Executive Summary

- Fundamentals and valuations in Emerging Markets (EM) remain attractive relative to Developed Markets, with manageable risks to the downside

- For insurance companies, investing in EM debt can increase portfolio diversification and potentially generate attractive, capital-adjusted yields

- There are various strategies and structures available for insurance investors in EM debt, some of which provide local currency exposure without associated operational issues

- Insurance-specific considerations when evaluating the EM asset class and determining the appropriate strategy include appetite for risk and volatility, liquidity, currency exposure, and asset-liability management

Attractive Fundamentals and Valuations in EM

While the effects of the global pandemic have been dire for countries around the world, we believe that in a recovery, Emerging Markets (EM) have a favorable growth trajectory compared to Developed Markets (DM). Signs of recovery, including growth pickups in Latin America, expected policy loosening in China and a revival of tourism in many Caribbean countries, point toward a challenging but constructive outlook for EM. With the large amounts of liquidity being dispersed by governments, we continue to see activity picking up across regions despite economies lagging from the effects of the pandemic. In addition, not all countries are created equal, and many EM economies have larger buffers than asset prices indicate, which will benefit those assets as markets normalize. As vaccination rates increase globally, we are optimistic about the recovery as we enter 2022.

The current environment is unique and leaves investors both searching for yield and questioning the funding dynamics of governments and corporates globally. EM was hit hard along with other global fixed income assets in March 2020. Spreads were at the widest levels since the Global Financial Crisis but recovered as stimulus packages reduced liquidity fears. With global rates ending 2021 at low levels to encourage economic growth and liquidity, EM continue to recover. Corporates have remained resilient during the pandemic with balance sheets remaining intact. Commodities have provided an attractive macro backdrop for EM recently, with a strong recovery in oil prices along with others, such as iron ore and copper, hitting all-time highs.

Despite a strong recovery thus far in the asset class, we believe there are still attractive opportunities across EM at these valuations as some credits have been over penalized in this downturn and have lagged in the ascent. The key is to differentiate those sovereigns and corporates that have sufficient buffers to withstand near-term liquidity pressures on a gradual road to recovery. Recently, the spread differential between EM and DM widened as EM underperformed DM in the second half of 2021. Concerns about a China slowdown driven by the property sector weighed on EM as a whole. The widening differential leaves room for potential spread compression over the coming quarters, as we continue to see supportive policy measures even in the face of Federal Reserve tapering. Over the coming months, as we anticipate more clarity on both U.S. taper policy and China’s policy response, there should be an opportunity to capitalize on the spread differentials between EM and DM. Security selection and country rotation will be key for any EM investor, as not all opportunities are created equally, and the dispersion in returns could be significant.

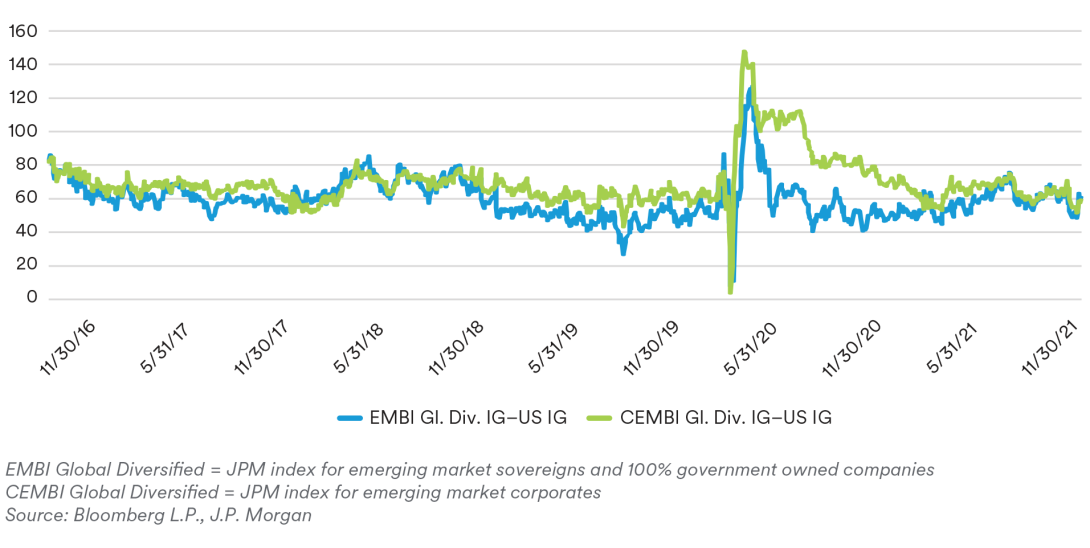

Spread Pickup of EM IG over DM IG

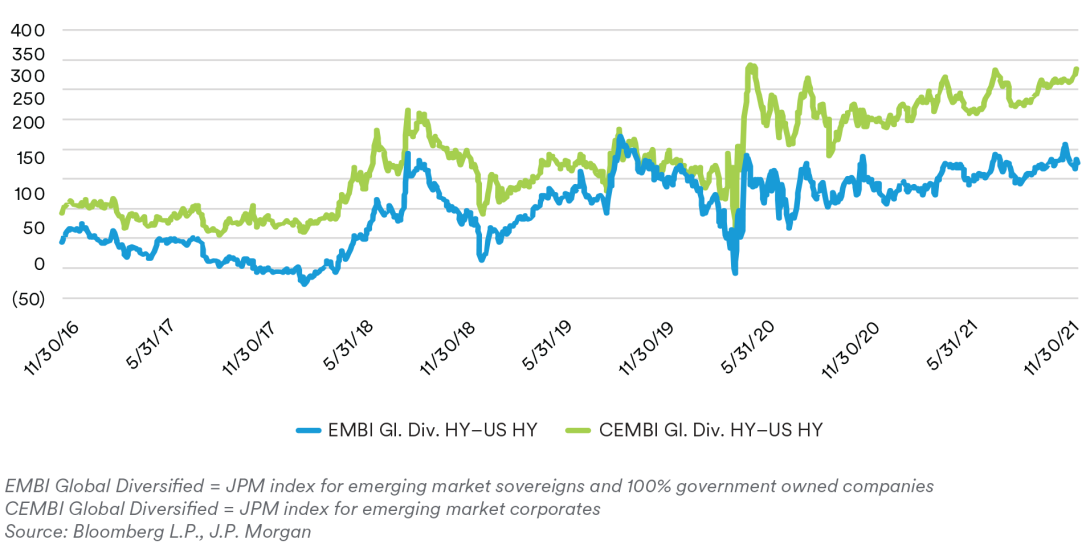

Spread Pickup of EM HY over DM HY

Manageable Risks to the Downside

We recognize that the asset class could be prone to exogenous shocks, such as geopolitical flareups or turbulence in commodities prices. Over the past decade, countries, like Peru and Indonesia, migrated from high yield to investment grade, while others, like Brazil and South Africa, have gone the other way. EM corporates have compared favorably, historically, to issuers in DM, and even in 2020, boasted lower default rates without massive sovereign support. We have seen the importance of investing in countries we believe can withstand the shocks, and where valuations look attractive to compensate for the risks. Hence, we look for improving stories, including countries that are focusing on implementing reforms (e.g., showing commitment to curb fiscal deficits, improving economic growth, etc.) and those that have sufficient liquidity reserves and resources to withstand the headwinds.

Various Strategies and Vehicles Available to Insurance Companies in EMD

Insurance company investors can access the EM debt (EMD) asset class through a variety of strategies and vehicles. Many insurance companies, particularly life insurers, have a high-quality, income-oriented bias that lends itself well to investing in an investment-grade-(IG)-focused, separately managed account (SMA). An IG SMA allows for the greatest flexibility, as an insurer can tailor its EM exposure based on the company’s objectives and preferences, including an assessment of appropriate, below-investment-grade holdings. Additionally, for insurers that have higher risk tolerance or for surplus accounts, there are higher-yielding EM strategies available in the market that could provide investors with a complementary and broader exposure to the EM universe. Specifically, an EMD blend strategy provides insurance investors with additional diversification, on top of what investors receive from EM, versus DM. Investors can gain diversification and flexibility through hard currency USD sovereigns and corporates as well as local currency assets. It delivers the benefits of security selection within a broader EM mandate, and through the local currency channel, the blended strategy gives investors access to a portfolio that can benefit in a weaker dollar environment. By investing in an EM blend strategy through a vehicle rather than a separate account, insurers can avoid the custody issues that can occur with local currency trades and the accounting issues that exist from owning the securities on the balance sheet.

EMD can Provide Attractive, Capital-Adjusted Yields for Insurance Companies

In addition to asset sector fundamentals and the macroeconomic outlook, relative value is an important input in the strategic and tactical asset allocation process for insurance companies. While absolute spreads and yields are factored in, we believe insurers should evaluate investments on a risk or capital[1]adjusted basis to: (1) screen which asset classes meet or exceed yield hurdles; and (2) determine the relative attractiveness of asset classes. Risk or capital[1]adjusted yields allow for comparability by asset class by incorporating differences in capital treatment and loss (default) experience, as well as additional spread premiums on private assets.

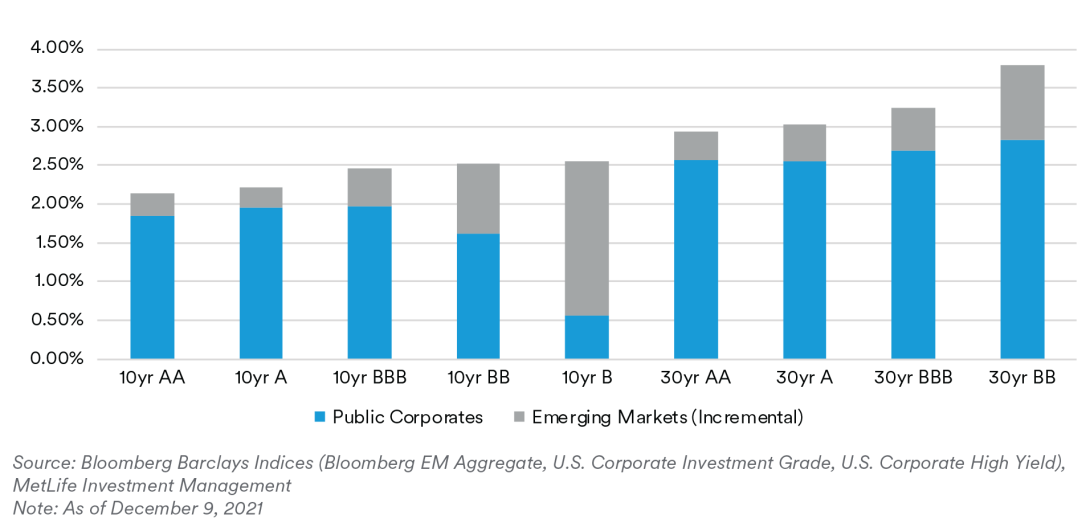

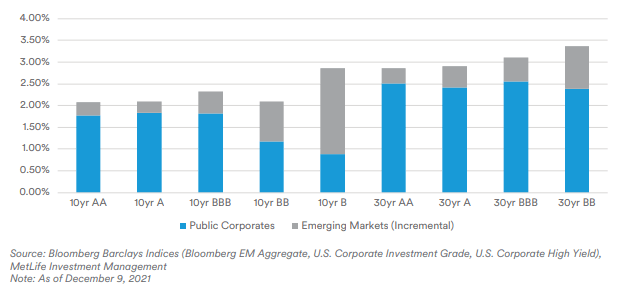

EMD screens as attractive for its capital-adjusted yields, with an average yield pickup of approximately 72 bps as compared to IG and HY corporates (comprising 40 bps average for IG and 140 bps average for HY). The graphs below show 10 and 30-year capital-adjusted yields for U.S. insurance companies under the recently approved, revised risk-based capital (RBC) bond factors, which moved to 20 categories from the prior 6 NAIC buckets. For U.S. life insurance companies, capital-adjusted yields range from 2.2% for 10-year, AA-rated EMD to 3.8% for 30-year, BB-rated EMD. For P&C insurance companies, capital-adjusted yields range from approximately 2.1% for 10-year, AA, A and BB-rated EMD to 3.4% for 30-year, BB-rated EMD. As the graphs show, the largest yield pickups versus corporates for life and P&C companies are in 10-year, B-rated EMD, followed by 30-year and 10-year, BB-rated EMD. For our calculations of capital-adjusted yields, we utilize the relevant EM and corporate index spreads from Bloomberg, historical default rates from Moody’s, and an assumed RBC ratio of 400% (i.e., 4x the amount of required capital). The yields are calculated after tax (at 21% tax rate), but do not include potential diversification and covariance benefits.1

Capital-Adjusted Yields for U.S. Life Insurers

Capital-Adjusted Yields for U.S. P&C Insurers

Conclusion

In the current recovery, we feel EM has a favorable growth outlook relative to DM, with fundamentals benefiting from resilient corporate balance sheets and tailwinds from improved commodity prices. Despite the recent recovery in the asset class, we believe valuations remain attractive; over the coming months, opportunities should exist to capitalize on the wide spread differentials between EM and DM, though security selection and country rotation will be key for any EM investor. For insurance companies, investing in EMD may increase portfolio diversification and generate attractive capital-adjusted yields given spread premiums to IG and HY corporates. Insurance investors can access the EM asset class via various strategies and vehicles, with the most appropriate dependent on insurance company-specific considerations such as income, capital, liquidity, volatility, among others.

Endnotes

1 This capital adjusted yield analysis is intended for educational and informational purposes only, and is based off several assumptions used by the authors (including the RBC ratio, default shaves and tax rate). Any change in the assumptions used could materially alter the yield information presented, and there is no guarantee investors will achieve similar yields to the ones presented herein.

Read More

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

This document is provided by MetLife Investments Securities, LLC, a FINRA member firm and member of SIPC. MetLife Investments Securities, LLC is an affiliate of MetLife Investment Management, LLC. This material is intended for investors who are accredited investors as defined in Regulation D under the U.S. Securities Act of 1933, as amended, and “qualified purchasers” under the U. S. Investment Company Act of 1940, as amended. This document does not constitute an offer to sell or a solicitation of an offer to buy limited partnership interests in a fund. Any such offer may be made only by means of the fund’s definitive private offering memorandum. This material is confidential and is not for onward distribution.

This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Fixed income investments are subject interest rate risk (the risk that interest rates may rise causing the face value of the debt instrument to fall) and credit risks (the risk that the issuer of the debt instrument may default).

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor. This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address Level 34 One Canada Square London E14 5AA United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102- 0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) No. 2414.

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102- 0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) No. 2414.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under U.S. law, which is different from Australian law.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), and MIM I LLC.