion purposes only and does not create any legally binding obligations on the part of DWS and/or its affiliates. Without limitation, this document does not constitute investment advice or a recommendation or an offer or solicitation and is not the basis for any contract to purchase or sell any security or other instrument, or for DWS to enter into or arrange any type of transaction as a consequence of any information contained herein. The information contained in this document is based on material we believe to be reliable; however, we do not represent that it is accurate, current, complete, or error free. Assumptions, estimates and opinions contained in this document constitute our judgment as of the date of the document and are subject to change without notice. Past performance is not a guarantee of future results. Any forecasts provided herein are based upon our opinion of the market as at this date and are subject to change, dependent on future changes in the market. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. Investments are subject to risks, including possible loss of principal amount invested.

Certain DWS products and services may not be available in every region or country for legal or other reasons, and information about these products or services is not directed to those investors residing or located in any such region or country. The material was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. It is intended for informational purposes only and it is not intended that it be relied on to make any investment decision. It is for professional investors only. It does not constitute investment advice or a recommendation or an offer or solicitation and is not the basis for any contract to purchase or sell any security or other instrument, or for DWS and its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein. Investment decisions should always be based on the Sales Prospectus, supplemented in each case by the most recent audited annual report and, in addition, by the most recent half-year report, if this report is more recent than the most recently available annual report. Past performance is not indicative of future results. No representation or warranty is made as to the efficacy of any particular strategy or the actual returns that may be achieved.

For investors in Bermuda: This is not an offering of securities or interests in any product. Such securities may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 of Bermuda which regulates the sale of securities in Bermuda. Additionally, non-Bermudian persons (including companies) may not carry on or engage in any trade or business in Bermuda unless such persons are permitted to do so under applicable Bermuda legislation.

© 2019 DWS GmbH & Co. KGaA. All rights reserved. I-069550-1

Unlock full access to our vast content library by registering as an institutional investor

RegisterUnlock full access to our vast content library by registering as an institutional investor .

Create an accountAlready have an account ? Sign in