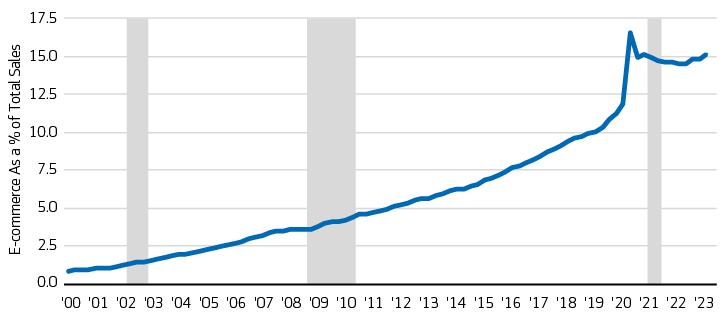

The retail sector has received a lot of attention in recent years given the Covid-19 pandemic, decline of the regional mall, wary shoppers, and subsequent government-mandated restrictions, leading some to doubt the need for physical retail establishments in the future. Predictably, e-commerce sales spiked in 2020, but as pandemic restrictions have receded, e-commerce as a percentage of total sales has stabilized in line with the prior trend (exhibit 1).

Exhibit 1: E-Commerce sales revert back to trend post pandemic

Shaded areas indicate US recessions. Source: US Census Bureau. May 19, 2023

The availability of retail space is near historic lows. There has been a significant decline in retail completions since the Great Financial Crisis as the sector was overbuilt coupled with the secular shift towards online shopping. In addition, the rise in construction costs has helped limit the threat of new supply across retail subtypes and geographies. As a result, we believe the retail sector is in a good position to weather a mild recession.

Despite the prominent news articles of retail tenants defaulting, the national retail vacancy rate was 4.2%, a 30-basis point decline over the past 12 months ending March 31, 2023.1 In addition, many power/neighborhood centers that tend to be the victims of these tenant bankruptcies are well-located in fundamentally strong markets, which limits the amount of downtime should space become available.

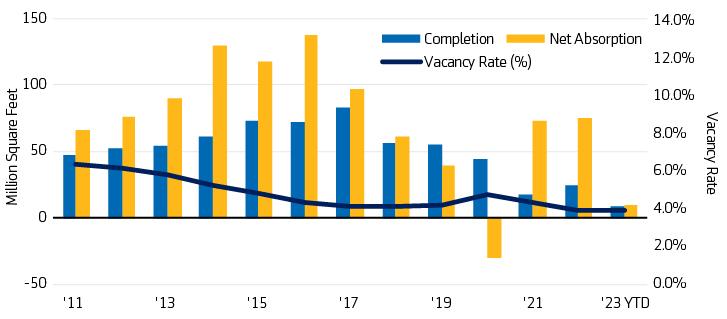

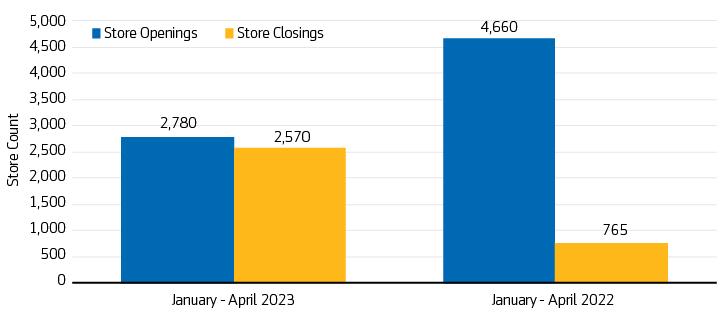

Nearly all major retail types, including fitness chains, cosmetic retailers and dollar-store chains, have experienced higher foot traffic when compared to 2019.2 Moreover, annual net absorption since 2011 has remained positive with the exception of 2020 (exhibit 2).1 Although store openings have slowed, during the first four months of 2023 there were more store openings than closings, specifically in the discounter segment, which has responded well during and after the pandemic (exhibit 3).

Exhibit 2: Minimal new supply has kept retail fundamentals largely balanced

Source: CoStar 1Q 2023 US Retail Report

Exhibit 3: Announced store openings still exceed closings

Source: Daily on Retail, May 2023

Finding lending opportunities

Grocery-anchored retail

One segment that has consistently demonstrated strength is grocery-anchored retail, in particular centers occupied by grocery stores with dominant market positions3 or smaller chains that fit a niche market and exhibit strong local market demand. In our underwriting, we prefer grocer tenants with a proven track record of sales growth and low occupancy costs. We believe these factors help to mitigate the risk associated with grocers prematurely exiting the market or at the end of their lease term.

For centers that contain junior anchor(s) and other in-line tenants, it is important to be mindful of co-tenancy clauses4 and to minimize in-line tenant space. Our preference is for centers located in well-established markets, supported by robust population counts that extend the trade area several miles and have median incomes within 1-, 3-, and 5-mile radii exceeding the national average. Additionally, we favor high-traffic areas with convenient access to major roads, ensuring optimal exposure and convenience for consumers.

Needs-based strip & unanchored retail

We believe there are promising prospects within the needs-based strip and unanchored retail segment. Properties in this segment typically include centers with a strong occupancy history, staggered lease expiration schedules, and a tenant mix that includes e-commerce resistant businesses. However, a heightened level of selectivity and careful evaluation throughout the underwriting process is warranted. We place a strong emphasis on in-fill locations within larger, densely populated markets that already have well-established customer bases. In addition, high land values also serve as a reinforcing factor, further solidifying viability of properties.

Recent examples

During the fourth quarter of 2022, Aegon AM Real Assets originated a loan secured by a grocery-anchored center situated in the Washington DC metropolitan statistical area (MSA). This center consists of a diverse mix of tenants, including a neighborhood grocery anchor, junior anchors, and in-line tenants. The anchor tenant's lease rollover is set for 2029, with multiple renewal options available and the loan is structured to reflect this upcoming event. The transaction featured a loan-to-value (LTV) ratio of less than 55% and a debt service coverage ratio (DSCR) of over 2.5x. The loan is set to mature in 2030 with a 30-year amortization schedule.

In the second quarter of 2023, we originated a loan secured by an unanchored retail center located within the Baltimore MSA. This center comprises several reputable junior anchors and in-line spaces, and benefits from staggered lease expirations. The property exhibits a high land-to-loan value ratio and a track record of long-term tenant occupancy. The transaction included an LTV ratio below 40% and a DSCR of over 3x. The loan is set to mature in 2030 with a 30-year amortization schedule, accompanied by a 36-month period of interest-only payments.

While price discovery is still an ongoing issue as retail transaction activity remains subdued, this is the case across all major commercial real estate sectors. By closely analyzing these types of retail properties, we feel there will continue to be opportunities to underwrite resilient investments in a rapidly evolving market.

1CoStar Realty Information, Inc. March 31, 2023

2Placer.AI. January 2023

3National and regional chains ranking among the top three in their respective markets.

4A co-tenancy clause allows a tenant to reduce their respective rent or potentially terminate their lease if a key tenant(s) (i.e., grocer, large anchor retailers) or a certain number of tenants leave the overall center, as specified in a lease.

Download the Insight Here

Disclosures

Unless otherwise noted, the information in this document has been derived from sources believed to be accurate at the time of publication.

This material is provided by Aegon Asset Management (Aegon AM) as general information and is intended exclusively for institutional, qualified, and wholesale investors, as well as professional clients (as defined by local laws and regulation) and other Aegon AM stakeholders.

This document is for informational purposes only in connection with the marketing and advertising of products and services, and is not investment research, advice or a recommendation. It shall not constitute an offer to sell or the solicitation to buy any investment nor shall any offer of products or services be made to any person in any jurisdiction where unlawful or unauthorized. Any opinions, estimates, or forecasts expressed are the current views of the author(s) at the time of publication and are subject to change without notice. The research taken into account in this document may or may not have been used for or be consistent with all Aegon AM investment strategies. References to securities, asset classes and financial markets are included for illustrative purposes only and should not be relied upon to assist or inform the making of any investment decisions. It has not been prepared in accordance with any legal requirements designed to promote the independence of investment research, and may have been acted upon by Aegon AM and Aegon AM staff for their own purposes.

The information contained in this material does not take into account any investor's investment objectives, particular needs, or financial situation. It should not be considered a comprehensive statement on any matter and should not be relied upon as such. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to any particular investor. Reliance upon information in this material is at the sole discretion of the recipient. Investors should consult their investment professional prior to making an investment decision. Aegon AM is under no obligation, expressed or implied, to update the information contained herein. Neither Aegon AM nor any of its affiliated entities are undertaking to provide impartial investment advice or give advice in a fiduciary capacity for purposes of any applicable US federal or state law or regulation. By receiving this communication, you agree with the intended purpose described above.

Past performance is not a guide to future performance. All investments contain risk and may lose value. Examples of loan originations are for illustrative purposes only. The business of investing in real estate is speculative and subject to numerous risks. No assurance can be made that Aegon RA would be able to obtain similar terms in the future or that positive outcomes have been or will be obtained. This document contains "forward-looking statements" which are based on Aegon AM's beliefs, as well as on a number of assumptions concerning future events, based on information currently available. These statements involve certain risks, uncertainties and assumptions which are difficult to predict. Consequently, such statements cannot be guarantees of future performance, and actual outcomes and returns may differ materially from statements set forth herein.

The following Aegon affiliates are collectively referred to herein as Aegon Asset Management: Aegon USA Investment Management, LLC (Aegon AM US), Aegon USA Realty Advisors, LLC (Aegon RA), Aegon Asset Management UK plc (Aegon AM UK), and Aegon Investment Management B.V. (Aegon AM NL). Each of these Aegon Asset Management entities is a wholly owned subsidiary of Aegon N.V. In addition, Aegon Private Fund Management (Shanghai) Co., Ltd, a partially owned affiliate may also conduct certain business activities under the Aegon Asset Management brand.

Aegon AM UK is authorised and regulated by the Financial Conduct Authority (FRN: 144267) and is additionally a registered investment adviser with the United States (US) Securities and Exchange Commission (SEC). Aegon AM US and Aegon RA are both US SEC registered investment advisers. Aegon AM NL is registered with the Netherlands Authority for the Financial Markets as a licensed fund management company and on the basis of its fund management license is also authorized to provide individual portfolio management and advisory services in certain jurisdictions. Aegon AM NL has also entered into a participating affiliate arrangement with Aegon AM US. In China, Aegon Private Fund Management (Shanghai) Co., Ltd is regulated by the China Securities Regulatory Commission (CSRC) and the Asset Management Association of China (AMAC) for Qualified Investors only.

©2023 Aegon Asset Management. All rights reserved.

Adtrax: 5776342.1GBL