![/></figure>

<!-- /wp:image -->

<!-- wp:paragraph -->

<p><strong>Conclusion</strong></p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

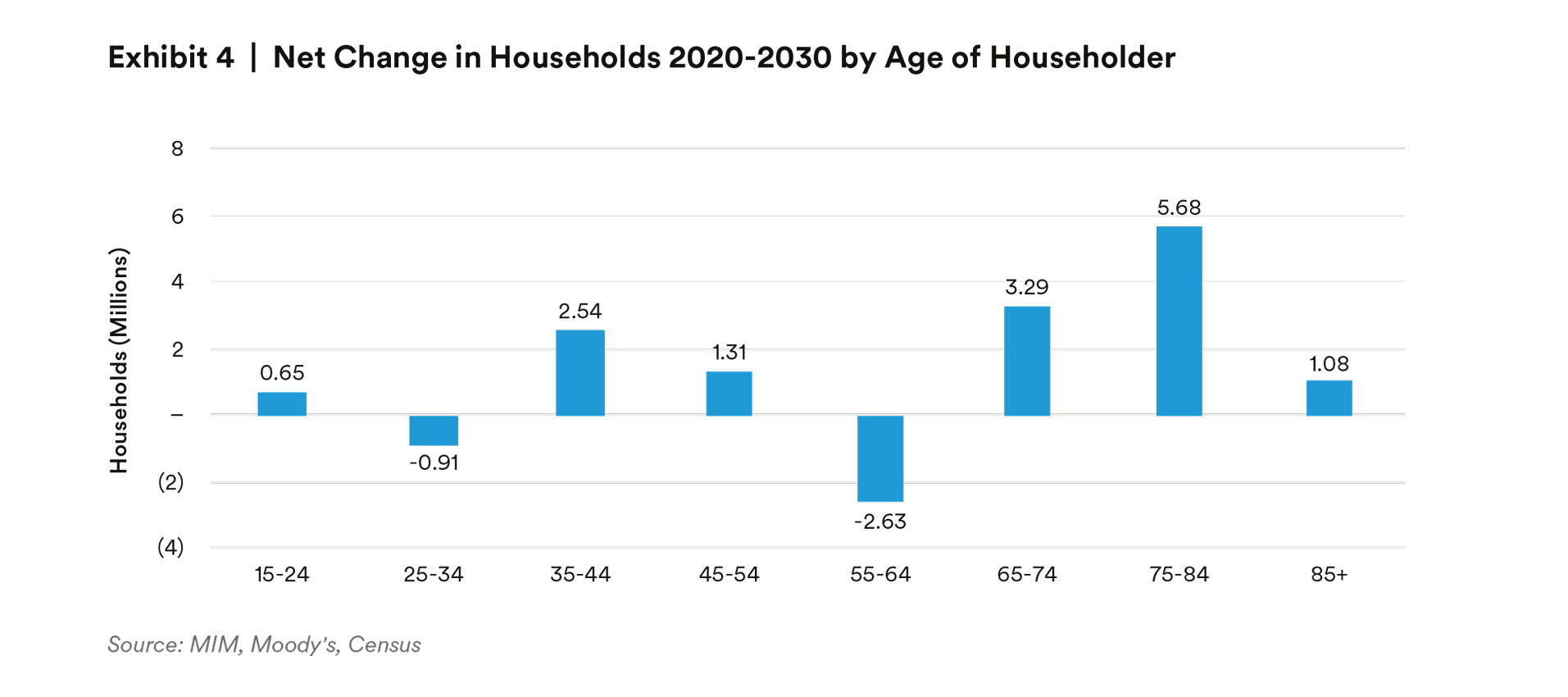

<p>With consideration of these risks, we believe the outlook for the residential sector, including both apartments and single family homes, is positive. We believe ground-up development and build[1]to-core opportunities are worth exploring in the SFR space, particularly in light of tight housing market conditions today as well as demographic shifts pointing toward resilient demand for this asset type.<sup>11</sup> Our outlook for the balance between supply and demand in the traditional apartment sector remains positive, even for studio and CBD apartments. Although we feel demographics may be less favorable for these categories, land, labor, and materials for new residential construction will likely be directed away from these formats, allowing for stable vacancies and rent growth during the decade.</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p><strong>Endnotes</strong><br><sup>1</sup> Demographic shifts from millennials who age into parenthood and want more space to raise children. Secular shifts from office workers who need more space to occasionally work from home.<br><sup>2</sup> NCREIF, 3Q 2021.<br><sup>3</sup> NCREIF, 3Q 2021.<br><sup>4</sup> The committee is chaired by Michael Steinberg of MetLife Investment Management<br><sup>5</sup> Based on analysis of Green Street data, as well as consideration of limited transaction data made available by SFR REITs, and transactions that MIM has considered.<br><sup>6</sup> Moody’s, November 2021.<br><sup>7</sup> Census, November 2021.<br><sup>8</sup> MIM, National Association of Realtors. November 2021.<br><sup>9</sup> Boomer Expectations for Retirement, Insured Retirement Institute. 2019.<br><sup>10</sup> California State Senate, 2021.<br><sup>11</sup> NCREIF, 3Q 2021.</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p><strong>Disclosures</strong></p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p>This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p>This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p>All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p>In the <strong>U.S.</strong> this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p>This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address Level 34 One Canada Square London E14 5AA United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the UK.</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p><strong>For investors in the Middle East:</strong> This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p><strong>For investors in Japan:</strong> This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102-0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) under the registration entry Director General of the Kanto Local Finance Bureau (FIBO) No. 2414.</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p><strong>For Investors in Hong Kong:</strong> This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”).</p>

<!-- /wp:paragraph -->

<!-- wp:paragraph -->

<p><strong>For investors in Australia: </strong>This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients.](https://investments.metlife.com/content/dam/metlifecom/us/investments/insights/research-topics/real-estate/images-new/Article/the-future-of-housing-our-outlook-for-single-and-multi-family-investments/iStock_000058031784_XXXLarge-housing-dev.jpg)

With more than 150 years of heritage, we deliver stability, disciplined risk oversight, and aligned investment strategies purpose-built for insurers. Our conviction-led, specialized teams span public and private markets, targeting dependable income and long-term total return. Recognized by Pensions & Investments as one of the world's Top 10 third-party insurance asset managers, we combine scale and expertise to help insurers address increasingly complex investment challenges. From strategic asset allocation to innovative, capital-efficient portfolio construction, our dedicated insurance specialists design solutions around each insurer’s unique objectives. Backed by on-the-ground expertise in 19 countries, we navigate regulatory and capital constraints with confidence across life, health, P&C and reinsurance.

MetLife Investment Management

One MetLife Way

Whippany, NJ 07981

Madhavi Chugh, CFA

Global Co-Head of Insurance Solutions

madhavi.chugh@metlife.com

(609) 216-6691

Jeannine Heal, CFA

Global Co-Head of Insurance Solutions

jeannine.heal@pinebridge.com

(732) 778-4734